https://www.cmegroup.com/content/dam/cmegroup/education/images/2019/btic-article_984x200.jpg

{kind=link}

BTIC Trading at Index Option Expirations

Basis Trade at Index Close (BTIC) Trading at Index Option Expirations

Most index options traders use index futures for hedging purposes. For cash-settled index options, however, the delta of an in-the-money option vanishes at the moment of expiry, leaving traders to extinguish the futures hedge in the open market. The options settlement price, however, can exhibit a pronounced discrete jump from the “continuous” price path for the index – and, by extension, the hedging vehicle. This discrete jump is random at the moment of expiry.

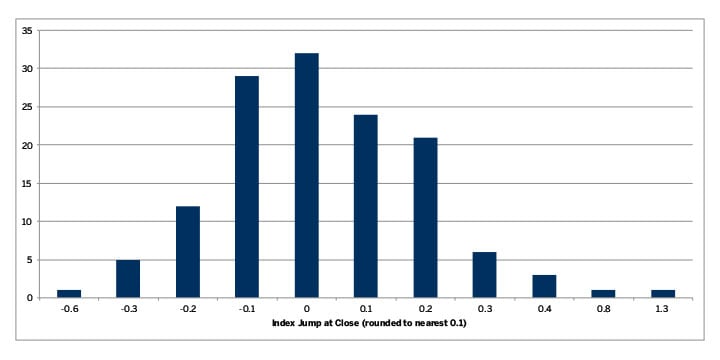

For S&P 500 Index options that settle to the official closing value of the index, the jump in index value is created by the market-on-close orders in each constituent merging with the orders from the continuous order book. The magnitude of this jump varies. Figure 1 shows the distribution of the jump for the last 135 trading days. While E-mini S&P 500 Index futures trade continuously at 4 p.m. ET, the official index close is calculated and disseminated minutes later, with a jump of uncertain magnitude – as large as 1.3 index point in magnitude in this period. The cash close is decoupled from the continuous market at which the futures hedge is extinguished in the continuous market. Thus, the jump in the final settlement mark is an undesirable source of P/L and a challenge for risk management.

Figure 1. Distribution of Index Jump at the Close, sampled from Sept. 21, 2015 – April 4, 2016

{kind=link}

Introducing Basis Trade at Index Close (BTIC)

Basis Trade at Index Close (BTIC) is a new order type introduced in late 2015 for E-mini S&P 500 Index futures that enables trades to be negotiated throughout the day in terms of the basis between the futures versus the cash index value, e.g. -7.85 index points. At the close of business, the official closing value of the index is obtained. The E-mini S&P 500 BTIC trade is then transformed into the trade in the underlying E-mini 500 Index futures, with a price equal to the closing index value adjusted by the basis agreed to in the trade. In this example, if the closing index value is 2066.26, the futures trade will print at 2066.26 + (– 7.85) = 2058.41.

The immediate implication is that the same jump in the closing index value from the continuous path is recaptured in the futures trade. Therefore, the unwinding of the futures hedge through a BTIC trade offsets the jump in the options settlement mark.

The BTIC market in E-mini S&P 500 Index futures trades at a price increment of 0.05 index points. During most of the trading day, the bid/ask spread in the CME Globex electronic trading system averages 0.05 or 0.10 index points with a healthy depth. In contrast, the outright market for the index futures trades at a price increment of 0.25 index points. Figure 2 shows the bid/ask spread of the BTIC market by the hour.

Figure 2. Electronic order book Bid/Ask Spread and Top-of-book depth in E-mini S&P 500 Index Futures BTIC market, data sampled from March 7, 2016 – April 4, 2016.

| Trading Hour (ET) | Avg. Size - Top of Book | B/A (pts) |

|---|---|---|

| 9-10 a.m. | 143 (~$14.65M) | 0.10 |

| 10 – 11 | 207 (~$21.22M) | 0.05 |

| 11 -12 | 354 (~$36.29M) | 0.05 |

| 12 - 1 p.m. | 323 (~$33.11M) | 0.05 |

| 1 – 2 | 383 (~$39.26M) | 0.05 |

| 2 – 3 | 366 (~$37.52M) | 0.10 |

| 3 – 4 | 223 (~$22.86M) | 0.10 |

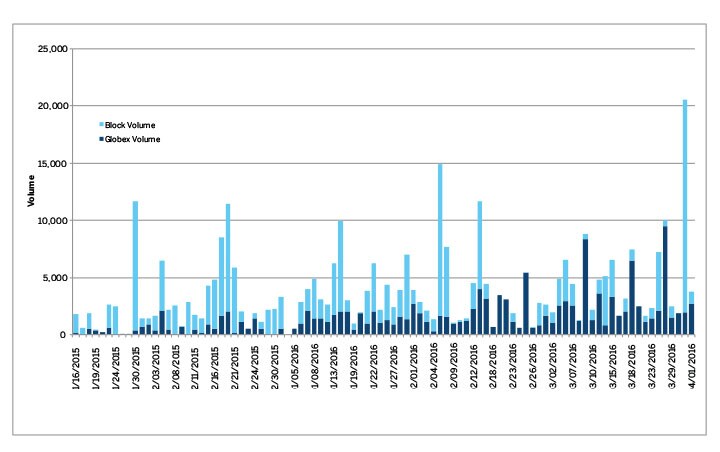

Figure 3. BTIC trading volume in E-mini Index Futures at CME Group

{kind=link}

Each E-mini S&P 500 Index futures contract has a $50 multiplier on the index. And options with $10,000x on the S&P 500 Index (equivalent to 100 listed SPX options) will translate into a 200-contract BTIC trade in E-mini S&P 500 Index futures.

Electronic trading in the BTIC market accounted for approximately 55 percent of the activity recently, with block trades accounting for the balance. As there is a diverse set of market participants who look to trade at a price based on the official closing index value with varying degrees of price sensitivity, options traders would likely be able to execute their hedges at desirable prices.

Option of Futures as Alternative

An alternative to using BTIC to manage the expiry risk on cash index options is to do away with the reference to the official closing index value. Options on E-mini S&P 500 Index futures result in delivery of the underlying E-mini S&P 500 Index futures; as a result, the jump risk in the cash index official closing value is completely bypassed.

For options expiring with the expiration of the futures, the exercise and assignment of in-the-money options result in a futures contract whose value is already fixed. If there is an offsetting position in the futures already, the two positions will simply offset. The final settlement price of the futures (and options) would play no further role in determining the P/L. Options that expire on the third Fridays in March, June, September and December behave this way.

If the options expire prior to the expiration of the futures, the exercise and assignment of in-the-money options result in a futures contract; therefore, the delta does not simply vanish at the expiration. This futures position can be offset with existing futures positions, as well as any ensuing futures trade.

European-style options1 exercise and assignment are driven only by the average price of the underlying futures trading during the 30-second period leading to 4 p.m. ET on the expiration day. This “fixing price” calculation is done virtually instantaneously, with the result publicly available within a split second when the 30-second period has elapsed. Since contrarian instructions are not permitted in these options, the resulting futures positions are also instantaneously known by both the long and short options position holders. As the futures market continues to trade for a short period following the determination of the exercise and assignment, market participants can trade out of any remaining positions in the futures if desired.

There is a dense expiration schedule for options on E-mini index futures. These options expire on the last business day of every week, as well as the last day of the month, in addition to the four quarterly expirations in which the underlying futures are expiring simultaneously. Traders will be able to target important economic events, such as non-farm payroll reports on the first Fridays of each month.

References

1 As of this writing, CME Group is converting all Serial options into European-style exercise. Currently, only April and May 2016 third Friday options on S&P 500 and E-mini S&P 500 Index futures and April, May and July 2016 third Friday options on E-mini NASDAQ-100 and E-mini Dow ($5) options allow for contrarian exercise and abandonment by the options holder. All other “non-quarterly” options are not contrarian instruction eligible. After July 2016, all non-quarterly options on index futures will disallow contrarian instructions on expiration.