{kind=link}

A Cost Comparison of Russell 2000 Futures & ETFs

A Cost Comparison of Russell 2000® Futures & ETFs

INTRODUCTION

This report leverages the framework in the Big Picture Report and compares the all-in cost of replicating Russell 2000 Index exposure via futures and ETFs across four common investment scenarios. The specific products used in the analysis are the Russell 2000 Index futures and the three U.S. listed Russell 2000 ETFs: the iShares IWM, Vanguard VTWO, and SPDR TWOK*.

COST ESTIMATES AND ASSUMPTIONS

The framework for the analysis will be that of an institutional investor executing a hypothetical order of $50,000,000 through a broker. The total cost of obtaining index exposure is divided into two components: transaction costs and holding costs.

TRANSACTION COSTS

Transaction costs are expenses incurred in the opening and closing of the position. These apply equally to all trades, regardless of the time horizon.

Commission: The first component of transaction cost is the fee charged by the broker for the execution, which varies from client to client. This analysis assumes execution costs of 0.2bps ($2.50 per contract) for the futures and 1bps (approximately $0.01 per share based on current prices) for the ETFs.1

Market Impact: The second component of transaction costs is market impact2, which measures the adverse price movement caused by the act of executing the order. Market impact can be difficult to quantify and depends on the given liquidity of the instrument at the time of execution as well as the way the order is executed. This analysis assumes 10bps of market impact for the futures and IWM, and 15bps for TWOK and VTWO.3 Given the superior liquidity of the futures and IWM relative to TWOK and VTWO, the impact estimates appear reasonable.

Table 1. Liquidity Comparison*

| Product | AuM / OI ($Bn) | ADV ($Mn) |

| Futures |

41.41 [text-align: center] |

10,987 [text-align: center] |

| IWM |

37.49 [text-align: center] |

3,968 [text-align: center] |

| VTWO |

1.00 [text-align: center] |

8.81 [text-align: center] |

| TWOK |

0.20 [text-align: center] |

2.01 [text-align: center] |

*H1 -2017 ADV and Average AUM/OI

Source: CME Group and Bloomberg

HOLDING COSTS

Holding costs are expenses that accrue over the time the position is held. ETF expenses generally grow evenly with time (e.g. ETF management fees, which accrue daily) and future expenses vary over time (e.g. execution fees on quarterly futures rolls).

The sources of holding costs for ETFs and futures are different because of the very different structures of the two products. Some, if not all, of the holding costs detailed below will apply depending on the investor.

ETFs:

- Investor must finance the full notional value for the ETF (forgoing additional investments), or use margin power within the account at inception.

- Regulation T margin requirement of 50% at margin loan rates (maximum 2x leverage)

- ETF provider charges an annual management fee 4

- The management fees for the three ETFs in this analysis range from 10bps to 20bps per annum

- Investors are entitled to receive dividends, but may be subject to withholding tax if domiciled outside the U.S.

Futures:

- Initial margin requirement of 3.8% 5 (approximately 26x leverage)

- Russell 2000 futures must be rolled on a quarterly basis, currently observed as 3-month USD ICE LIBOR (3mL) minus 8bps 6

Unlike ETFs, futures do not carry management fees, but rather an implied financing cost embedded in the price. Since the buyer of futures is implicitly paying the seller to replicate the index returns with their own capital, the futures price will be adjusted to reflect the cost of these “borrowed” funds. Recall, the buyer of futures incurs only a nominal cash outlay of 3.8% for initial margin, and the remaining cash balance is available for deposit and will generate interest7 to help offset the implied financing rate of the futures position.

This implied financing rate is most readily inferred in the futures calendar spread, also referred to as “the roll”.8 The price differential between the nearby and deferred contract implies a financing rate, which is compared to the corresponding USD-ICE LIBOR rate over the same period to determine whether the future is rolling “rich” (implied rate “paid” via holding the future is above ICE LIBOR) or “cheap” (implied rate below ICE LIBOR).

This analysis assumes an implied financing rate of 3mL- 8bps for Russell 2000 futures9.

There are structural inefficiencies in the small-cap market that have caused the Russell 2000 futures roll to trade persistently “cheap”10. The less liquid nature of the small-cap stocks makes them more difficult and costly to borrow. Futures are much simpler to use, especially for those investors seeking short exposure who would otherwise have to locate the available stocks to borrow and pay a high borrow fee to sell-short the stocks. Consequently, short investors overwhelmingly prefer to use Russell 2000 futures for obtaining exposure to the small-cap market, resulting in a supply-demand imbalance11. This has translated into a specific implied financing pattern observed over the years, where the Russell 2000 futures roll has traded at a negative spread to 3-month ICE LIBOR.

SCENARIO ANALYSIS

In each case, the total cost is computed for a holding period of 12 months. All scenarios assume the same transaction costs and market impact at both trade initiation and exit.

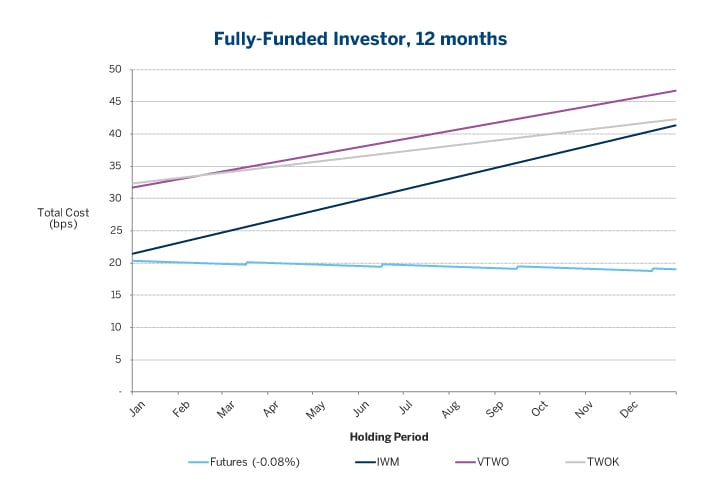

Scenario 1: Fully-Funded Long Investor For a fully-funded investor, the total cost is the sum of transaction costs plus the pro-rata portion of annual holding costs.

The starting point for each graph represents the round-trip execution costs, ranging from 20.4bps for futures to between 21.4bps to 32.4bps for ETFs.

Figure 1

{kind=link}

The ETF lines slope upward as time passes, reflecting the gradual accrual of the annual holding costs; the downward slope of the futures line reflects the cost savings due to the cheapness of the roll, with small jumps illustrating the quarterly roll execution costs.

As evident in the Figure 1, there is no breakeven point in which the ETF becomes more cost-effective than the futures over the 12-month holding period. In fact, the futures would remain the more cost-effective vehicle in perpetuity as the net impact of the quarterly roll execution costs (0.2bps per leg) plus implied financing (3mL -8bps) incurred on the futures is less than the annual management fees charged on the ETFs.

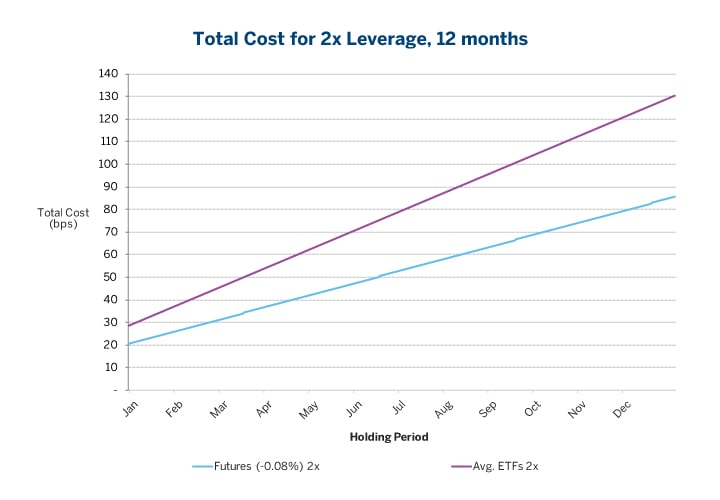

Scenario 2: Leveraged Investor

A major difference between futures and ETFs is the amount of leverage possible with each product. Russell 2000 Index futures require an initial margin deposit of 3.8% , resulting in approximately 26x leverage on the position. The three ETFs in this analysis – IWM, VTWO and TWOK – are not leveraged ETFs, but may be purchased on margin by those investors who desire to leverage their position. Under Federal Reserve Board Regulation T, there are limits on the amount a broker may lend to an investor wishing to purchase securities on margin. For ETFs, the investor is required to deposit a minimum margin of 50% of the purchase price at trade initiation, resulting in a maximum of 2x leverage on the position.12

The 2x leveraged investor is assumed to have $25mm with which to take a $50mm position. The ETF investor, who must pay the full notional amount of the trade at initiation, borrows $25mm from a prime broker to fund the purchase. The holding cost for an ETF position purchased on margin is therefore the same as the fully-funded investor from Scenario 1 plus the interest expense charged on the borrowed $25mm at 3mL+40bps.13

For a futures position, it is not a question about borrowing money, as the investor with $25mm already has 9x the required initial margin. Rather it is a case of generating less interest to defray the baseline financing cost (3mL) embedded in the future. In contrast to the fully-funded investor, the 2x leveraged investor’s amount of cash to deposit is reduced by half and will only generate enough interest to offset one-half of the 3mL-based financing on the total futures notional. Consequently, the 2x leveraged investor will incur the implied financing on the remaining half of the futures notional less the credit of the negative spread on the full $50mm contract value. Hence, his or her holding cost can be viewed as the same as the fully-funded scenario plus the added interest expense of $25mm at the baseline funding rate of 3-month USD-ICE LIBOR.

Figure 2

{kind=link}

Figure 2 shows that as a function of leverage, the total cost associated with futures will never exceed that of the ETFs. For the 2x leveraged investor, the ETF holding cost has increased by 44bps per annum more than the futures due to above-ICE LIBOR rates charged on borrowed funds by a prime broker. Consequently, futures are more economical across all time horizons at the 3mL and roll levels observed at the time of the analysis.

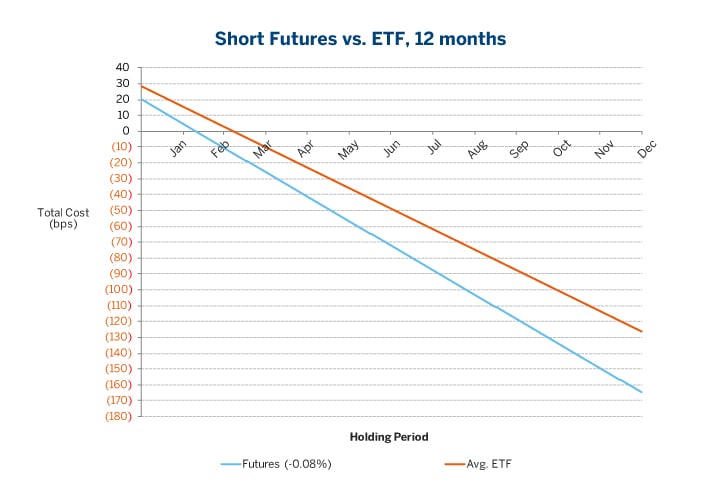

Scenario 3: Short Investor

A short position provides negative market exposure and is inherently leveraged. When analyzing the economics of a short position, it is important to remember that the holding costs for the long investor become benefits for the short. The holding costs for short positions in futures and ETFs can be summarized below:

Futures:

- Receive implied financing rate 14

- Receive 3-month USD-ICE LIBOR on $25mm cash deposit

ETFs:

- Receive the management fee (10-20bps per annum)

- Receive 3mL – 60bps on $50mm raised from the short sale. 15

- Receive 3mL on $25mm cash balance

Figure 3

{kind=link}

Figure 3 shows that the holding costs are negative for both the futures and ETFs – over time, the investor’s relative performance versus the short return of the benchmark improves, as depicted by the downward slope of the lines.

For shorter holding periods, the higher transaction costs of the ETFs make futures the more cost effective choice. As the holding duration increases, the most cost effective vehicle for the short investor depends on the degree of roll cheapness and the ETF management fees. At the 3mL-8bps roll average, futures provide 38bps more cost savings compared to the average ETF over the 12-month holding period. Generally speaking, short investors will save more with futures as the roll richens (or if the ETF management fees decrease), and save less with futures as the roll cheapens (or if the ETF management fees increase). This is also a function of the ETF stock borrow rate: as the spread goes more negative, the futures will provide greater savings16.

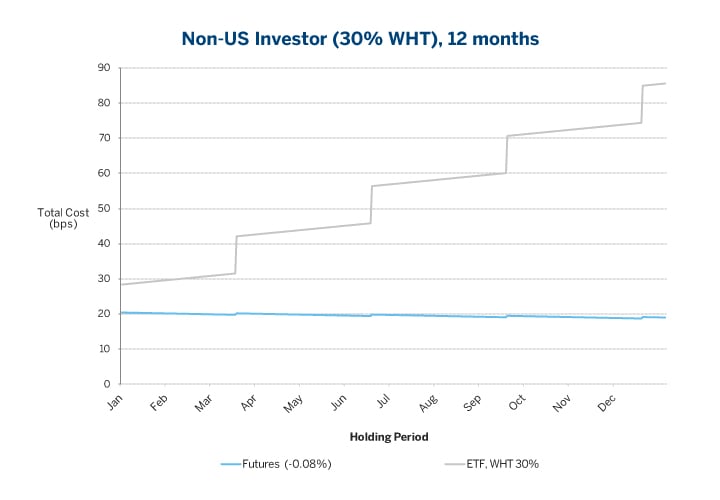

Scenario 4: Non-US Investor

In general, non-US investors in the U.S. equity market are subject to a withholding tax on dividend payments by U.S. corporations. The base withholding rate is 30 percent, resulting in a “net” dividend received by foreign investors equal to 70 percent of the “gross” dividend available to U.S. investors.

This withholding tax also applies to fund distributions paid out by ETFs. The ETFs in this analysis pay a quarterly distribution, which represents the pass through of dividend income received by the fund on the underlying shares held. The dividend yield of the Russell 2000 Index is approximately 1.40 percent, which implies an additional 42bps holding cost per annum for non-US ETF investors due to the withholding tax.

Futures contracts, unlike ETFs, do not pay dividends. For non-US investors, futures on qualified indices are not subject to a dividend withholding tax per IRS Rule 871(m). The Russell 2000 Index is believed to be a qualified index product so non-US investors are exempt from withholding tax on Russell 2000 Index futures.

Figure 4

{kind=link}

Figure 4 shows the holding comparison for a fully-funded long position (Scenario1) as experienced by a non-U.S. investor based on a 30 percent withholding. The jump in the purple line illustrates the impact of the withholding tax for the ETF holder, and the futures is the more cost effective product in perpetuity.

CONCLUSION

The cost advantages of the Russell 2000 Index futures over the corresponding ETFs are remarkable and should not be ignored. The fully-funded investor can save between 22 to 28bps per annum when using Russell 2000 futures in lieu of ETFs for a 12-month holding period. For the 2x leveraged, futures can provide on average 44bps of savings, while the futures cost savings are even larger for the non-US investor at an average of 66bps. The most cost effective vehicle for the short investor depends on the holding period and degree of roll cheapness, as well as the ETF management fee and stock borrow rate. Generally, futures will be the most economical choice because the short investor will receive more from the credit of the futures implied financing rate than the credit received from the sum of the ETF management fees plus the interest generated from the short sale of the ETF. In this analysis, the short investor would save on average 38bps per annum using futures in lieu of ETFs.

Table 2: Summary of Results

| Total Futures Cost Savings by Scenario (in bps)* | ||||

|

Scenario 1 [text-align: center] |

Scenario 2 [text-align: center] |

Scenario 3 [text-align: center] |

Scenario 4 [text-align: center] |

|

|

Full-Funded [text-align: center] |

2x Leveraged [text-align: center] |

Short Investor [text-align: center] |

Non-U.S. Investor [text-align: center] |

|

| Russell 2000 Futures |

+22bps to +28bps [text-align: center] |

+44bps [text-align: center] |

+38bps [text-align: center] |

+66bps [text-align: center] |

Table 3: Most Cost Effective Choice

| Most Cost Effective Choice | ||

|

Scenario [text-align: left, width: 20%] |

Roll is Cheap [text-align: left, width: 40%] |

Roll is Rich [text-align: left, width: 40%] |

| Fully-Funded | FUTURES | Depends on holding period and degree of roll richness |

| Leveraged (2x) | FUTURES | FUTURES |

| Short Investor | Depends on holding period, degree of roll cheapness, ETF management fee, and cost of borrow | FUTURES |

| Non-U.S. Investor | FUTURES | FUTURES |

Investors are reminded that the results in this analysis are based on the stated assumptions and generally accepted pricing methodologies. The actual costs incurred by an investor will depend on the specific circumstances of both the investor and trade including the trade size, time horizon, broker fees, execution methodology and general market conditions at the time of the trade, among other. Investors should always perform their own analysis. For questions or comments about this report or CME Equity Index products, contact equities@cmegroup.com

References

*On October 16, 2017, State Street changed indices for TWOK from the Russell 2000 Index to the SSGA Small Cap Index. Additionally, State Street reduced TWOK’s management fee from 10bps to 5bps.

- Transaction cost estimates are based on “middle-of-the-range” pricing for institutional clients.

- In the simplest case – an unlimited market order sent directly to the exchange – the market impact can be accurately defined as the difference between the market price immediately prior to the order being submitted and the final execution price of the trade.

- Average impact based on feedback from liquidity providers.

- The annual management fee is 20bps for IWM, the most liquid of the ETFs; 15bps for VTWO and 10bps for TWOK.

- Margin amounts are subject to change. On September 12, 2017, the initial margin estimate for E-mini Russell 2000 futures was $2,750 on a contract notional of roughly $72,050.

- This analysis uses a roll cost of 3mL -8bpsbps, which was the respective average cost during the preceding four quarterly rolls.

- It is assumed interest earned on cash deposits will be on par with the baseline risk-free rate used to value futures. This analysis uses a financing rate equal to 3mL to align with standard convention for U.S.-based equity products.

- Since futures expire on a quarterly basis, an investor wishing to maintain a futures position will realize this cost when “rolling forward” their positions by liquidating the nearby contract and re-establishing the position in the deferred month contract.

- This analysis uses the 3mL rate of 1.33% during the most recent roll (Sep-Dec 2017) and a roll level of 3mL-8bps, which was the respective average cost during the preceding four quarterly rolls.

- The average roll cost over the last eight quarters was 3mL -50bps.

- Those holding long positions in small-cap stocks are also willing to sell the futures at a discount to 3-month ICE LIBOR since they can generate additional fees via loaning small-cap stocks. Also, it is more difficult for index arbitrageurs to capitalize on pricing inconsistencies between the index futures and basket of stocks for Russell 2000 as it requires buying the futures and selling the 2,000 stocks in the index.

- Unlike futures, ETFs are subject to Federal Reserve Board Regulation T margin requirements.

- Average borrow rates for IWM of 3mL +40bps bps are assumed.

- The short sale of futures does not require a loan of shares to sell short or pay the associated fee. The sale of futures is identical to the purchase, with the same margin posted with the clearing house.

- The ETF holder borrows shares to sell short from a broker and pays a borrow fee, which is deducted from the interest paid on the cash raised from the sale. A standard broker fee of 60bps per annum is assumed, resulting in a rate return on the cash raised of 3mL – 60bps.

- If the prime broker rate negative spread plus the negative management fee is more negative than the futures spread to ICE LIBOR, then the future will remain the more cost effective product.

Equity Total Cost Analysis Tool

Explore the potential cost savings of E-mini Russell 2000 Index futures for your specific investment scenario