Like SPAN, the SPAN 2TM framework will be based on a Value at Risk (HVaR) framework, using historical data to model how a position or portfolio may gain or lose value under various risk scenarios.

The SPAN 2 framework will allow implementation of granular and dynamic adjustments to margins at a product and portfolio level. In addition, enhanced reporting of margining into different risk factors such as market risk, liquidity, and concentration will be provided.

- To ease the transition and facilitate margining of portfolios that have products across both the SPAN and SPAN 2 frameworks, CME will ensure customers can continue to use the SPAN margining system, which will support both the current and enhanced methodology inside the system.

- CME will provide a range of margin services tools to enable customers to evaluate their portfolio and see how the SPAN 2 framework may impact their margin levels.

Total Portfolio Margin =

x*Historical Risk

+ (1-x)*Stress Risk

+ Liquidity

+ Concentration

Market Risk/HVaR Overview

Market Risk/HVaR Overview

Assess the potential losses a portfolio can incur due to the daily price movements over a reasonable lookback period. HVaR uses a minimum of 10-year historical data and scenarios are generated using volatility and correlation scaling. Explicit treatment is made for seasonal risk and for options where the implied volatility surface is used including skew as risk factors.

Stress Risk Overview

Stress Risk Overview

Assess the potential losses a portfolio can incur due market events. This framework allows risk managers to add expert judgment to manage seen and unforeseen risks and is made of two parts.

Portfolio Liquidity Charge

Portfolio Liquidity Charge

The liquidity charge captures close out costs during a default, based on available bid/ask spreads from a reasonable lookback period. Close out costs are assessed according to trading practices and costs observed in the market. The costs are calibrated to actual traded information for products when available.

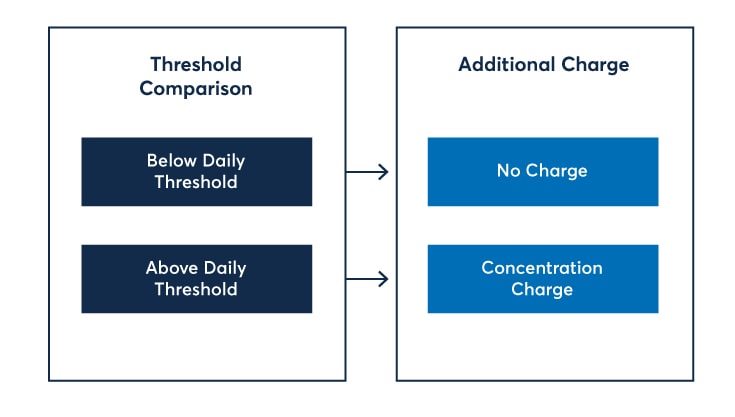

Concentration Charge

Concentration Charge

The concentration charge accounts for the additional cost of closing out large portfolios due to their size, an add on if the size of the holding is higher than a certain level of threshold, which is calibrated from recent days of Average Daily Volume.

Firms using the SPAN 2 framework will get the same reports they use today for back office processing, collateral management and settlements. To help you better understand the portfolio margin requirements using the SPAN 2 framework, new reports will also be produced from our post-trade risk services.

During the prod parallel period we will be publishing accurate files using the SPAN 2 methodology at least once a day that will allow for customer evaluation against SPAN.

The Risk Parameter files will be separate for the SPAN and SPAN 2 frameworks.

We will continue to facilitate offsets across the SPAN and SPAN 2 frameworks as per the below illustration.

PostTradeServices@cmegroup.com

Global Support

US: +1 312 580 5353

UK: +44 20 3379 3500

APAC: +65 6593 5599

© 2026 CME Group Inc. All rights reserved.