Intercommodity Spreads (ICS) allow traders to conduct spread trades between Treasury futures contracts at different points on the yield curve in a single transaction. ICS allow for easier and more efficient execution, and eliminates the risk of price slippage by executing all legs at once.

The ICS section of the Treasury Analytics tool provides current statistics for market participants looking to trade and hedge these yield curve spreads.

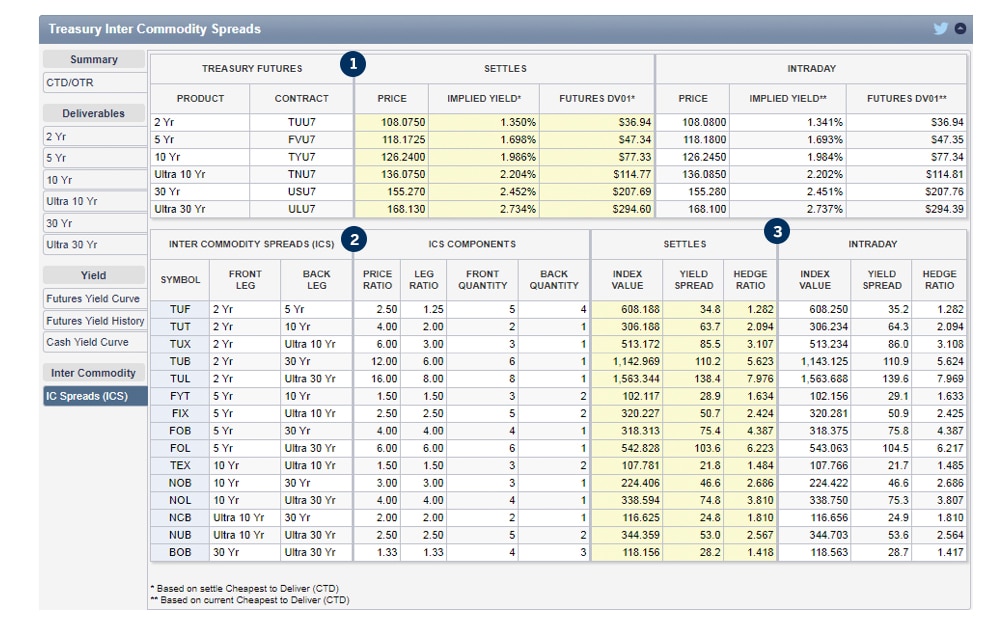

The first row of the ICS tool lists each Front Month Treasury Futures contract, which are the components of each ICS. The “Settles” box in the top row lists the Price, Implied Yield, and DV01 for each contract based on the previous trading day’s settlement CTD. The “Intraday” box in the top row lists the Price, Implied Yield, and DV01 of the current CTD based on intraday trading activity.

The “Intercommodity Spreads” section lists the symbol for each ICS and identifies the front and back leg of the spread. The “ICS Components” section then lists the leg ratios and price ratios for each spread, along with the corresponding leg quantities.

Ratio Calculations

Leg Ratio = Front Leg Quantity / Back Leg Quantity

Price Ratio = Total Front Leg Notional / Total Back Leg Notional

Index Value, Yield Spread, and Hedge Ratios of each ICS on the tool are calculated for both the previous trading day’s settlement CTD and for the current CTD based on intraday trading activity.

The Index Value quotes the spread without relying on net change on the day pricing conventions. Yield Spread measures the Implied Yield difference between the front and back leg contracts. The Hedge Ratio represents the DV01 weighting of a 1:1 spread between the ICS components.

ICS Statistic Calculations

Index Value = [(Front Leg Price * Front Leg Quantity) – [(Back Leg Price * Back Leg Quantity)]

Yield Spread = Back Leg CTD DV01 Implied Yield – Front Leg CTD DV01 Implied Yield

Hedge Ratio = Back Leg DV01 / Front Leg DV01

The holder of a short position in a Treasury futures contract must deliver a cash Treasury security to the holder of the offsetting long futures position upon contract expiration. There are typically several cash securities available that fulfill the specification of the futures contract. Because of accrued interest, differing maturities, etc. of the various cash securities, there are differing cash flows associated with the deliver process. The cash security with the lowest cash flow cost is known as the Cheapest to Deliver.

The Yield for a futures contract is calculated as the yield to maturity of a cash security with the following specifications:

- Settlement Date = last delivery day for the futures contract

- Maturity Date = maturity date of the CTD cash security

- Coupon Rate = coupon rate of the CTD cash security

- Bond Price = futures price * conversion factor

- Coupon Frequency = coupon frequency of the CTD cash security

- Day Count Basis = actual/365

- Par Value = 100

DV01, sometimes called Dollar Duration, is the change in the value of a treasury (cash or futures) in dollars, for a one basis point (.01%) change in the yield.

© 2026 CME Group Inc. All rights reserved.