Learn about Basis: Grains

{kind=link}

Understanding Grains Basis

The futures markets for Grains and Oilseeds indicate the prices for those commodities that are discovered through buying and selling at the exchange, representing the culmination of the forces of supply and demand.

Cash prices and futures prices tend to move up and down together, which is what makes the concept of effective hedging possible. But those whose business involves buying or selling physical grains and oilseeds are aware that the cash price in their own local area, or what their supplier quotes for a given commodity, usually differs from the price that is quoted in the futures market.

This is because in local markets, the futures price for a commodity is going to be adjusted for variables such as freight, handling, storage and quality, as well as supply and demand factors impacting that particular area. This price difference is known as the basis, which is calculated as the cash price minus the futures price.

Basis can be either positive or negative. A negative basis is referred to as being under, in other words, the cash price is under the futures price. A positive basis is referred to as being over, the cash price is over the futures price.

Basis is important because it affects the final outcome of a hedge, in terms of the ultimate price either paid or received.

Examples

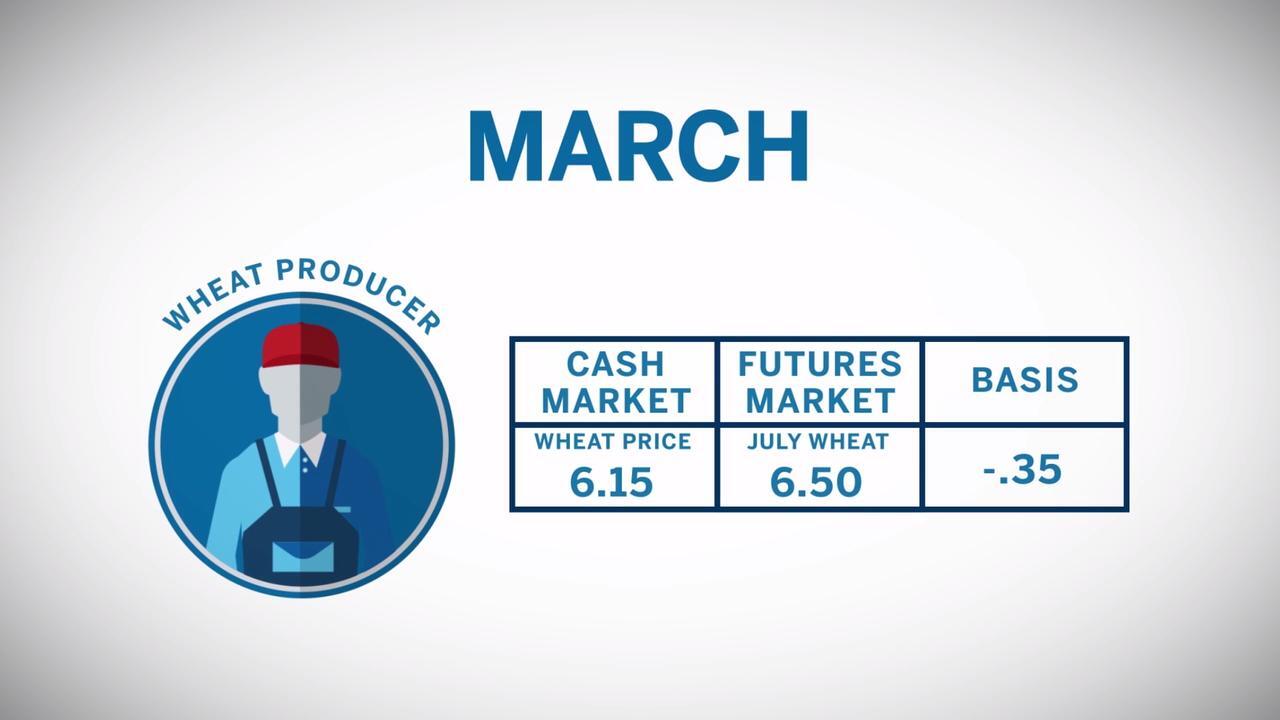

In March, a wheat producer plans to sell his crop to his local elevator in mid-June, so he is looking to establish a short position in the July Wheat futures contract. The July Wheat futures price is $6.50 per bushel, and the cash price in his local area in mid-June is normally around 35 cents under the July futures price.

With a basis of 35 cents under, the approximate price this producer is trying to establish by hedging is $6.15 per bushel, which is the futures price of $6.50 minus the expected basis.

One of the key considerations in understanding the basis is its potential to strengthen or weaken when cash prices increase or decrease relative to the futures prices. The more positive – or less negative – the basis becomes, the stronger it is. In contrast, the more negative – or less positive – the basis becomes, the weaker it is.

A strengthening basis will increase the selling price for a short hedger. In the previous example, suppose the basis in mid-June turned out to be 30 cents under rather than the expected 35 cents under. Then, the net selling price, taking into account both futures and cash transactions, would be $6.20, rather than $6.15.

A basis that is weaker – or more negative – than expected, decreases the selling price. Had the basis changed from 35 cents under to 40 cents under, the net selling price would be $6.10.

Basis and Long Hedge

Basis has the exact opposite effect on a long hedge; long hedgers benefit from a weakening basis

Imagine that in October a livestock feeder is planning to buy soybean meal in April, so he is looking to establish a long hedge in the May Soybean Meal futures contract. May Soybean Meal futures are trading at $350 per ton, and the local basis in April is typically around $20 over the May futures price.

This hedge would result in an expected purchase price of $370 per ton: $350 May futures + $20 over expected basis.

But what if the basis strengthens, becomes more positive, and instead of the expected $20 over it actually $40 over in April? Then, the net purchase price increases to $390 per ton: $350 + $40.

Conversely if the basis weakens, moving from $20 over to $10 over, the net purchase price drops to $360 per ton: $350 + $10.

Again, note that the long hedgers benefit from a weakening basis and short hedgers benefit from a strengthening basis.

Summary

The behavior of the basis in Grains and Oilseeds markets can have a significant impact on the performance of a hedge. By hedging with futures, buyers and sellers are essentially reducing their price risk by assuming basis risk. Basis risk is typically much lower than price risk, so the tradeoff is worth it.. Planning is key and it is important that hedgers maintain historical basis records in order to make realistic basis expectations for the time they plan to buy or sell.