{kind=link}

Introduction to the Japanese power market

Reforms and market opening

Japan was one of the first countries to use electric lighting. The Tokyo Electric Light Company (the predecessor of Tokyo Electric Power Company) was established in 1883, less than five years after Thomas Edison invented the incandescent lamp. Since then the Japanese electricity market has developed into one of the largest in the world.

Long dominated by 10 regional integrated companies with a virtual monopoly on generation and distribution in their respective area, the Japanese power market has been gradually opened to competition since the mid-90s and reaching full liberalization in 2016 ‒ paving the way for development of a financial market like the German power market.

Fig.1a: Japanese power market liberalization – timeline

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/introduction-to-the-japanese-power-market-fig22.jpg

Source: FEPC, TEPCO

{kind=link}

The Great East Japan earthquake in March 2011 and the subsequent Fukushima Daiichi accident marked a turning point in this process, with the resulting tight demand and supply balance reinforcing the need for reforms.

The Japanese model of liberalization is based on fair competition and transparency while keeping a strong focus on ensuring a stable supply of electricity across the country.

Two entities are key in this process. The Organization for Cross-regional Coordination of Transmission Operators (OCCTO) was established in 2013, while the Japan Electric Power Exchange (JEPX) started operation in 2015.

JEPX is Japan's only wholesale electricity exchange acting as an intermediary for electricity sales between producers and retailers. JEPX auction mechanisms enhance competition among market participants and are designed to improve efficiency in this newly liberalized electric power business.

Fig.1b: JEPX day-ahead daily volumes

{kind=link}

JEPX only permits physical electricity participants to become exchange members.

Daily trading volumes on JEPX reached on terawatt hour (1 TWh) in 2020 and are regularly above 800-gigawatt hour (GWh), corresponding to roughly 1/3 of the national daily demand. By comparison, 53.7 TWh was traded on EPEX Spot’s markets in the Germany Intraday market in 2019, a rise of 4.6% versus 20181. A total of 593.2 TWh was traded across the European markets in 2019, according to the latest EPEX spot data.

JEPX allows for different types of bidding/offering:

- Day-ahead market (spot market): balancing point of generation and demand plans for every 30-minutes period of the next day.

- Market of the day (pre-time market): electricity trading for adjustment due to power generation malfunction on the day and change in temperature.

- Forward market: allow members to fix the price of electricity delivered in the future.

The day-ahead (spot market) contract price is set by JEPX during a blind single price auction at the intersection of the supply and demand curve provided by members prices are set for each 30-minute period of the day (48 daily prices).

JEPX divide the calculation by region due to constraints on the amount of electricity that can be passed through interconnection lines.

The contract prices calculated by this process are called area prices (six areas in Western Japan and three areas in Eastern Japan).

The intersection price calculated by combining bids across Japan is called the system price.

Fig. 2a: structure of the Japanese power market

{kind=link}

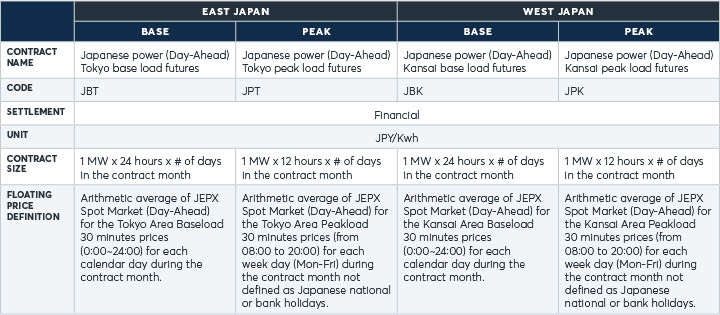

Among these nine areas, the region of Tokyo and Kansai are the largest in term of electricity consumption.

In the nascent derivative market, the Tokyo area serves as the benchmark for East Japan and the Kansai area plays a similar role for West Japan.

For these two areas, derivative transactions are based on JEPX Day-Ahead assessments over a calendar month, either for all 30-min prices (baseload) or for weekdays from 8:00 am to 8:00 pm (peak load).

Fig. 2b: NYMEX Japanese Power futures contract

{kind=link}

Baseload contracts allow commercial hedgers to manage the price exposure for a given month. By contrast, peak load contracts offer an additional hedging granularity with floating prices covering the peak-hours (08:00 to 20:00) and excluding weekends and holidays.

Size matters

Currently only a limited number of countries in the Asia-Pacific region, like Australia and Singapore, have a liberalized electricity market and an adjacent derivatives market.

Electricity demand in Japan is far greater than the one in Germany; the largest market in Western Europe and home of a deep derivatives market. A total of 1,088.5 TWh were traded in German baseload and peak load futures in 2019, a 28% increase in the volumes recorded in 2018.

With a physical market nearly four times bigger than its Australian counterpart, Japan has the potential to become a vibrant derivatives market attracting both commercial hedgers and traders.

Fig. 3a: power generation in Japan & selected countries with an existing power derivatives market

{kind=link}

Adding to an impressive size of nearly 1,000 TWh per year, Japan’s electricity production is based on a diversified generation mix, a large number of active firms, a weather-driven seasonality, and an interconnected grid.

This contrasts with Australia, which is largely dominated by coal generation, and Singapore, which uses largely natural gas for power generation, lacking a strong seasonality and interconnection.

Fig. 3b: power generation mix in some APAC countries

{kind=link}

{kind=link}

{kind=link}

Source: IEA

These factors combined with a very active physical spot market provide a good ecosystem to develop a liquid paper market based on the Tokyo and Kansai area benchmarks.

Several international firms, mainly energy majors and European utilities, have already entered the Japanese power market, attracted by the potential trading opportunities it offers.

Japan energy mix and generation capacity

Japan’s diversified generation capacity allows for optimization between different sources of energy depending on the economics.

The country had to adapt as well to a changing generation landscape since 2011, when it was forced to close of all its nuclear reactors.

The nuclear factor

Electricity from nuclear plants represented 25% of the country power generation in 2010 but dropped to zero in the years following the Fukushima Daiishi accident. While Japan has implemented a massive plan to review and reinforce the security of its nuclear installation, the future re-commissioning of several plants will depend on regulatory approval as well on political choices, themselves influenced by the opinion of local communities.

By November 2020, Japan had 33 operable nuclear reactors with a total installed generating capacity of 32 GW, down from 54 reactors with 47 GW of capacity before the Fukushima accident in 20111. Only a limited number of these reactors in the Kansai, Kyushu, and Shikoku regions were operating.

Japan: world’s largest LNG importer

Japan is historically the largest importer of liquefied natural gas (LNG) in the world. Even if China is forecasted to take over this position in the coming years, Japan remained the largest imported of the ultra-chilled gas in 2019.

Fig. 3c: LNG imports in key Asian countries

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/introduction-to-the-japanese-power-market-fig04.jpg

Source: International Gas Union IGU world LNG reports

{kind=link}

Renewables transition in power?

Power generation is continuing to shift towards renewable energy, driven by policy, innovation, and access to capital. This mirrors what has happened in other developed power markets in Europe where wind and solar energy are part of the generation mix.

The Ministry of Economy, Trade, and Industry (METI) announced in 2020 a plan to gradually phase out inefficient thermal coal fired power plants2.

Thermal coal is an important baseload source for power generation in Japan, accounting for nearly 30% of the country’s production in 2019. METI is targeting mainly plants with a lower heat conversion rate, while Ultra Super Critical -USC- plants and other efficient installations will still be allowed to operate.

Later in 2020, newly elected Prime Minister Suga pledged to achieve net zero carbon emissions by 20503.

With most of the country’s nuclear power plants idle, it means that Japan will have to increase its renewable generation capacity, and this will provide a central role for LNG in the generation mix.

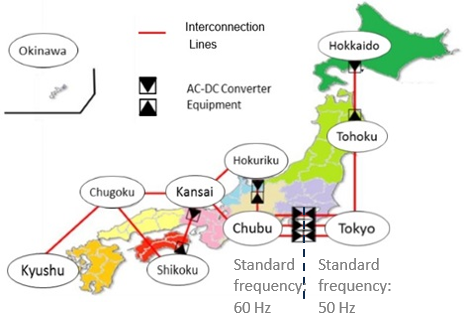

Regional differences

The generation mix is not only diverse, it is as well different for each region. Exchanges through service areas are possible through interconnections and AC-DC converters.

Fig. 4a: peak demand by service area (FY 2109) and interconnections capacity

{kind=link}

A series of individual but connected regional power markets have been created with their own supply and demand characteristics. On instruction from OCCTO, the generation capacity from one region can be used to divert supply to different regions where issues occur.

This creates an integrated and interconnected market with regional arbitrage opportunities, while two references serve as benchmarks for East and West Japan respectively, as well as liquidity aggregators for the burgeoning paper market.

In the key service areas of Tokyo and Kansai, LNG was the largest source of power generation during the 2019 financial year, with 65% and 42% of the total generation respectively. The remaining regional power markets in Japan are smaller and not diverse enough to support a vibrant derivatives markets at this point.

Fig. 4b: generation capacity and actual generation (FY 2019)

{kind=link}

{kind=link}

For producers in these regions the spread between LNG and power prices are key indicators.

Historically, LNG imported to Japan through term contracts was linked to oil prices, more specifically to the Japan Crude Cocktail (JCC). In the last few years, imports based on spot prices increased but JCC remains an important benchmark for Japanese LNG.

With the increase of US LNG exports, NYMEX Henry Hub has gradually increased its influence in the Japanese market, consolidating its status of global benchmark for natural gas.

Creating a trading ecosystem for a hedger

The spark spread is defined as the difference between the price that a power generator can obtain from selling electricity and the cost of the natural gas needed to generate it. It is usually calculated in megawatt hour (MWh). Converting the price of natural gas depends on its calorific value, pricing unit, and the efficiency rate of each power plant.

Spark spread is a key measure of potential profit for generating electricity an to compare this profit to other energy source like coal (dark spread).

Fig. 5: historical prices for Japanese power and Japanese Crude Cocktail

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/introduction-to-the-japanese-power-market-fig20.jpg

Source: JEPX, METI

{kind=link}

JCC futures denominated in US dollars are already listed on NYMEX2, as well as Platts JKM futures in US dollars.

In order to facilitate spark-spread hedging without taking a foreign exchange’s exposure, JCC futures and JKM futures (denominated in Japanese yen) are now available as well for trading. Traders can adjust quantities on both legs on the spread to reflect their physical exposure.

With the addition of these contracts, thereby complementing the existing wide range of natural gas futures and options, market participants have relevant and efficient hedging tools at their disposal on the same exchange.

{kind=link}

Conclusion

Japan is the third largest economy in the world and is the home of a huge power market which has been fully liberalized. In term of size, generation mix and infrastructures, this market gathers all the conditions favorable for the emergence of a vibrant futures market.

Japanese Power futures on NYMEX, combined with the existing LNG futures, sit alongside the existing benchmarks on natural gas. This offering provides a diverse set of trading instruments that can be accessed during Asian hours (and beyond). All products are available for clearing via CME Clearing.

With the help of these instruments and CME Group’s platforms, the Japanese derivatives market enters a new and exciting age.