Get to know: FX Monthly Futures

Subscribe to UpdatesTrade a key part of our comprehensive, efficient, central liquidity pool to manage FX forward and swap exposure.

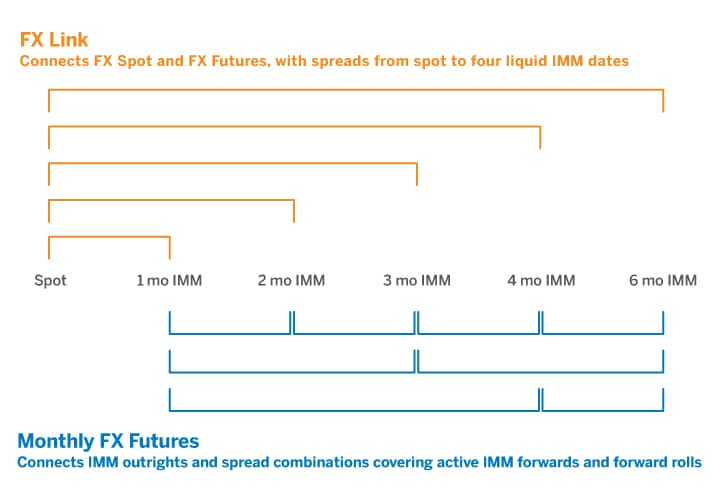

Trade monthly FX futures, with implied pricing, on six of our most liquid currency pairs. Giving you more liquidity, more trading opportunities, and more ways to streamline your costs, via the capital efficiencies of futures and increased outrights and spreads across the FX curve.

- With quarterlies, more ways to trade first four monthly IMM dates

- No credit line tie-ups and a shorter, two-day Margin Period of Risk (MPR)

- Lower leverage ratio, risk-weighted asset utilization reduces balance sheet impact

- Full netting, same currency and maturity date, fewer line items

- Reduced minimum tick of one-tenth for consecutive month spreads means lower costs

- Now, combined with FX Link you can trade one spread in the OTC Spot FX market via our monthly futures

- Transparency of an open-access, electronic central limit order book

- Blocks, EFPs and Request For Crosses allow you to trade off-exchange

Elligible Currencies

EUR/USD, JPY/USD, GBP/USD, AUD/USD, CAD/USD, EUR/GBP

Contract Months

EUR/USD, JPY/USD, GBP/USD, AUD/USD, CAD/USD: 3 monthlies, in addition to current offering of 20 quarterlies

EUR/GBP: 3 monthlies, in addtion to current offering of 6 quarterlies

Daily Settlement

Settlement prices established at 14:00 CT

Contract Settlement

Physical delivery

Trading Hours

CME Globex and CME ClearPort: Sunday – Friday, 17:00 – 16:00 CT, with a 60-minute break each day beginning at 16:00 CT and no 17:00 CT session on Fridayettlement prices established at 14:00 CT

Position Accountability

Single & All Months: 10,000 Contracts Single & All Months: 6,000 Contracts

EFRPs

Allowed

Matching Algorithm

Outrights: FIFO Spreads: Pro-Rata

| Euro Futures | Japanese Yen Futures | British Pound Futures | Australian Dollar Futures | Canadian Dollar Futures | EUR/GBP Futures | |

| On Globex | 6E | 6J | 6B | 6A | 6C | RP |

| On Reuters | 1URO | 1JY | 1BO | 1AD | 1CD | RP |

| On Bloomberg | ECA Curncy | JYA Curncy | BPA Curncy | ADA Curncy | CDA Curncy | RPA Curncy |

| Contract Size | 125,000 EUR | 12,500,000 JPY | 62,500 GBP | 100,000 AUD | 100,000 CAD | 125,000 EUR |

| Quotation | Quoted in USD per EUR | Quoted in USD per JPY | Quoted in USD per GBP | Quoted in USD per AUD | Quoted in USD per CAD | Quoted in GBP per EUR |

| Tick | Outrights: | Outrights: | Outrights: | Outrights: | Outrights: | Outrights: |

| 0.00005 USD per EUR (6.25 USD) | 0.0000005 USD per JPY (6.25 USD) | 0.0001 USD per GBP (6.25 USD) | 0.0001 USD per AUD (10.00 USD) | 0.00005 USD per CAD (5.00 USD) | 0.00005 GBP per EUR (6.25 GBP) | |

| Consecutive Month Spreads: 0.00001 USD per EUR (1.25 USD) | Consecutive MonthSpreads: 0.0000001 USD per JPY (1.25 USD) | Consecutive Month Spreads: 0.00001 USD per GBP (0.625 USD) | Consecutive Month Spreads: 0.00001 USD per AUD (1.00 USD) | Consecutive Month Spreads: 0.00001 USD per CAD (1.00 USD) | Consecutive Month Spreads: 0.00001 GBP per EUR (1.25 GBP) | |

| All Other Spread Combinations: 0.00005 USD per EUR (6.25 USD) | All Other Spread Combinations: 0.0000005 USD per JPY (6.25 USD) | All Other Spread Combinations: 0.0001 USD per GBP (6.25 USD) | All Other Spread Combinations: 0.00005 USD per AUD (5.00 USD) | All Other Spread Combinations: 0.00005 USD per CAD (5.00 USD) | All Other Spread Combinations: 0.000025 GBP per EUR (3.25 GBP) | |

| Last Trading Day | 9:16 a.m. Central Time (CT) on the second business day immediately preceding the third Wednesday of the contract month (usually Monday) | 9:16 a.m. CT on the business day immediately preceding the third Wednesday of the contract month (usually Tuesday) | 9:16 a.m. Central Time (CT) on the second business day immediately preceding the third Wednesday of the contract month (usually Monday) | |||

| Reportable Limits | 200 Contracts | 25 Contracts | ||||

| Block Trade | Monthlies: 20 Contracts | Monthlies: 20 Contracts | Monthlies: 20 Contracts | |||

| Quarterlies: 150 Contracts | Quarterlies: 100 Contracts | Quarterlies: 50 Contracts | ||||

| Spreads: Sum of the legs must equal the higher of the two block thresholds | Spreads: Sum of the legs must equal the higher of the two block thresholds | Spreads: Sum of the legs must equal the higher of the two block thresholds | ||||

© 2026 CME Group Inc. All rights reserved.