{kind=link}

NYMEX LNG Freight futures – first successful year

Introduction:

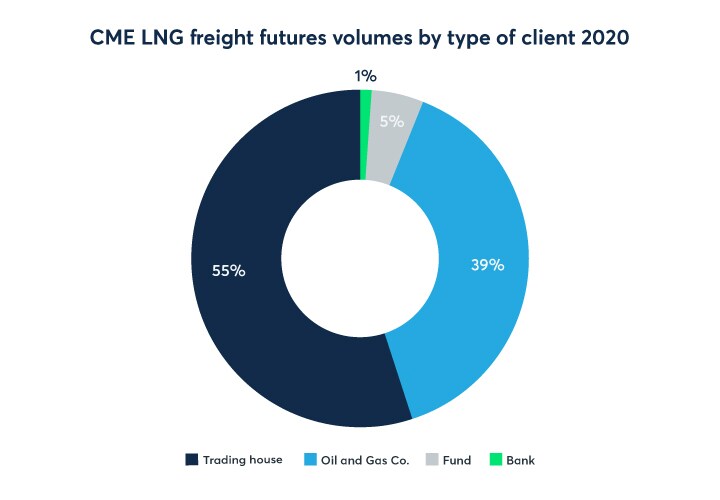

The bulk of LNG Freight futures trading volume in 2020 came from trading desks of oil and gas companies as well as commodities trading houses. The latter category is playing an increasing role in LNG trading by taking positions in the physical market. At the same time, trading houses are key liquidity providers in the derivatives market. A handful number of banks working as hedge providers for some of their clients have as well been actively trading NYMEX LNG Freight futures in 2020.

The latest CME Group LNG Freight futures contracts[1] are based on LNG vessels that use part of the boil off as the bunker fuel. This mirrors a trend that has been growing in the LNG market with additional vessels using increasing volumes of LNG. The use of boil off gas as fuel for propulsion and electricity generation on board instead of marine distillates or marine fuel oil makes the LNG fleet cleaner than other shipping in terms of carbon dioxide emissions. Firms engaged in lower carbon-based products also helps to support the broader ESG mandates, which is a growing industry trend across the broader energy market.

The case for hedging LNG freight:

Since their initial listing, CME Group NYMEX LNG Freight futures have been actively traded by firms willing to manage this risk.

{kind=link}

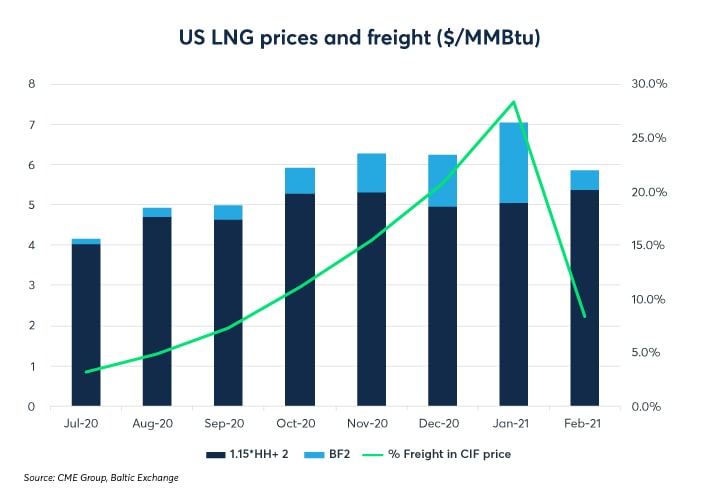

LNG freight costs rise to 30% of LNG cargoes

LNG freight costs represent a high share of the delivered price for LNG compared to other energy products such as crude oil or refined products. LNG freight is a volatile market which brings additional complexity to the traders when making key decisions around what arbitrage opportunities may exist including how to source the right cargoes and ensure they are delivered in a cost-effective manner to the intended destination.

In the LNG market, the charter cost per LNG cargo has risen to around 25-30% and this is a major factor that is considered when deciding to hedge the freight costs in the LNG trade. In a six month period, the freight cost as a percentage of the LNG cargo has risen from around 5% to just under 30%. This compares to the crude oil market where the cost of chartering compared to the crude oil cargo cost is less than 5% but trading volumes on key routes such as Middle East to Asia remain very actively traded. Across the freight markets, the inelasticity of the supply side (the delivery of new vessels and the scrapping of old ones) is a major contributing factor to the volatility in the price. This is particularly true in LNG freight. Additionally, it is worth noting that LNG production is incremental with new additional capacity only added when new liquefaction trains are commissioned.

{kind=link}

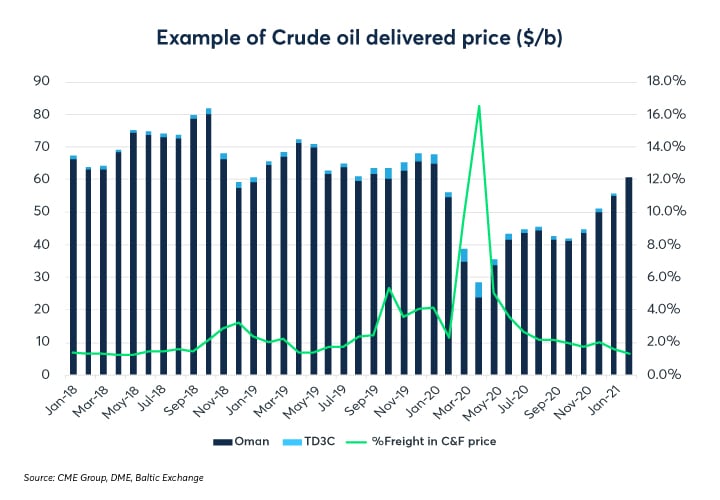

The chartering cost expressed as a percentage of the cost of a cargo in any commodity can increase or decrease over time. In the case of crude oil, this has happened on a several different occasions. Firstly, in late 2019 when several VLCC’s were essentially banned from the market by US sanctions, or more significantly in the first quarter 2020, when spot prices for crude oil fell sharply due to the COVID-19 pandemic. Traders then rushed to book cargoes to store oil and benefit from the contango structure in the market where nearby prices trade at steep discounts to the deferred or forward month prices. Similar instances can also occur in other commodities, such as LNG, which increases the potential demand for hedging.

{kind=link}

CME Group’s global LNG coverage

Our Freight futures are based on the Baltic Exchange suite of indices for three major LNG routes for the Pacific basin, Atlantic basin, and Inter-Pacific basin respectively. Each route being under a constantly updated methodology. To further support the market, CME Group will list three Baltic LNG Freight Futures contracts on March 22, 20211 that reflect the growing use of the boil off from LNG as a bunker fuel.

The Baltic indices are widely acknowledged by the industry to be a key benchmark. Key players across the LNG industry have used the derivatives and brokers have played an important role in facilitating these trades. LNG freight sits alongside other key energy benchmarks for futures and options such as NYMEX Henry Hub, JKM, JCC, Dutch TTF, and UK NBP to allow firms to manage price risk amidst an increasingly volatile market. The LNG Freight Futures are available for trading up to three years forward. More specifically the three references and Baltic Exchange current methodology are:

- Daily rate in USD ($/day)

- 91,500 mt dwt TFDE propulsion

- 160,000 cbm capacity

- Basis delivery cold, ready to load

- 0.1% boil off

- Max age 20 years

| Round voyage | Gladstone / Tokyo | Sabine Pass / UK – continent | Sabine Pass / Tokyo via Panama | |||

| Delivery Gladstone, loading 25-40 days from index date, for a derived round voyage via Tokyo of 23 days duration, with redelivery Gladstone, based on daily hire and lumpsum assessments with 1.25% total commission. | Delivery Sabine, loading 25-40 days from Index date, for a derived round voyage via Isle of Grain of 29 days duration, with redelivery Sabine, based on a daily hire and lumpsum assessments with 1.25% total commission | Delivery Sabine, loading 25-40 days from Index date, for a derived round voyage via Tokyo of 54 days duration (routing via Panama Canal), with redelivery Sabine, based on daily hire and lumpsum assessments with 1.25% total commission. | ||||

| Original | New | Original | New | Original | New | |

| Combustion | Marine Fuel mode on laden and ballast | Gas mode on Laden and Ballast at Boil Off Rate | Marine Fuel mode on laden and ballast | Gas mode on Laden and Ballast at Boil Off Rate | Marine Fuel mode on laden and ballast | Gas mode on Laden and Ballast at Boil Off Rate |

| Knots/day |

|

|

|

|

|

|

| Port consumption |

|

|

|

|

|

|

| Assessment | BLNG1 | BLNG1g | BLNG2 | BLNG2g | BLNG3 | BLNG3g |

| Futures contract | BF1 | BL1 | BF2 | BL2 | BF3 | BL3 |

*For freight bunkering with marine fuels the round voyage time is 1 day less for each route.

Broader adoption of spot contracts boosts demand for LNG

The LNG market has undergone significant changes over the past few years. Most notably has been the wider adoption of spot and short-term contracts (up to four years ahead). In 2019, a total of 120 million tons of LNG or 34% of the global trade was transacted on this basis2 compared to 28% in 2016. There are currently 21 exporting countries for LNG and around 40 countries that can receive LNG. This represents a sizeable increase on 2011 levels where only around 25 countries had any regasification terminals.

Whilst there have been several LNG carriers commissioned since 2018, additional ships are needed to support the growing trade and the current order book suggested strong deliveries out to 2023. All these factors contribute to a more active and complex LNG shipping market where freight rates have always been volatile

US LNG freight flows to Asia are robust

LNG freight assessments are based on round voyage (RV), composed of the laden journey from loading port to destination and the ballast trip to return (theoretically) to the original point. In the case of LNG vessels, they return empty after discharging the LNG at a receiving terminal and ballast elsewhere to re-load with another LNG cargo.

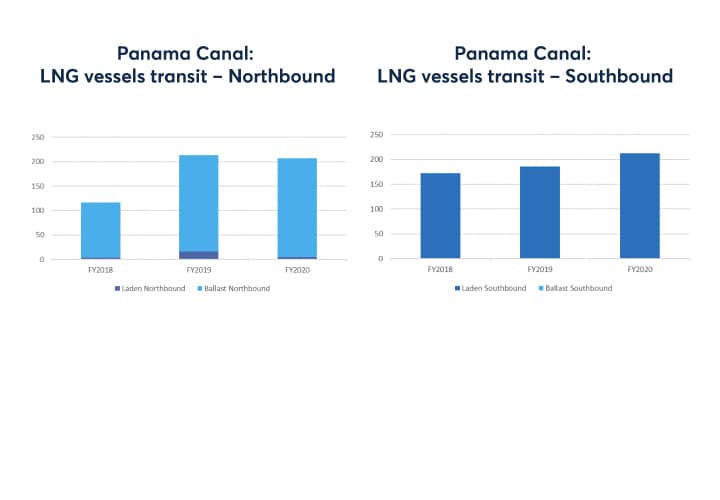

The Panama Canal provides a perfect illustration of this (almost) one-way traffic.

{kind=link}

Source: Panama Canal Authority. FY: October 1 to September 30.

This graph clearly shows that in 2020 all cargoes leaving the US. and exiting via the Panama Canal southbound are leaving full but for the return leg northbound, ships are largely ballasting with no cargo onboard. LNG traffic has been increasing via the Panama Canal (to Asia) since 2016 following the commissioning of Cheniere’s Sabine Pass terminal. According to the Panama Canal Authority, containerships, dry bulk, and chemical tankers represent more than half of the traffic, followed by liquefied petroleum gas (LPG) carriers and liquefied natural gas (LNG) carriers.

According to S&P Global Platts, a total of 58 LNG vessels transited the Neopanamax locks in January 2021, surpassing the prior record of 54 vessels in January 20203. From the perspective of the LNG shipping market, the importance of the maritime route via the Panama Canal is growing. The IGU estimated in its 2020 World LNG report that a total of 5,701 of LNG trade voyages were completed in 2019, an 11% increase compared to the 2018 level of 5,130 voyages4. The volume of LNG carriers exiting the Panama Canal to Asia are increasing year on year and are expected to continue to do so in the years ahead.

More than 90 percent of the LNG world's fleet can now transit the Panama Canal, which opened the doors to a new market and allows LNG traders to send US natural gas to Asia at competitive prices. The LNG freight route BLNG3 and BLNG3g (LNG fuel) futures provide unique derivatives instruments for this maritime route.

CME Freight futures a benchmark for broader LNG shipping

The three Baltic routes listed on CME play the role of benchmark for major LNG flows.

Benchmark routes that can served as the floating rate reference in freight agreements. Benchmarks allow as well to aggregate interests in the derivative market on a limited number of routes, which in turn helps building liquidity.

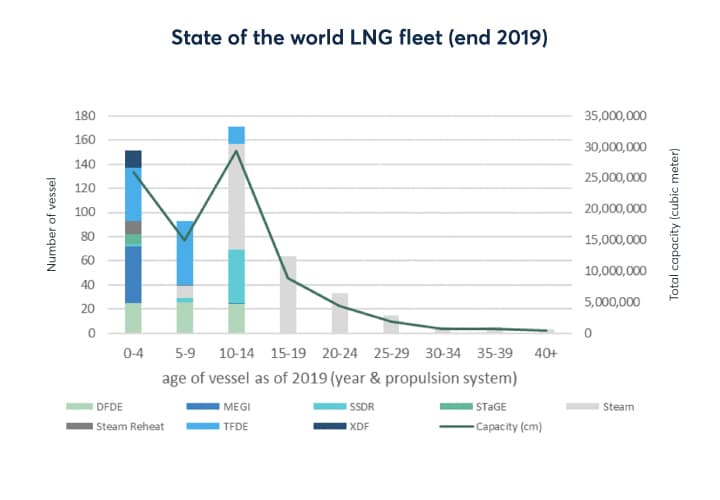

While Qatar remains a vital source of supply, the extensive use of its own fleet of super carriers (Q-Max and Q-Flex), term contracts based on a delivered-ex-ship basis, reduce the interest of freight indexation and hedging for vessels out of the Middle East. Most of conventional LNG vessels have dimensions fitting the Panama Canal new standards (Neopanamax). Carriers with 160 to 180 thousand cubic meters capacity seem to be the norm in the order book. In term of propulsion, steam engines used to be the norm of the industry but most of the new vessels commissioned in the past ten years use more efficient propulsion systems like Dual- and Tri-Fuel Diesel Electric (DFDE, TFDE) able to used boil-off gas such as LNG as a bunker fuel. The Baltic Exchange rates reflect assessments for TFDE propulsion vessels, under 20 years, with a capacity of 160,000 cubic meters. These vessels are typically more efficient and are commonplace in the younger fleets (below 20 years old). Charter rates for the more efficient ships tend to be higher than those with older propulsion technology. Using the futures, traders can typically offer these more efficient ships and apply a market premium which reflects the greater efficiency of the vessel.

{kind=link}

The LNG freight market is continuing to evolve, and the futures markets are helping to support the broader development of the market. The rising cost of LNG freight as a percentage of the total LNG cargo is pushing more companies to look at hedging the cost of freight, in a similar way to developments we have seen in the dry freight markets. With LNG is becoming a bigger feature of the freight market in terms of bunker fuels, the growth in futures based on the LNG indices is expected to increase.

References

- https://www.cmegroup.com/content/dam/cmegroup/notices/ser/2021/02/SER-8704.pdf

- GIGNL Annual Report 2020 https://giignl.org/sites/default/files/PUBLIC_AREA/Publications/giignl_-_2020_annual_report_-_04082020.pdf

- https://www.spglobal.com/platts/en/market-insights/latest-news/natural-gas/020321-panama-canal-sets-new-monthly-record-in-january-for-lng-transits-operator

- IGU 2020 LNG Report https://www.igu.org/app/uploads-wp/2020/04/2020-World-LNG-Report.pdf