{kind=link}

Will a Sino-U.S. Trade War Impact Grain, Meat Markets?

With China threatening to retaliate against U.S. agricultural producers after the White House announced $50 billion in tariffs, it’s a good time to evaluate how China influences agricultural prices – both directly and vicariously. In a direct sense, China is primarily a buyer of U.S. soybeans – imports it could replace with supplies from Argentina and Brazil. It is also an importer of U.S. wheat, which it could find in Russia and Ukraine. The U.S. in no longer a big exporter of corn to China but it does export a great deal of pork and, increasingly, beef.

To the extent that China retaliates against the U.S. by imposing tariffs on agricultural goods, it will disadvantage U.S. producers to the benefit of their foreign competitors. That said, agricultural goods are to a large extent fungible. If China reduces imports from the U.S., it will have to increase imports from elsewhere. If other countries increase their exports to China, they won’t be able to export as much to other markets, which, in turn, creates an opportunity for U.S. farmers to send their goods elsewhere. As such, the overall impact on prices may not be as dramatic as many fear – although it likely won’t be positive either.

China’s biggest influence on agriculture is indirect. As we discussed in our previous paper, China’s pace of economic expansion exerts an enormous influence on the prices of industrial metals and energy products. By extension, it also influences the value of currencies of commodity exporting nations. It turns out that China’s growth rate also has a similar but somewhat delayed impact on the prices of many agricultural goods such as corn, soybeans, soybean oil, rough rice and wheat but for reasons that are somewhat different than one might think.

That China would influence metals prices is obvious: the country consumes 40-50% of most of the world’s industrials metals. By contrast, China consumes only about 7% of the world’s crude oil. Even so, China’s growth influences crude oil prices mainly because of crude oil’s extreme demand-and-supply inelasticity: small fluctuations in demand and supply have outsized impacts on prices. China’s direct impact on agricultural prices has, of course, to do with its massive population (4x that of the United States). China consumes about 20% of the global food supply.

While China’s tremendous economic growth has increased its calorie count from 2,500 per day in 1990 to around 3,200 per day in 2017, on a year-on-year basis, fluctuations in China’s growth rate have only a weak correlation with actual changes in food consumption (Figure 1). This is true both of China’s official GDP measure as well as the Li Keqiang alternative measure of growth.

Figure 1: Growth Rate of Agricultural Consumption

{kind=link}

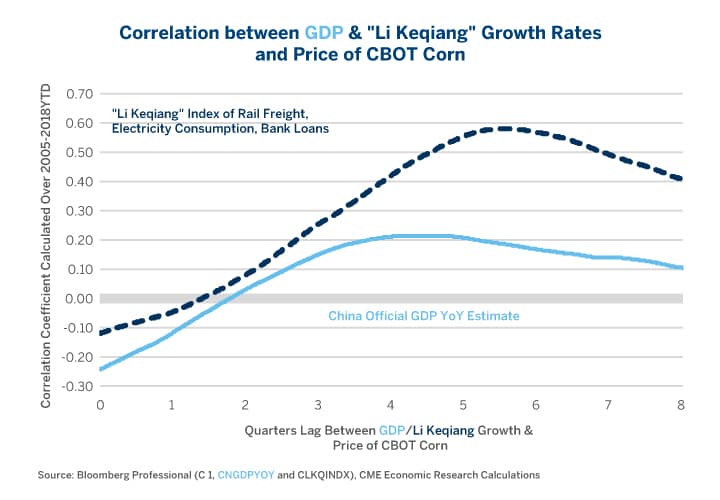

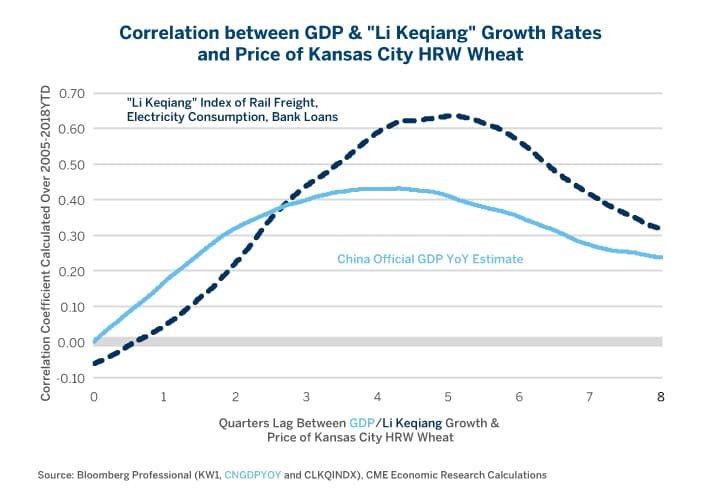

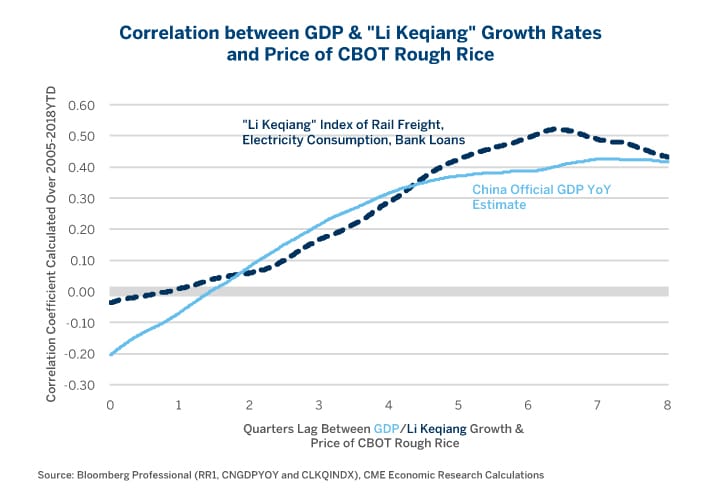

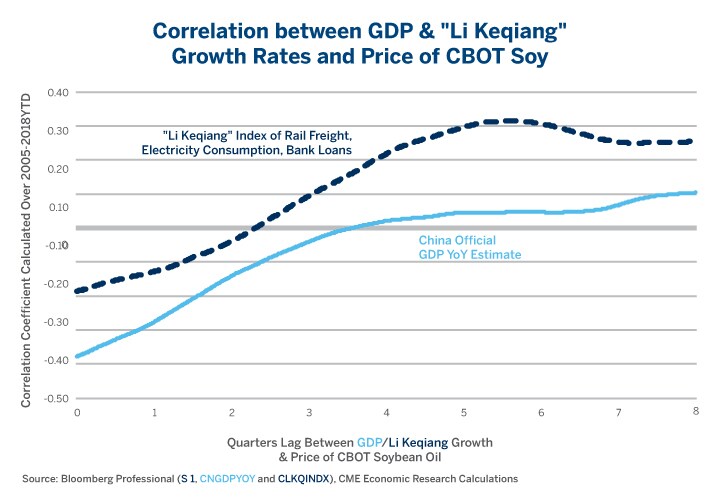

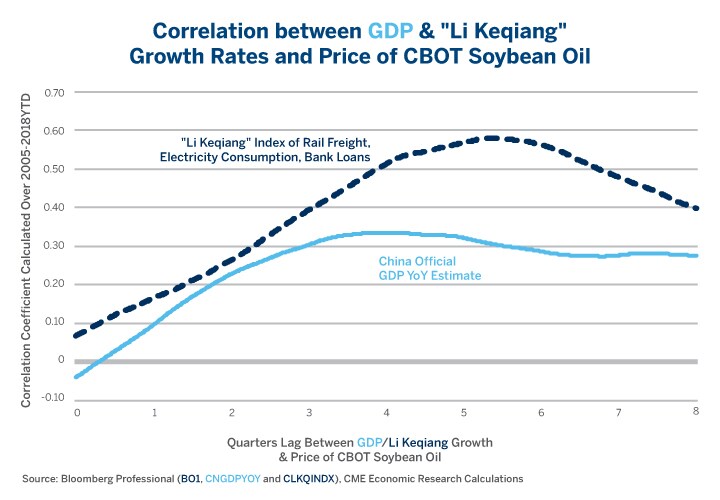

So, how and why does China’s growth influence agricultural markets if Chinese consumers don’t increase or decrease their food demand in response to short-term fluctuations in the pace of economic growth? The answer appears to lie in China’s impact on currency markets, and especially the currencies of major agricultural exporters such as Argentina, Brazil, Canada and Russia. Just as is the case for metals, energy and currencies, the Li Keqiang proxy measure of China’s GDP growth rate has proven to be a much better indicator of China’s influence on agricultural goods prices than China’s official GDP. This is evident for corn, wheat, soybeans, soybean oil and rough rice prices (Figures 2-16).

The Li Keqiang index measures changes in the volume of rail freight, electricity consumption and bank loans. While there are those who say that the Li Keqiang index no longer works as a proxy of China’s official GDP, what we are most interested in is the health of China’s industrial economy and its impact on currency and commodity markets.

What is curious is that changes in China’s growth rate appear to have their biggest impact on agricultural goods prices 5-8 quarters into the future. So, in other words, a slowdown in China in early 2018, might not negatively impact the prices of agricultural goods until 2019 or even early 2020. The transmission mechanism doesn’t appear to involve the Chinese eating less or more. Rather, when China’s growth accelerates (decelerates), the prices of energy and metals tend to rise (fall), which in turn leads the currencies of other major agricultural producers to rise (fall) in relation to the U.S. dollar. A stronger Brazilian real, Canadian dollar and Russian ruble will make their farmers less competitive and will raise their cost of production from a USD perspective. At some point down the road, often about 1-2 years later, this boosts agricultural goods prices. Of course, the opposite happens when China’s growth slows, weakening energy and metals prices and sending the Canadian dollar, the Brazilian real and the Russian ruble lower. The same pattern could assert itself in the future with the Argentine peso, which until recently was on a moving peg versus the U.S. dollar.

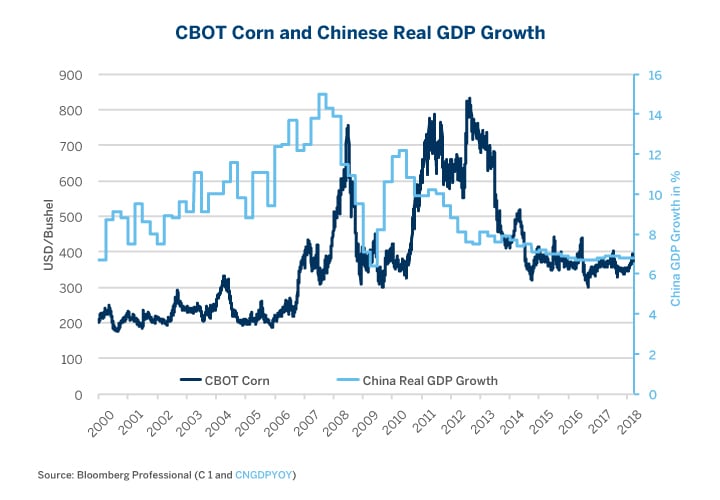

Figure 2: Moves in Corn Prices have Often Lagged Changes in the GDP Growth Rate

{kind=link}

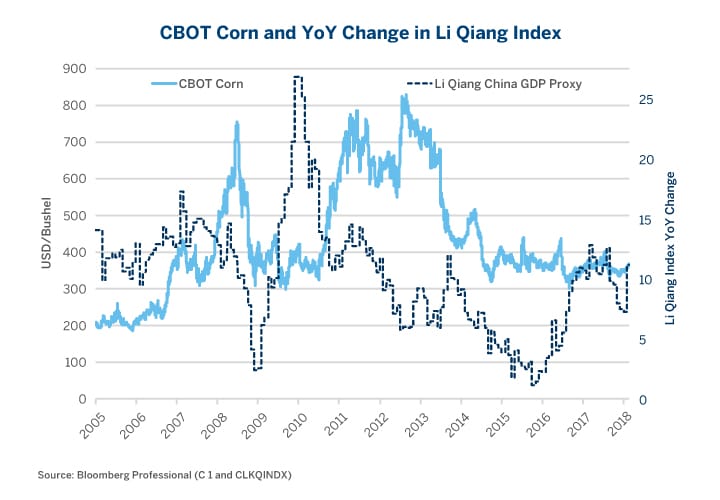

Figure 3: The Li Keqiang Index Correlates More Strongly with Corn Prices Than Official GDP.

{kind=link}

Figure 4: Li Keqiang Dominates Official GDP Insofar as Correlation with Future Corn Prices is Concerned

{kind=link}

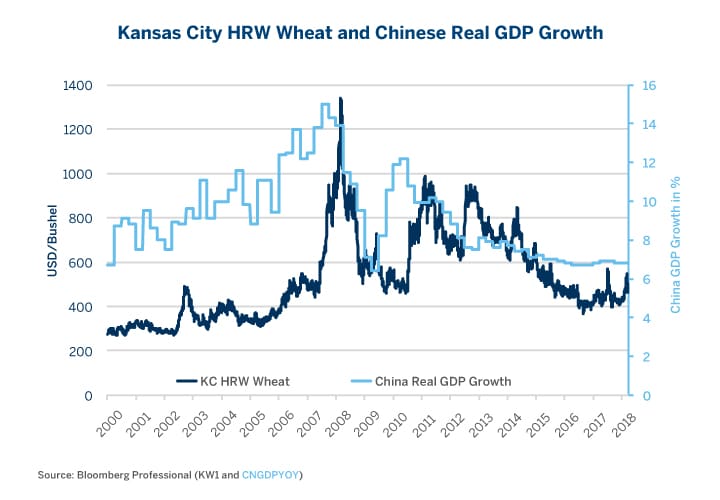

Figure 5: China’s Official GDP Versus Chicago Wheat

{kind=link}

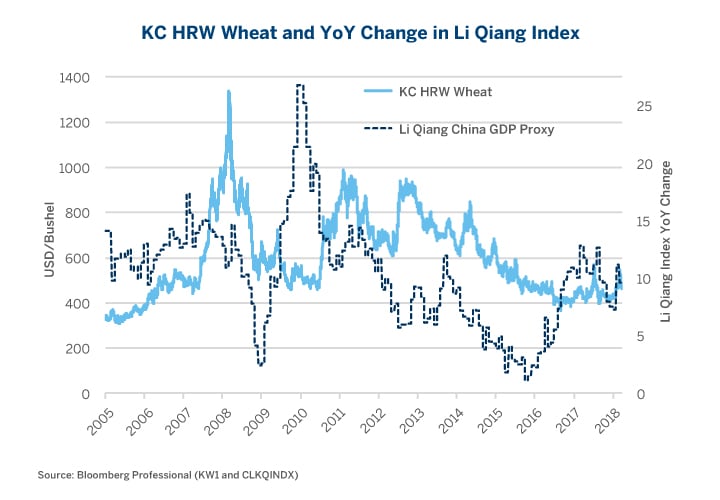

Figure 6: Li Keqiang Index Versus KC HRW Wheat

{kind=link}

Figure 7: Li Keqiang Does a Better Job than GDP of Explaining Future Movements in Wheat Prices

{kind=link}

Figure 8: Rough Rice and Chinese GDP growth

{kind=link}

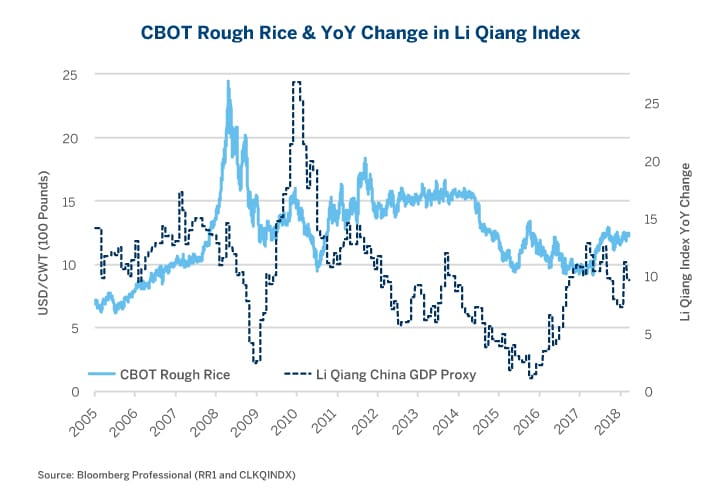

Figure 9: Rough Rice Often Lags Growth in the Li Keqiang Index

{kind=link}

Figure 10: Li Keqiang Does Slightly Better at Forecasting Rice Prices 5-8 Quarters Out Than Official GDP

{kind=link}

Figure 11: Official GDP and Soybeans

{kind=link}

Figure 12: Li Keqiang Index and Soybeans

{kind=link}

Figure 13: Li Keqiang Index and CBOT Soybeans

{kind=link}

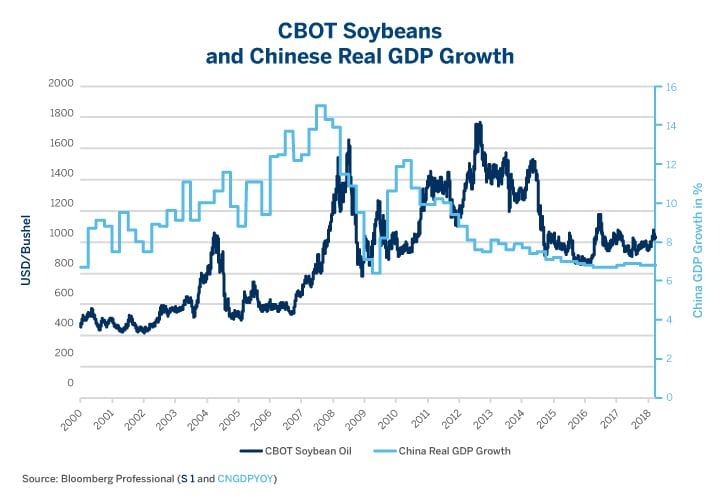

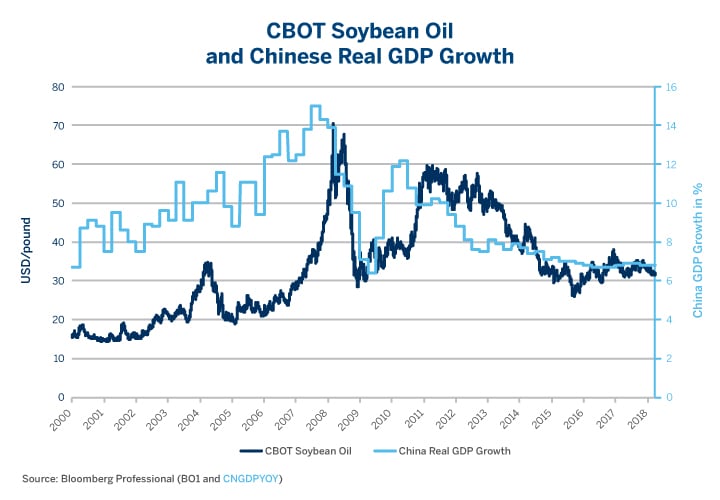

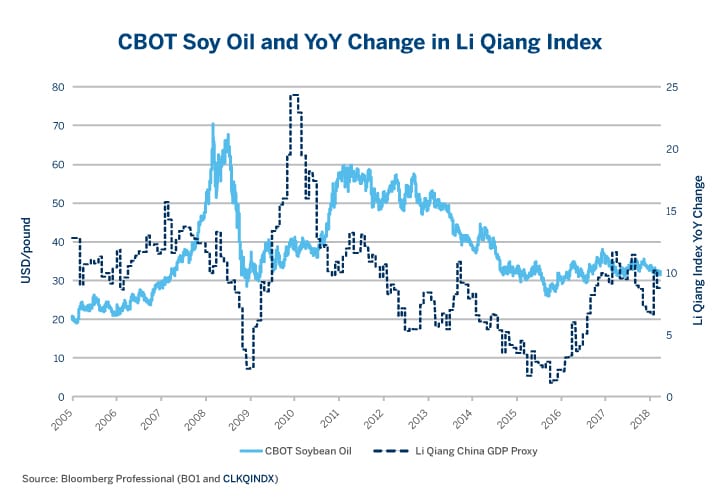

Figure 14: Soybean Oil and Chinese Official GDP Growth

{kind=link}

Figure 15: Soybean Oil Versus Li Keqiang Index

{kind=link}

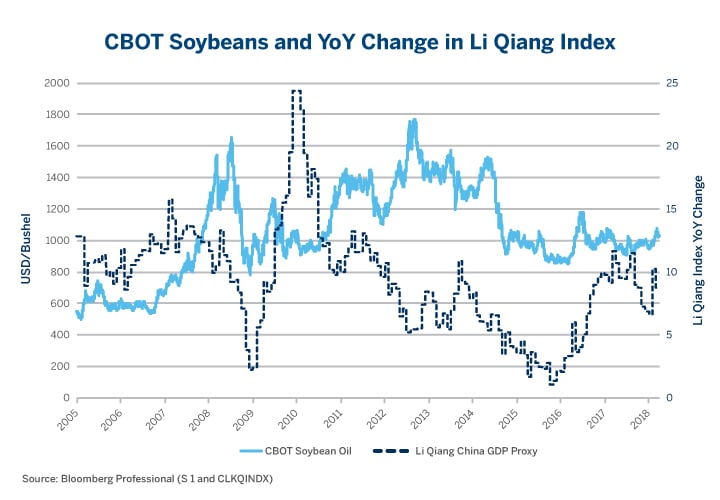

Figure 16: Li Keqiang has Proven a Strong Indicator of Past Movements in Soybean Oil Prices

{kind=link}

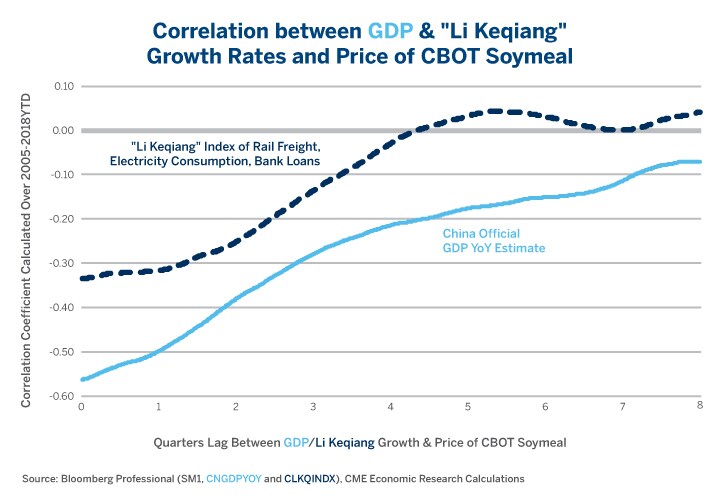

Figure 17: Soymeal is Alone Among Crops in Not Showing a High Correlation to GDP or Li Keqiang

{kind=link}

Only soymeal (Figure 17) fails to show a high correlation with either GDP or the Li Keqiang index and appears to be little influenced by Chinese economic growth.

Outlook

China’s yield curves have gone flat during the past year and this, in turn, is a harbinger of both slower official GDP growth and slower growth from the perspective of the Li Keqiang index. In fact, growth has already begun to slow according to the latter measure from over 15% in mid-2017 to below 10% by early 2018. If the yield curve maintains its past predictive power, this might imply further slowing for growth throughout 2018.

If the past is any guide, slower Chinese growth in 2018 might have little immediate bearing on the prices of agricultural goods but could impact them negatively as we move into the end of the decade if a Chinese slowdown does indeed impact metals, energy and commodity currencies negatively as well. It’s a lot of “ifs,” but as observers of both China and agricultural goods markets, we would pay especially close attention to the Li Keqiang GDP proxy, which appears more adept at forecasting future movements in agricultural goods prices than official GDP – as is the case for nearly all of the goods, currencies and interest rate products to which we have correlated it.

Hedging Trade Tensions

China is a major importer of U.S. soybeans, pork and, increasingly, beef. Sales of these commodities could be affected if trade skirmishes between the U.S. and China become an intractable dispute. Hedge against the uncertainty and potential volatility with the suite of CME Group Agricultural products.