{kind=link}

U.S. Pullout of Iran Nuclear Deal: What Next for Oil, Business?

The U.S. announced on May 8, 2018, its withdrawal from the Joint Comprehensive Plan of Action (JCPOA) – aka, the Iran nuclear deal. In the week prior to this decision, expectations were rising that the U.S. would pull out of the deal. A variety of European leaders flew to Washington and lobbied the U.S. Administration to remain in the deal. French President Emmanuel Macron flew into Andrews Air Force Base (technically Joint Base Andrews), was received with a State dinner, and failed to convince the Republican Administration to change its mind. German Chancellor Angela Merkel arrived at Dulles International Airport, received a less formal welcome, and also failed to convince the U.S. to change its mind. Even UK Foreign Secretary Boris Johnson, a supporter of the U.S. President, showed up in Washington to make the case for staying in the Iran deal. He even appeared on Fox News and talked to the Republican base, to no avail.

Within hours after the U.S. decision to withdraw was announced, the leaders of France, UK and Germany put out a joint statement, which was quite emphatic in its opposition to the U.S. decision:

“It is with regret and concern that we, the leaders of France, Germany and the United Kingdom, take note of President Trump’s decision to withdraw the United States of America from the Joint Comprehensive Plan of Action… According to the IAEA (International Atomic Energy Agency), Iran continues to abide by the restrictions set out by the JCPOA, in line with its obligations under the Treaty on the Non-Proliferation of Nuclear Weapons. The world is a safer place as a result. Therefore we, the E3, will remain parties to the JCPOA. Our governments remain committed to ensuring the agreement is upheld, and will work with all the remaining parties to the deal to ensure this remains the case, including through ensuring the continuing economic benefits to the Iranian people that are linked to the agreement. [emphasis ours, Source: https://www.diplomatie.gouv.fr/en/french-foreign-policy/disarmament-and-non-proliferation/events/article/jcpoa-joint-statement-by-france-the-united-kingdom-and-germany-08-05-18]

What are the impacts on the oil market, Mideast peace, and global trade? For our discussion, we have opted for a question and answer format:

Q1 What does the U.S. withdrawal from the Iran nuclear deal mean for the supply of oil to world markets in the short run?

Probably not much initially. Some analysts suggest that Iranian oil production will be curtailed by new U.S. sanctions to the tune of 500,000 to 1 million barrels a day. This is not likely this time around. Iran will probably continue to produce oil at a full pace and find willing buyers, although it may have to provide some discounts.

Prior to the deal, sanctions were imposed on Iran by the United Nations (UN), Europe, and the U.S. This time around, only the U.S. is likely to impose sanctions, and any U.S. unilateral sanctions will be disputed and vigorously opposed in international legal forums by France, UK, and Germany, as well as by the UN.

Moreover, China, an oil importer, was an initial signer of the deal, and China considers the terms of the deal to still be in place, just without U.S. participation. This means that China may decide to buy more oil from Iran, possibly under discounted long-term contracts. This would increase China’s influence in the region, circumvent any U.S. sanctions, and mean that China might buy less oil from U.S. shale supplies being exported from the Gulf of Mexico.

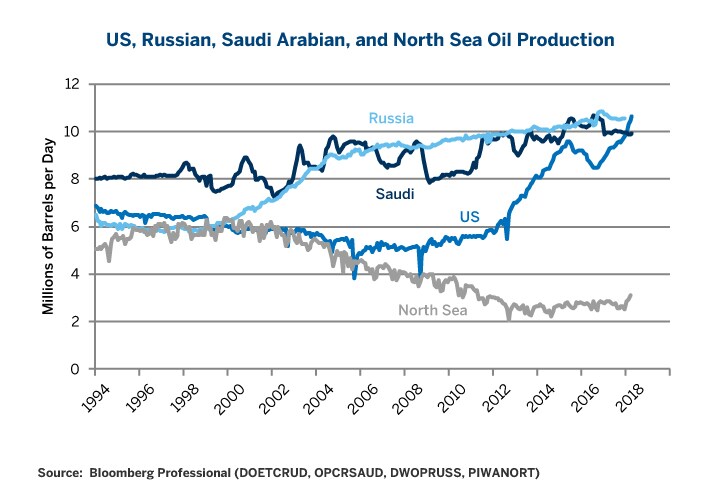

Figure 1: Oil Production Trends

{kind=link}

And, very critically, the higher spot prices of oil are highly likely to lead to increased production from Russia and Saudi Arabia. They have been curtailing production to push prices higher, and their objectives have been achieved. On net, with more Chinese purchases of Iranian oil, and more production from Russia and Saudi Arabia, not to mention U.S. shale, global oil production is headed higher, not lower.

There is a big “if” to consider. If the supply of oil is disrupted in any way, it will probably be because of military action in the Mideast and not because of newly re-imposed U.S. sanctions on Iran.

Q2 If the supply of oil is not immediately impacted, why are oil prices rising?

The concern for oil market participants is the future potential for oil supply disruptions in the Mideast. As a result, a “Mideast risk premium” of around $10/barrel appears present in the price of oil, and this risk premium could easily go higher. The U.S. withdrawal from the Iran nuclear deal works to increase, at least in the short-term, market participants’ perceived risk of military conflict in the Mideast that could involve both Iran and Saudi Arabia. While military actions remain a low probability event; the impact factor on oil prices is extremely high.

Q3 How will the U.S. sanctions work without global support?

For sanctions to work well they require global support. Prior to the Iran nuclear deal, the sanctions were clearly inflicting considerable pain on the Iranian economy. These sanctions were fully supported by the UN and Europe along with the U.S. While the U.S. has announced it will re-impose sanctions, it is highly unlikely to have any multilateral support at all. France, UK, and Germany have made it crystal clear that they consider the deal, even without the U.S., to be viable. Indeed, in their joint statement, they went out of their way to explicitly state that they will work together to make sure Iran receives the economic benefits it was promised for complying with the nuclear deal. China and Russia, also signed the deal, and indicated they consider the deal to remain in force. This means, that these countries do not plan on supporting any U.S. unilaterally imposed sanctions, and that they will support commercial activities between Iran and their countries.

The real legal battle over U.S. sanctions will be the issue of whether the U.S. can force non-U.S. companies to comply with U.S. unilateral sanctions by threatening the ability of these companies to do business in the U.S. U.S. companies simply do not do enough direct business with Iran to make any sanctions on only U.S. companies meaningful to Iran. To have an impact, the U.S. must impose its sanctions on non-U.S. companies – from France, UK, Germany, the rest of Europe, China, etc.

The anger in Europe over the U.S. moves to withdraw from multi-lateral agreements is very deep. European governments, despite Brexit, are committed to multi-lateral approaches to dealing with global issues. The U.S. withdrew from the Paris Accord on the environment, pulled out of the Trans Pacific Partnership, seems ready to exit the North American Free Trade Agreement (NAFTA) in short order, the U.S. threatened tariffs on steel and aluminum on European countries in the name of U.S. national security, and now the U.S. withdrew from the Iran nuclear deal. This U.S. withdrawal from the Iran nuclear deal may be the straw that breaks the camel’s back in terms of European governments’ willingness to support any U.S. sanctions or future military operations. While time will tell, at least for now, U.S.-European relationships are at a very low point.

Q4 What are the consequences for the US economy?

The main impact on the U.S. economy will be rising gasoline prices at the pump for consumers. $4/gallon prices at the pump may arrive on average across the nation by the end of the summer driving season. If retail gasoline prices head for $5/gallon will depend on whether oil prices move even higher.

We note that the Federal Reserve (Fed) typically looks through any temporary volatility in energy and food prices and focuses on the core inflation rate. Core inflation is inching higher. Based on the federal funds futures market, the Fed is on track for more rate rises, with the next coming in June 2018.

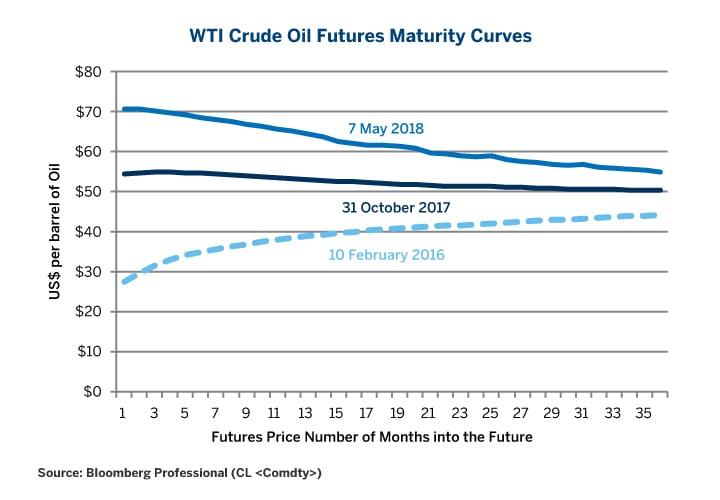

Q5 Is backwardation, when spot oil prices are higher than long-term prices, here to stay?

Currently, the main cause of the backwardation in the oil futures maturity curve is due to fears of market participants concerning the possibility that tensions between Iran and Saudi Arabia could lead to military action. The battlegrounds might be Syria or Yemen now, yet market participants fear an expansion of hostilities that could impact oil supplies. Hence, the spot and near-term futures prices for oil reflect a heightened “Mideast Risk Premium”. Backwardation is likely to persist if fears of Mideast tension erupting in to military action remain on high alert. If the U.S. makes progress on negotiating a new deal with Iran, then spot prices would fall and backwardation might disappear.

Figure 2: Oil is in backwardation

{kind=link}

Q6 What does persistent backwardation mean for US shale oil production?

U.S. shale oil producers cannot turn on and off production with a switch, so it is not the front-end spot price that matters. Shale producers will be looking to the six-month to 24-month futures prices as part of their assessment of whether to put new rigs into operation. With backwardation, these prices are well below the headline spot price for oil. Still, the prices in the longer-term futures maturities offer excellent incentives for expanding U.S. shale oil production. Our estimate is that U.S. oil production could top 12 million barrels a day by the end of 2019 – putting the U.S. on par with Russia and Saudi Arabia as the three top oil producers in the world.

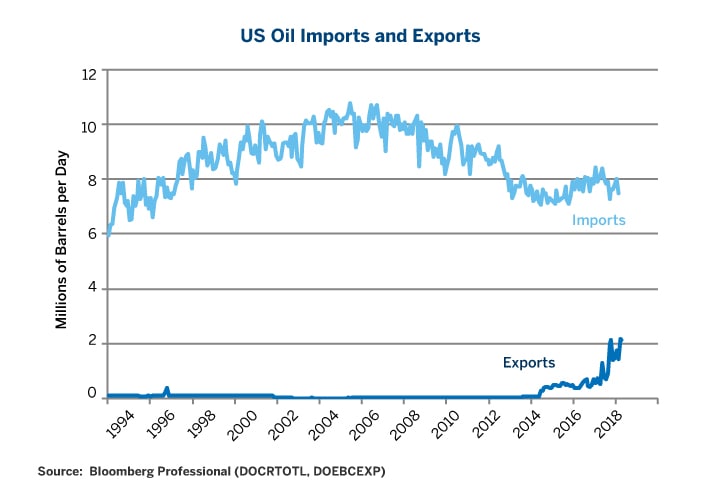

Q7 The US is now an exporter of oil, how does this impact global oil prices?

The repeal of the U.S. ban on oil exports has allowed excess U.S. shale oil production to be loaded on ships and sold to Europe and Asia. U.S. exports are now 2 million barrels a day and rising. (The U.S. remains a big oil importer.) The ability of the U.S. to export oil strengthens the connections with other oil benchmark around the world, based in part on spot shipping costs. While shipping costs are notoriously hard to estimate, a $4-to-$6/barrel cost is plausible, depending on distance, term of contract, size of ship, speed of ship, etc. This puts a soft cap on the spread between WTI and North Sea Brent prices. We say a soft cap because the spread could widen by more than $6/barrel; however, this would put strong incentives in play for more U.S. oil exports.

Figure 3: US exports and imports of oil

{kind=link}

Hedging Iran Uncertainty

The United States has pulled out of the Iran nuclear deal in a move that could have wide-ranging implications for oil markets, trade and the Middle East peace process. Protect your portfolio and hedge the uncertainty with the suite of NYMEX Energy futures and options.