{kind=link}

Hedging the Next Explosion in High-Yield Bond Spreads

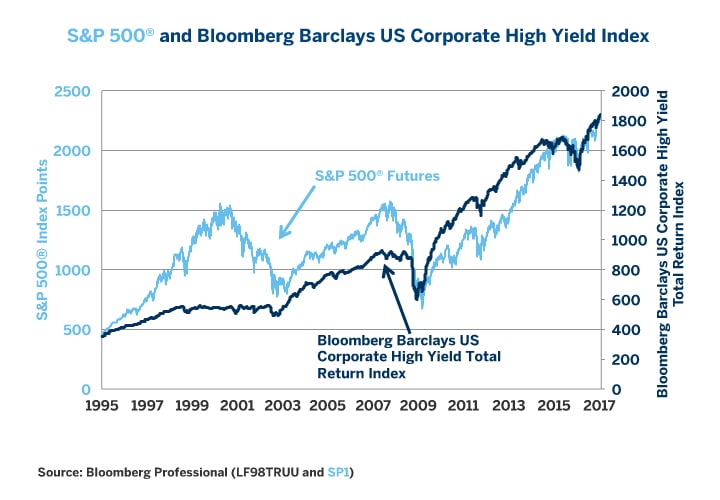

Since they hit bottom in early 2009, the S&P 500® and the Bloomberg Barclays U.S. Corporate High Yield Index have been on a roll. Both are up over 200% from the depths of the financial crisis (Figure 1).

Figure 1: On a Roll, But for How Much Longer?

{kind=link}

When markets are in a secular bull market, hedging against potential downside is costly. Indeed, anyone who hedged either stocks or bonds would have missed out on gains over the past eight years. Bull markets, however, are not eternal. As the current bull market in equities and bonds ages, the risk of a sharp correction or a bear market will begin to increase, as will the temptation or even the necessity to hedge downside exposure.

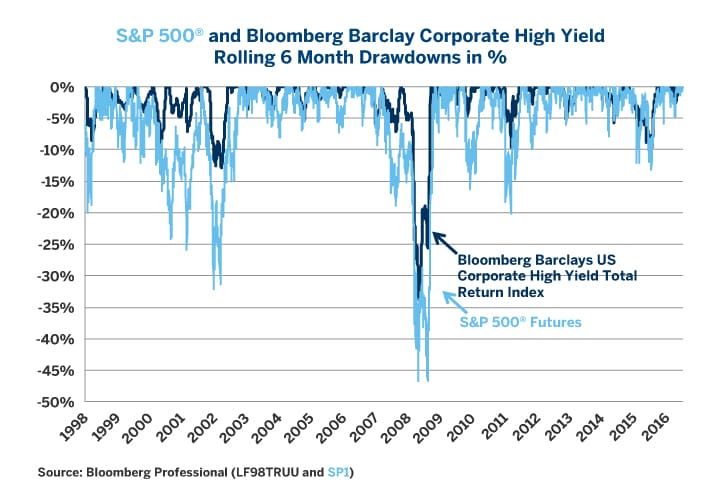

Although the S&P 500® and the Bloomberg Barclays U.S. Corporate High Yield Index are not perfectly correlated, their drawdowns tend to coincide (Figure 2). Since 2002, nearly every sharp sell-off in stocks has coincided with a sharp downward move in the price of high-yield corporate bonds (Figure 2).

Figure 2: Sharp Declines in Stocks Almost Always Coincide with Sharp Declines in Corporate Bonds.

{kind=link}

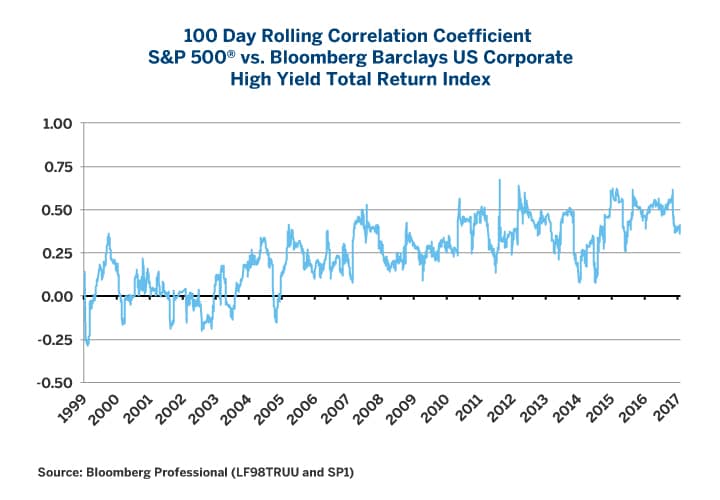

Moreover, the day-to-day correlation between the S&P 500® and measures of corporate bond performance has also risen over the years, perhaps in part because corporate bond markets became somewhat more liquid (meaning a higher degree of trading frequency) between 1999 and 2009. Over the past few years, the equity to high-yield bond correlation has often been in the 0.40-0.60 range (Figure 3), meaning that one could plausibly hedge corporate bond exposure using equity index futures – although not without potentially significant tracking risk.

Figure 3: A Rising but Still Imperfect Correlation Between Stocks and High-Yield Bonds.

{kind=link}

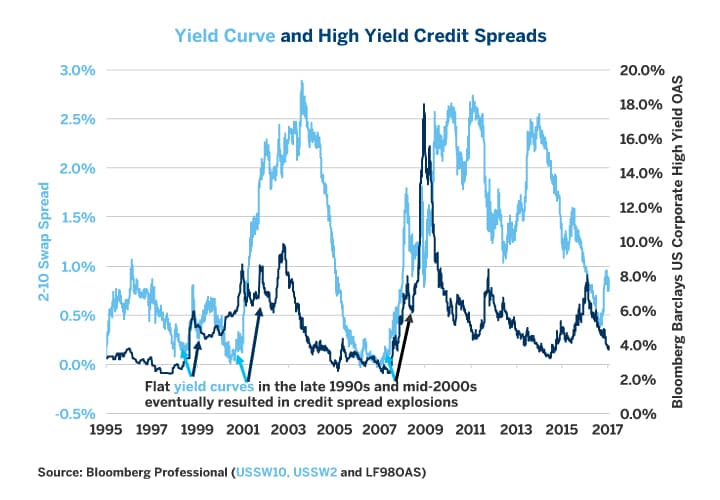

When hedging corporate bond exposures using futures or options, timing is everything. Our research suggests that the probability of a sharp selloff in corporate bonds is not evenly distributed across time. Basically, when monetary policy is very easy – low rates and/or quantitative easing — there is little risk of an explosion in corporate bond spreads over Treasuries. As monetary policy tightens and yield curves flatten, the risk of a sharp drop in the value of high-yield bonds relative to government bonds begins to increase.

Before the financial crisis, the mechanism was fairly simple: when the Federal Reserve (Fed) introduced an easy monetary policy, it held short-term interest rates below the level of longer-term interest rates. This in turns encourages the banking system to lend money. Banks and other lenders can borrow funds inexpensively from the Fed or depositors and then lend the money longer term at higher rates, making money on the yield curve’s steepness as well as by charging more on loans to lower-grade borrowers. By contrast, when the Fed tightens policy and raises short-term interest rates towards the level of long-term interest rates, the banks and other lenders can no longer make money from the steepness of the yield curve and over time will begin to reduce access to credit. As access to funds is cut off, some debtors will find it difficult to rollover loans, the economy will slow and defaults and fears of defaults will rise and credit spreads will widen. This has happened three times in the 20 years leading up to the most recent financial crisis:

- The Late 1980s Savings & Loan (S&L) Crisis: The yield curve inverted in 1989 and credit spreads exploded, leading to the collapse of major Wall Street investment banking firm Drexel Burnham Lambert, the worsening of the S&L crisis, and an economic recession in 1990-91.

- The Late 1990s Asian and Russian Crises/Early 2000s Tech Wreck: By 1997, the yield curve had become fairly flat, coinciding with a series of credit events beginning with the collapse of Long-Term Capital Management (LTCM) in 1998 and, after a renewed flattening of the curve in 1999 and 2000, there was a rapid expansion of credit spreads from 2000-2002, coinciding with the 2001 tech wreck recession.

- The Subprime Mortgage Crisis of 2007-08: By 2006, the yield curve had gone flat and by 2007 credit problems related to the housing sector were beginning to appear. Corporate bonds and equities crashed in 2008 as the economy tanked.

Episodes 2 and 3 above are reflected in Figure 4.

Figure 4: Flat Yield Curves Can Eventually Drive Explosions in Credit Spreads.

{kind=link}

Post-financial crisis, most of the mechanisms work as before. The only addition to the mix is quantitative easing (QE), in which the Fed no longer attempts to influence monetary policy by moving short-term interest rates, which are blocked near zero, but rather buys longer-dated bonds in order to inject more money into the system. QE can temporarily flatten yield curves somewhat without creating much risk of a credit-spread explosion. This doesn’t matter much now for a couple of reasons. First, even during the most aggressive stages of the Fed’s QE programs between 2009 and 2014, the yield curve remained fairly steep. Secondly, the Fed ended QE over two years ago and is now back to targeting short-term interest rates.

During 2015 and 2016, the Fed was exceedingly cautious about raising rates with only one 25 basis-point hike each year. As we enter 2017, U.S. monetary policy is still fairly easy and the yield curve is still reasonably steep. This suggests that in the near term there is probably only a low-to-moderate risk of a 1989, 1998 or 2007-style explosion in credit spreads.

If the Fed accelerates its pace of monetary tightening, however, those risks will grow. If and when short-term rates begin to approach the level of longer-term rates, the system will be blinking red for the possibility of a severe bear market in corporate credit.

As such, early 2017 might not be the most propitious time to hedge credit spread exposures using S&P 500® Index futures. However, there are other possibilities. One is to hedge credit exposures by using deep out-of-the-money options on S&P 500®. These are selling at near historic-low prices (Figure 5).

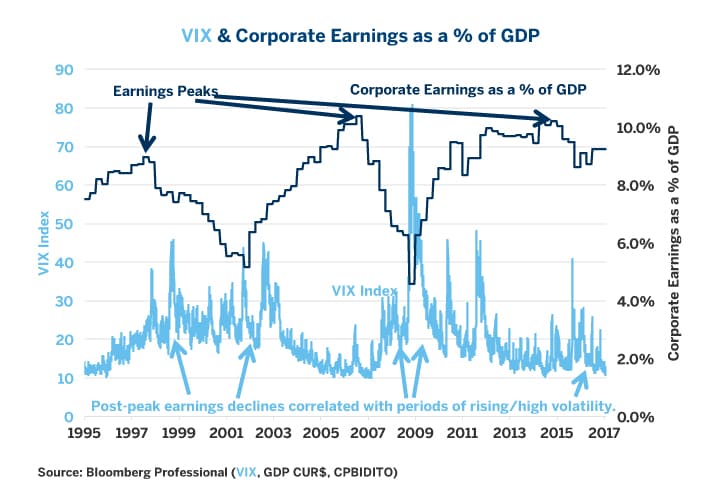

Figure 5: If Corporate Earnings Begin to Fall, Options Prices Might Begin to Rise.

{kind=link}

Note that when corporate earnings fall, as they often do in the late stages of an economic expansion, this can set off a simultaneous rise in the price of both options and credit spreads. For the moment, corporate earnings are around 9.3% of GDP, which is off the highs from 2013 but still close to the historic upper range of around 10.5% of GDP. As the current economic expansion, which began in 2010 continues, it is likely that the labor market will tighten further, putting upward pressure on wages and downward pressure on corporate profits. As this happens, the Fed will likely tighten further and this will eventually lead to rising options prices as well as wider credit spreads and more volatile equity markets, which are more prone to sharp corrections and bear markets. This will be the time when hedging high yield corporate bond exposures through futures may become imperative.

One should also note that not every expansion of spreads can be explained on the basis of monetary policy. Credit spreads grew in 2015 mainly as a result of the collapse in energy prices and concern over energy-specific issuers in the face of low crude oil prices. With the rebound in crude oil, these fears have eased but they could resurface if oil prices fall again. Investors who have exposure to sector- specific corporate bond exposures could look towards E-mini S&P select sector futures and other products to hedge their financial exposure rather than use the broader market indices with the same caveats discussed above: namely, that equity index futures, be they broad or sector specific, have imperfect correlations to movements in the corporate debt market.