Comparing Grain Buying Strategies

{kind=link}

There are many risk management strategies that offer price protection against rising markets for long hedgers, buyers of grain and oilseed products, such as grain processors, feed manufacturers and food companies.

The circumstances for each hedger is different, and their hedging needs are specific to their goals and objectives and the financial status of their business operations, as well as their own level of risk tolerance.

Because of this, there is no one, perfect strategy that will fit all hedgers in all market conditions, nor is there one strategy that an individual hedger will want to employ in every scenario.

The long hedging strategies addressed in this chapter, while among the most common, are not an exhaustive list of all the strategies available. All long hedgers should become familiar with the various risk management alternatives and which ones may work best for their particular needs.

This module will review some long hedging strategies, and compare their pros and cons.

For the purpose of our comparison, we will use the case of a feed manufacturer who is planning to buy corn for his operation later in the year.

Assume that the December Corn futures price is currently $4 a bushel. For the sake of simplicity, we will disregard the issue of the basis and use hypothetical prices for Corn futures and options.

Long Futures Position

The long futures position is the most basic strategy for a grain buyer, providing price protection against the risk of rising prices. Say the feed manufacturer goes long December Corn futures at $4.

The key advantage is that it allows him to lock in the $4 price in advance of the actual purchase. If futures prices rise between buying futures and December, his purchase price is protected. However, this strategy does not allow him to benefit from lower prices if corn prices fall.

Call Options

If the manufacturer would like to protect against rising prices, but still retain the ability to purchase corn at a lower price if futures fall, he may prefer the flexibility of a long call option. For example, buying an at-the-money call with a strike price of $4 for a premium of 30 cents.

Buying the call establishes a maximum, or ceiling, purchase price of $4.30, the strike price plus the premium, while retaining the opportunity for the feed manufacturer to pay a lower net price if the market falls.

As the buyer of the call option, the feed manufacturer will not be required to post a performance bond, but he does pay the 30-cent premium upfront for the protection and opportunity that the call option provides.

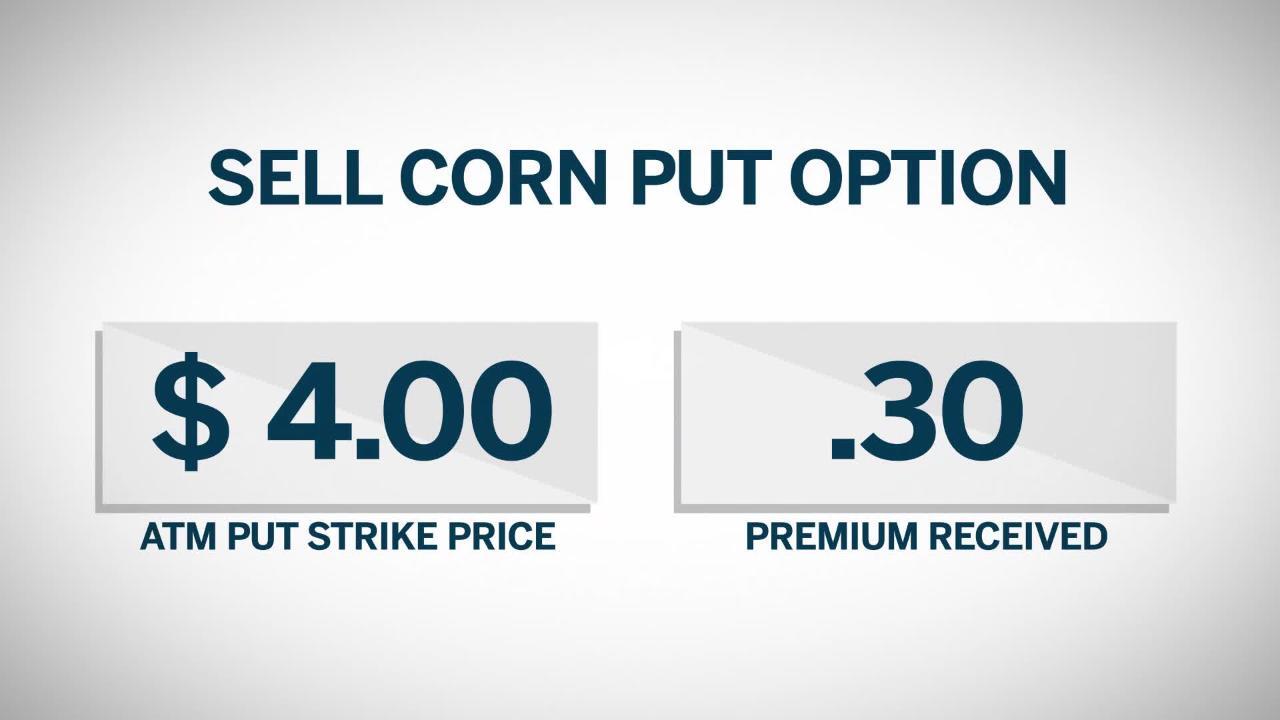

Put Options

In a stable market environment, a short put position may provide the feed manufacturer with the best net purchase price, but it is a riskier strategy. For instance, say he sells an at-the-money corn put option for which he receives the 30-cent premium.

As long as the market actually remains stable, he will retain the 30-cent premium, which will allow him to effectively lower his net purchase price.

However, the effectiveness of this strategy is contingent upon the market remaining stable. The short, put option establishes a minimum purchase price of $3.70, the strike price minus the premium, which limits the feed manufacturer’s ability to participate should prices decline.

Should the corn market increase significantly, his protection against rising prices is limited to the 30-cent premium he received for selling the put option. In addition, as the seller of the put, the feed manufacturer will be required to post a performance bond at the time he sells the option.

Combined Put and Call Options

The manufacturer can also combine a short, put position with a long, call position, which will allow him to establish a buying price range for the corn he needs.

For example, he could buy an at-the-money call option with a strike price of $4 for a 30-cent premium and simultaneously sell an out-of-the-money put option with a strike price of $3.75, for which he receives a premium of 20 cents.

He establishes this position at a net premium of 10 cents: the 30-cent premium he paid minus the 20-cent premium he received.

The long call establishes a ceiling price of $4.10, the $4 call strike price plus the net premium, and the short put establishes a floor price of $3.85, the $3.75 put strike price plus the net premium.

The advantages of this strategy are that it creates a known buying price range; the feed manufacturer knows upfront the maximum, as well as the minimum, price he will pay for his corn. The premium he collects allows him to establish a lower ceiling price level than he would have by simply buying the call option.

However, the disadvantage is that it limits the opportunity of paying a lower price for his corn should the market decline. Also, as the seller of the put option, he will be required to post a performance bond for that side of the trade.

No Trades

Finally, the feed manufacturer has the alternative of doing nothing, the most simplistic, but also the riskiest strategy for a grain buyer. While this may yield the best purchase price if the corn market falls, it provides no protection at all in the event of a market rally.

Conclusion

There are many strategies available to grain buyers to manage risk, involving futures, options, the cash market, or a combination of these, each with their own advantages and disadvantages.

{kind=link}

It is important for hedgers to become acquainted with all of their alternatives and understand when a specific strategy should or should not be used. Remember that a strategy that was effective for hedging one sale, may not be the best choice for the next.

No one can predict the future, but hedgers can take steps to manage it. Using grain and oilseed futures and options allows those who need protection against falling prices to have peace of mind knowing that they have taken steps to manage the price risk associated with selling these commodities.