{kind=link}

Is Higher Volatility Making a Comeback?

- Long dormant volatility begins to stir anew across several asset classes

- Copper still undecided even as gold, silver implied volatility heads higher

- Fed’s serial rate hikes could be the cause if volatility returns in a big way

Occasional brief spikes notwithstanding, volatility has been dormant across most asset classes (excluding energy) over the past eight years. Equities, fixed income products, currencies, metals and agricultural goods saw steep declines in implied volatility after 2010 and it that has generally remained at exceptionally low levels for the past several years. In the past few months, however, there have been signs that implied volatility might be in the early stages of a transition to much higher levels in the coming months or years across a wide range of assets.

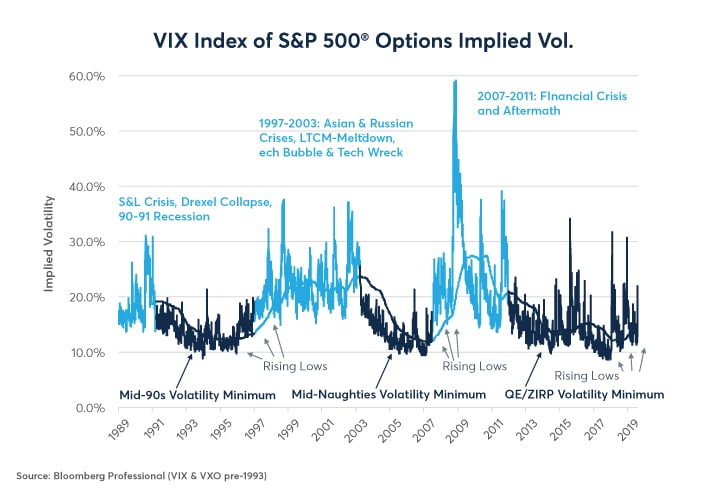

Options on US equity indices are in the vanguard of the nascent trend towards higher volatility. S&P 500® volatility hit bottom in early 2018 and has since seen a pattern of rising off lows, looking eerily like moves in 1996 and early 2007 as the market prepared to transition from a low-volatility state to a higher one. That said, implied volatility on S&P 500 options remains exceptionally low by historical standards. Even during the volatility spike early this August, the VIX peaked out at 23% – near the low end of its range during its previous high-volatility state such as the one from 1997 until 2003 or from mid-2007 until late 2011 (Figure 1).

Figure 1: Are Equity Options’ Implied Volatility on an Upward Trend?

{kind=link}

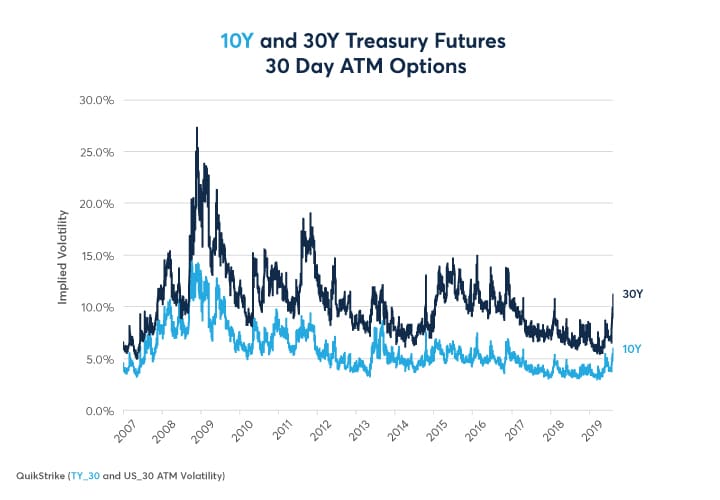

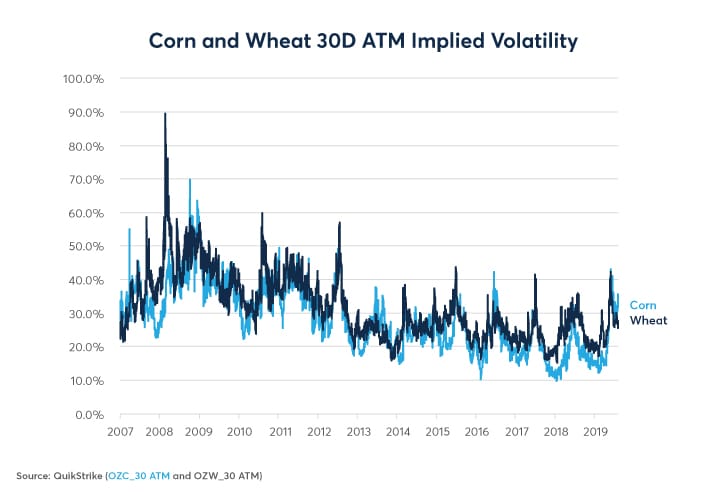

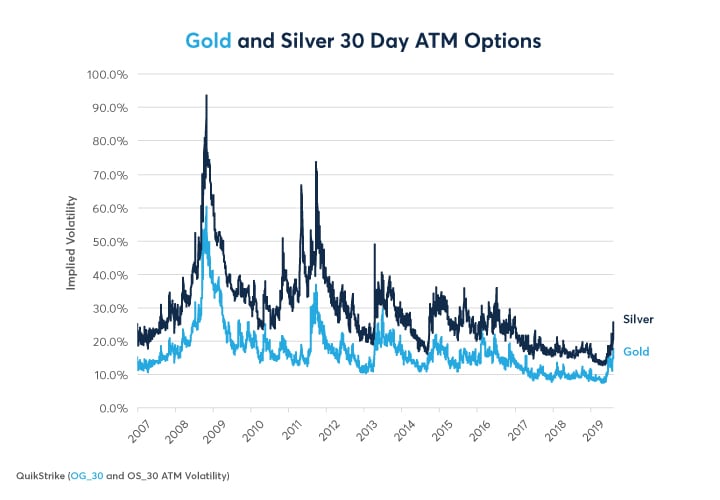

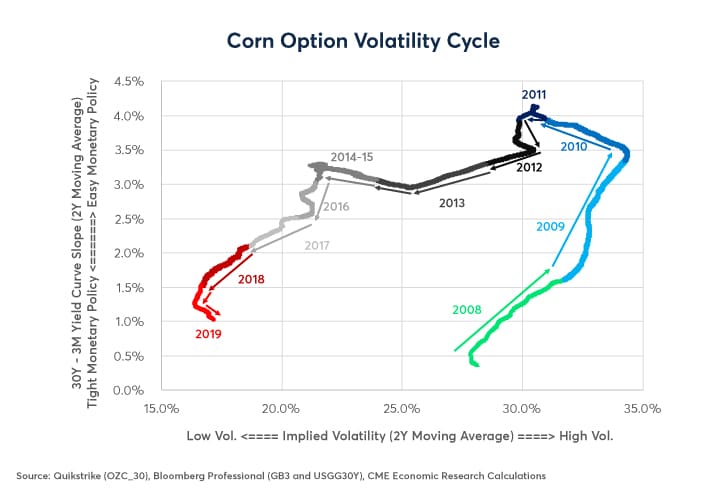

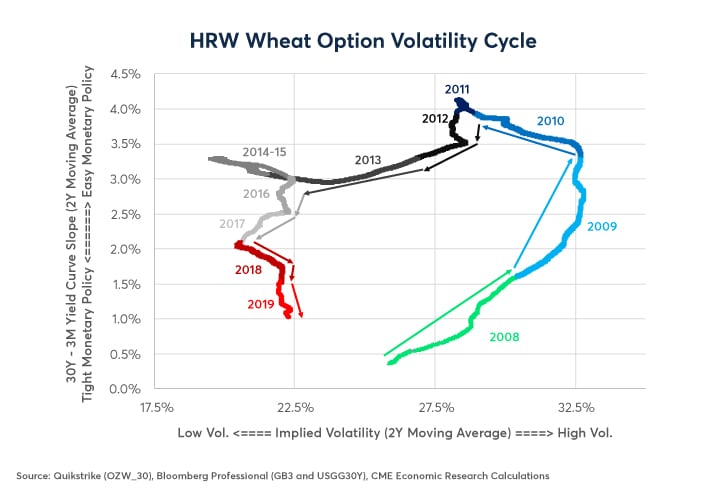

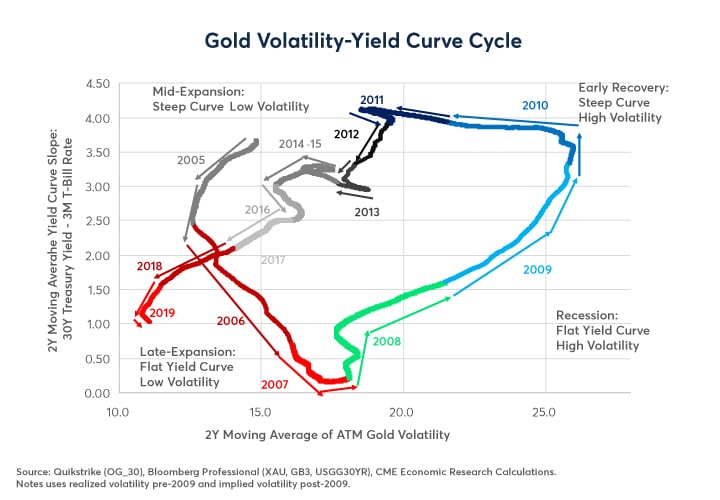

In most other markets, volatility hit bottom more recently and, in some markets like currencies it’s still skidding along the bottom near all time lows. That said, in fixed income (Figure 2), grain markets (Figure 3) and gold and silver (Figure 4), volatility appears to be one the rise. Although volatility has risen in the last few months, in each of these markets, the cost of options remains much closer to historic lows than historic highs and is way less than one-half of levels achieved between 2007 and 2011.

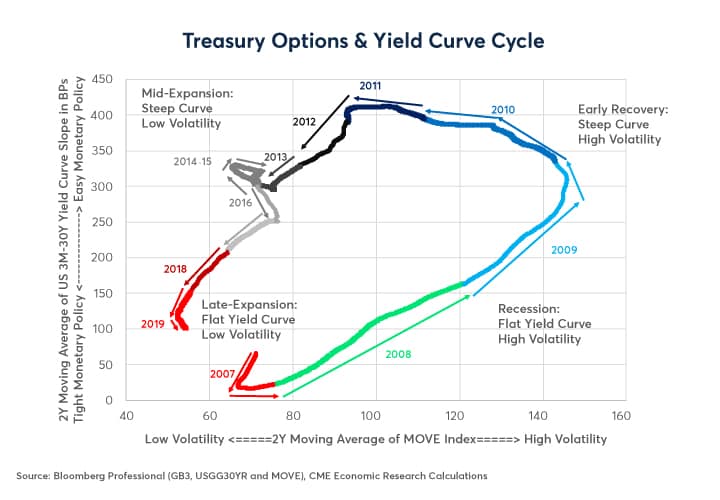

Figure 2: Treasury Options May Now Also be in a Pattern of Rising Off Lows.

{kind=link}

Figure 3: Corn and Wheat Options Implied Volatility has Risen.

{kind=link}

Figure 4: Implied Volatility on Gold and Silver Options has Risen From Historic Lows.

{kind=link}

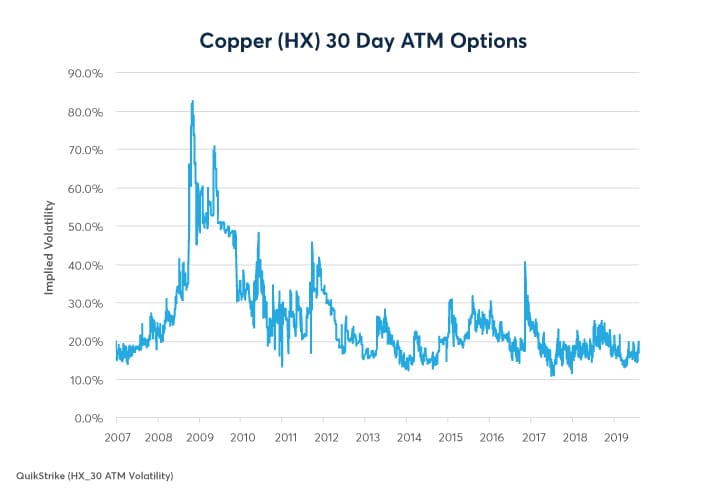

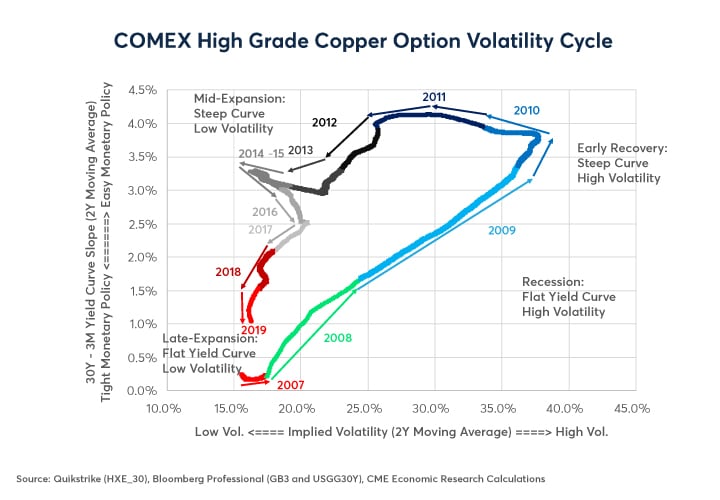

Copper options have not participated to any great extent in the move towards higher implied volatility seen in the gold and silver markets despite a 5% fall in the dollar-denominated price of copper following the intensification of the Sino-US trade war. That said, implied volatility on copper options hit bottom in mid-2017 at around 12% and has since moved closer to 20% (Figure 5).

Figure 5: Implied Volatility on Copper Options Hit Bottom in 2017 but Hasn’t Risen Dramatically, Yet.

{kind=link}

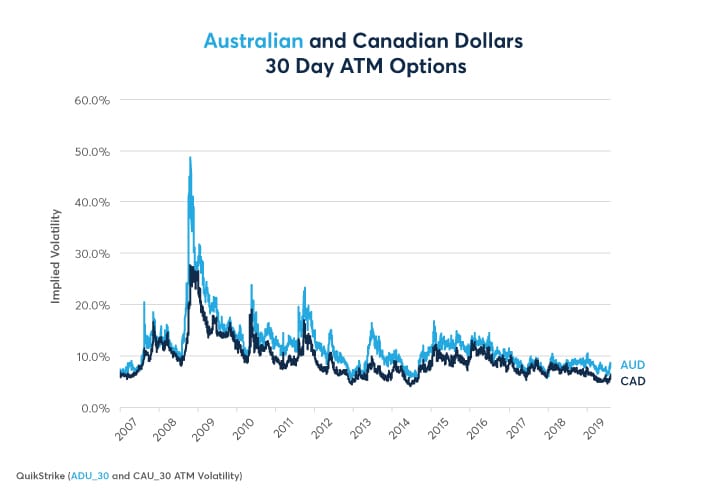

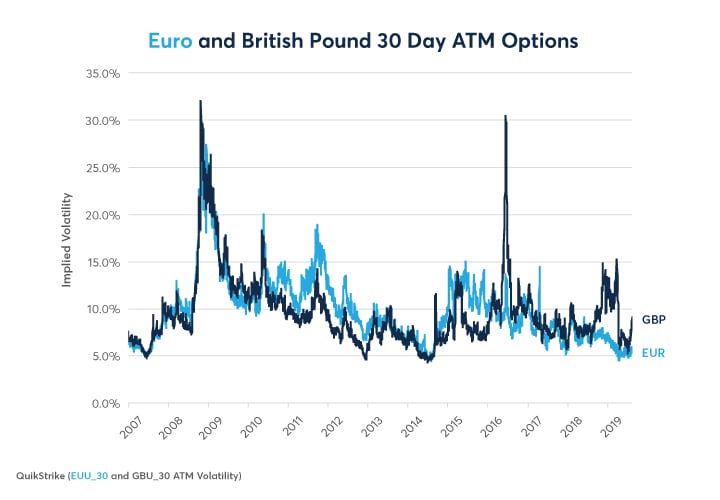

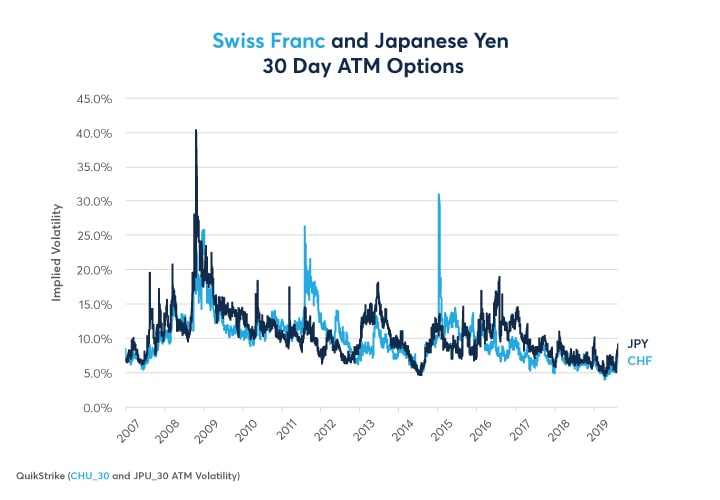

Currency options implied volatility has also risen slightly off its recent lows but any upward trend in implied volatility among the major currency pairs is not as noticeable as it is in the other asset classes (Figure 6-8). The exceptions are pound (driven by Brexit) and the yen, where volatility has risen a bit more.

Figure 6: AUD, CAD Options Barely Stifled a Yawn Over the Escalation in Sino-US Trade Dispute.

{kind=link}

Figure 7: Brexit is Driving Pound Options Implied Volatility Slightly Higher but EUR Options Apathetic.

{kind=link}

Figure 8: Trade War has Sent JPY Options Implied Volatility Slightly Higher but not CHF.

{kind=link}

Periods of high and rising volatility usually have two things in common:

- A proximate cause: An event or series of events get blamed for the rise in volatility.

- A deep underlying cause: The real reason why implied volatility shifts from low to high.

The proximate cause varies from period to period. In the late 1980s, rising volatility was blamed on program trading in equities, portfolio insurance, trade disputes and the S&L crisis/the collapse of Drexel Burnham Lambert. In the late 1990s, the structural rise in volatility was blamed on the Asian financial crisis, the Russian debt default and the meltdown of the Connecticut-based hedge fund Long Term Capital Management (LTCM). When that period of high volatility extended into the early 2000s, it was attributed to the popping of the tech bubble and the subsequent 85% decline in the NASDAQ, 9/11 and the run up to the Iraq War. The subprime crisis and subsequent banking failures were blamed for the explosion in volatility in 2008.

Fair enough. Without a doubt each of these diverse events contributed to rising volatility. What ties these various events together is a common underlying factor: US monetary policy. In the years prior to each of these events, the Federal Reserve (Fed) tightened policy, flattened the yield curve, dried up market liquidity, made the economy in both the US and emerging markets more susceptible to credit defaults and set the conditions for a spark to light the volatility fire. Each time the spark was different but each time a period of tight money eventually provided the tinder necessary to ignite a rise in volatility.

When the Fed maintains an easy monetary stance, a great deal of money finds its way into financial and commodity markets. Amid easy credit conditions, buyers and sellers can find one another easily. Even large orders can often be executed without moving prices dramatically. Moreover, when low volatility persists over long periods, short-volatility strategies prosper, and investors become complacent. Risk models, which are often myopic and backward looking, can be beguiled by years of modest-sized market moves into underestimating the actual amount of risk in the financial system. This creates problems when the Fed tightens monetary policy and markets begin the process of transitioning from low to high volatility.

As the central bank raises rates (and in the current cycle, reduces the size of its balance sheet), it drains money out of the financial system. Eventually, there comes a day when a piece of news causes a trader or group of traders to execute large orders in the market – ones that would not have ordinarily moved prices a great deal in an easy money environment. The problem is that after a period of tight money, there won’t necessarily be anyone to take the other side of these trades at anything close to the current market prices. As prices begin to move to fill the orders, volatility begins to rise. People get closed out of positions, especially short-volatility positions, and the cost of options begins to rise as the prices of “risk assets” cascades lower.

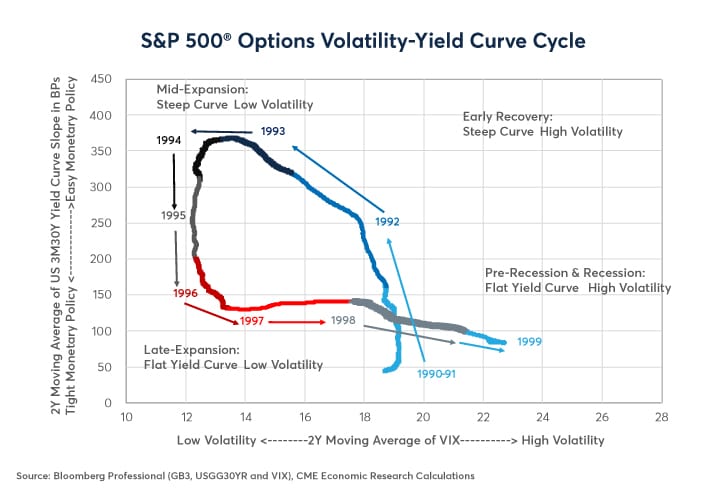

Figure 9: The 1990s Equity Index Option Volatility Cycle.

{kind=link}

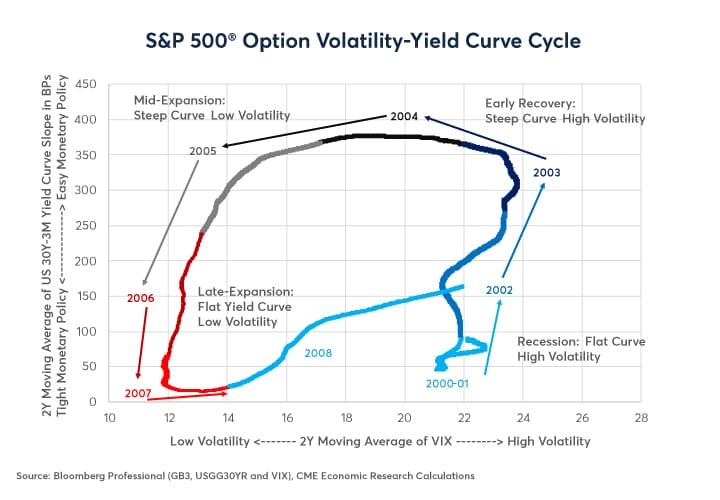

Figure 10: The Tech Wreck to Financial Crisis Equity Index Options Volatility Cycle.

{kind=link}

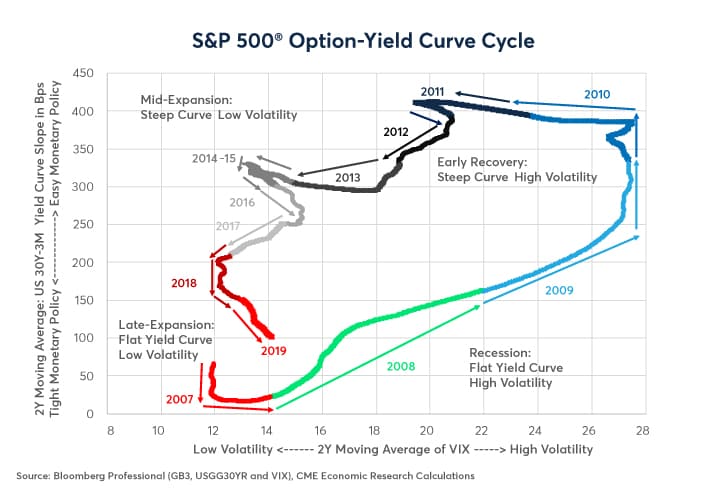

Figure 11: The Current Equity Index Options Volatility Cycle – Notice The Recent Rise in Volatility.

{kind=link}

The interplay between volatility and monetary policy gives rise to a four-part cycle that has been repeating in equity index options (Figures 9-11) for at least three decades and has been present in US Treasury options for at least two decades (Figures 12 and 13). The data history on the other asset classes is shorter but for those asset classes, it has been visible since at least 2007 (Figures 14-18). The cycle works as follows:

- Late Expansion/Pre-Recession: Tight monetary policy characterized by a flat yield curve, gives way to a significant and sustained rise in market volatility.

- Recession: Extremely high volatility and weak economic growth, oblige the central bank to ease policy, steepening the yield curve.

- Early Recovery: Easy monetary policy, characterized by a steep yield curve, generates an economic recovery. Volatility, which remains high in the early stages of a recovery, begins to subside.

- Mid-Expansion: Volatility falls to low levels and central bank begins to tighten monetary policy, flattening the yield curve.

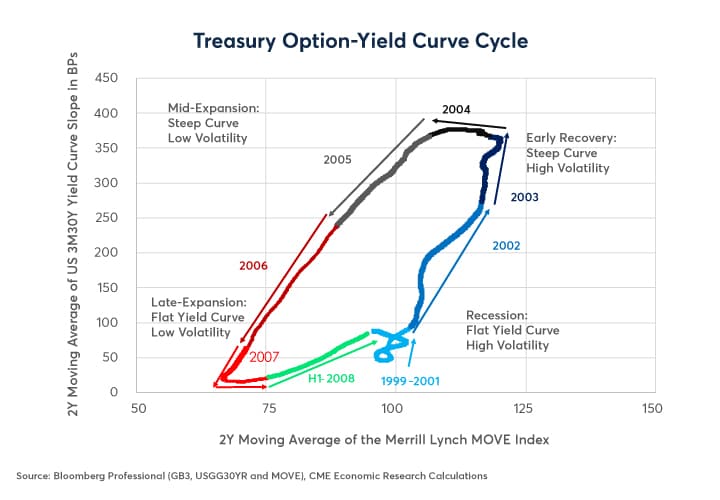

Figure 12: The 1999-2008 Treasury Option Volatility Cycle.

{kind=link}

Figure 13: After Years of Declines, Treasury Option Volatility May Have Turned the Corner.

{kind=link}

Thus far in the current cycle, equity index volatility has been on a decided upturn since early 2018. Bonds, gold, silver, copper and grains are now turning upward in terms of volatility as well. This begs the question, will the July 31 Fed rate cut do anything to stave off a shift to a structurally higher level of volatility? We doubt it. After raising rates by 300 basis points (bps) in 1994, the Fed cut rates by 75 bps in 1995. Volatility started to trend higher. After a major bout of volatility in 1998, the Fed cut rates by an additional 75 bps. Volatility remained high anyway until after the Fed slashed rates from 6.5% in 2000 to 1% by mid-2003 . As such, after raising rates from 0.125% in 2015 to 2.375% by the end of 2018, it will require probably more than three Fed cuts to quell a cross-asset surge in volatility.

Figure 14: Corn Options Volatility May be Turning Higher.

{kind=link}

Figure 15: Wheat Options Volatility May Soon be on the Rise.

{kind=link}

Figure 16 : Gold Option Volatility May have Hit Bottom and Could Begin Trending Upward.

{kind=link}

What’s more is that the yield curve was inverted more deeply after the Fed’s July 31 rate cut than it was before. The escalation of the trade war on August 1 pushed long-term yields lower. If volatility does rise substantially across asset classes later this year and in 2020, the trade war may be the proximate cause, but the Fed’s monetary tightening will be underlying cause. The combination of trade disputes plus tight money could send volatility soaring.

Figure 17: Will Tighter US Monetary Policy also Drive Copper Volatility Higher?

{kind=link}

Figure 18: Currency Options are the Only Ones that Have Resisted a Rise in Volatility.

{kind=link}

Finally, be wary of articles and analyses that blame hedge funds, risk parity, high-frequency traders, algorithms etc. These entities were present during the low volatility and they will also be present in the high volatility period. They shouldn’t be blamed for any coming rise in volatility any more than they should be given credit for the past eight years of exceptionally low volatility. The fault may lie with the Fed, whose easy monetary policy between 2009 and 2016 after the financial crisis muted volatility, and now risks elevating volatility after raising rates nine times between 2015 and the end of 2018.

Equity options

CME Group's suite of Equity Index options on futures offer around-the-clock liquidity, market depth, and extensive product choice on the world's benchmark indices to suit a variety of trading strategies. Capitalize on potential margin offsets on futures and options strategies, advanced on-screen spreading capabilities, and the certainty of central clearing.