{kind=link}

Industrial Metals: Can Demand Meet Supply Challenge?

Two decades ago, the main problem in base metals markets was insufficient supply to meet rising demand, particularly from China. As a result, prices soared. Copper prices rose 440% between 2000 and 2011. For aluminum, prices doubled between 2000 and 2008 despite a growth in supply.

These price increases incentivized massive increases in production that essentially inversed the metals markets main economic problem. During the 2010s, the primary issue has been too much supply chasing too little demand. Since the mid-1990s, global production of iron ore and aluminum has tripled, while copper and steel production has more than doubled (Figure 1). Given the large supplies available, and slowing growth in emerging markets, metals prices crashed after 2011 and have not fully recovered.

Figure 1: A world awash in metals

{kind=link}

In recent years, despite the mid-decade crash in prices, the production of aluminum, copper and steel has continued to rise. This suggests that even at post-crash prices, it is still profitable to invest in new production and to maintain existing production facilities. The only exception to this appears to be iron ore, whose mining production dipped in 2015 and 2016 before recovering in 2017 and 2018.

The primary challenge of the metals markets in the 2020s will be to absorb the outsized increases in mining supply and that depends on continued demand growth in China, which consumes 40-50% of the aluminum, copper and steel supply and up to two-thirds of the world’s iron ore. Meanwhile, China’s GDP, measured at 2019 exchange rates, will be about 16.2% of global GDP, according to the International Monetary Fund (IMF). On a purchasing power parity basis, which account for the cost of living in each country, China’s GDP accounts for 19.2% of global total.

There are two reasons why China’s consumption of industrial metals appears to be so high relative to the size of its GDP. The first is that China buys raw materials from all over the world, inflating its metals import figures, but then re-exports globally the metals as finished products. In other words, Chinese metals consumption statistics overstate its domestic consumption of these metals. Chinese exports and manufacturing account for 17.5% and 38% of GDP, respectively. If one assumes that nearly all of China’s exports are manufactured goods, this implies that nearly half (about 45%) of metals that enter China eventually leave as parts of finished goods.

Even under this assumption, China’s purely domestic consumption of metals is still about 20-30% higher than the world average, given the size of its GDP. Part of the reason for China’s elevated level of metals consumption is that China does relatively less metals recycling than other nations. In the US, Europe and Japan, when new metal is needed, a great deal of it can be obtained from scrapped cars, building materials and appliances. By contrast, as China grew rapidly during the past few decades, recycling opportunities were scarce relative to the size of its demand for industrial metals.

That will begin to change during the 2020s. The average car lasts for about a dozen years before being scrapped. China became the world’s largest car market by annual sales in 2009. Currently, China has over 250 million motor vehicles, just behind the EU and US in terms of aggregate numbers. Growth in China’s automotive purchases will probably slow during the 2020s while vehicle retirements will increase. This will likely translate into less demand for newly produced metals.

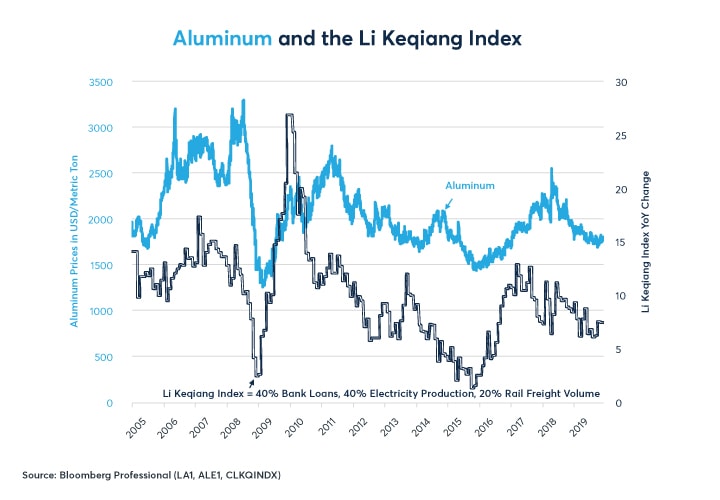

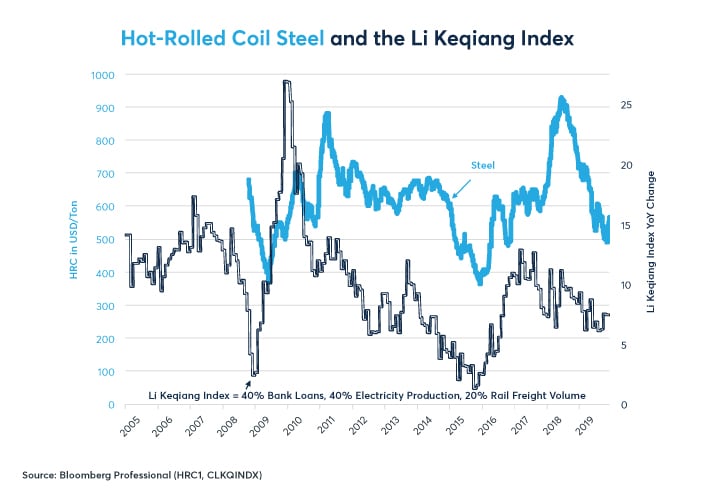

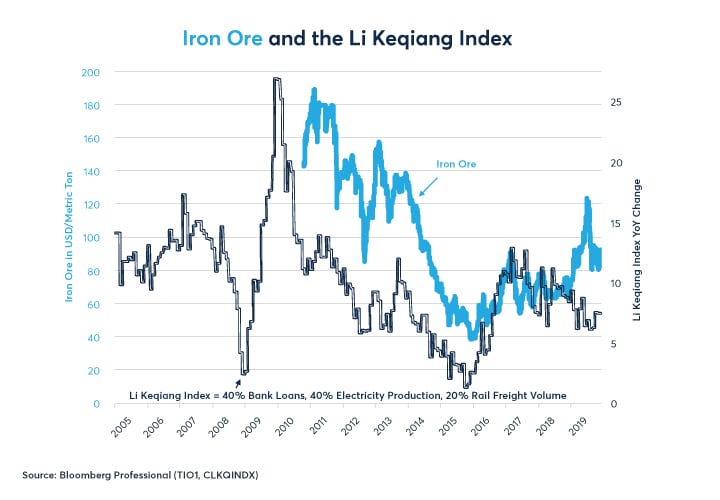

The good news for producers of industrial metals is that heading into 2020, China looks like it’s in pretty good shape. While export growth has stalled in large part because of the trade war (Figure 2) and official GDP growth has slowed slightly, alternative, narrower measures of China’s industrial economy show strong growth. The so-called Li Keqiang measure of electrical consumption, bank loans and rail freight has been showing growth rates of around 7.5% year on year (Figure 3). This measure shows an especially high correlation to future movements in metals prices (Figure 4).

Figure 2: China’s exports have stagnated but not fallen like in 2008 or 2014-16

{kind=link}

Figure 3: Narrow measures of GDP show faster growth than the official (broader) GDP

{kind=link}

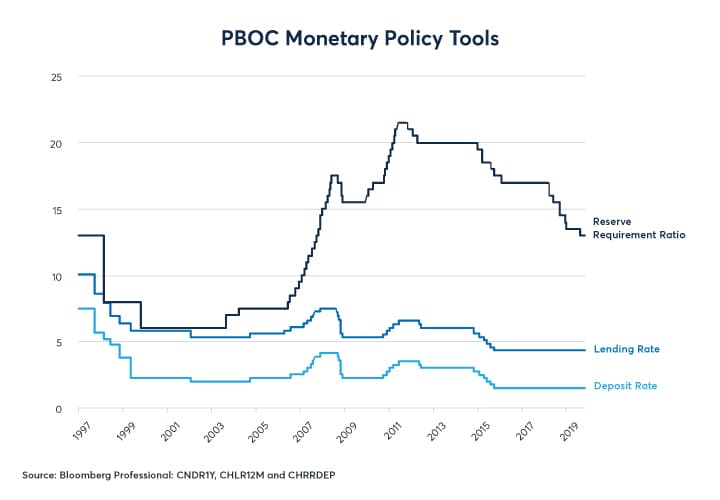

These sorts of numbers suggest that, so far, China’s efforts to stimulate growth have overwhelmed the negative impacts of the trade war. Indeed, the People’s Bank of China has been slashing its banks’ reserve requirement ratios (Figure 5). Easier monetary policy in conjunction with a weakening of the currency that has largely offset the impact of the higher tariffs appears to have stabilized China’s growth rate, at least for now. If China’s yield curve is any indication, the Middle Kingdom’s growth may continue robustly into early 2020 – welcome news for producers of industrial metals.

Figure 4: All industrial metals show a strong response to changes in the Li Keqiang index

{kind=link}

Figure 5: PBOC has been easing monetary policy

{kind=link}

The risk is that the very things that China has been doing to stabilize its growth rate in the short term will create long-term problems. If lowering the reserve requirement ratio was meant to stimulate credit growth, by all appearances, it worked. In the first half of 2019, China’s total credit to the non-financial sector rose from 254.6% to 261.5% of GDP. Every category increased: government debt rose from 49.8% to 52.4% of GDP; household debt increased from 52.6% to 54.6% and non-financial corporate debt, which had been falling the previous three years, inched up from 152.2% to 154.5% (Figure 6). This now puts China’s debt levels higher than those in the EU, UK or US relative to the size of its GDP (Figure 7).

Figure 6: Chinese debt levels resumed their rise in H1 2019

{kind=link}

Figure 7: Chinese debt/GDP ratios now exceed those in the West

{kind=link}

High debts levels combined with unfavourable demographic developments could slow China’s growth in the 2020s. During the coming decade China’s working age population will decline by 5%, after having grown by 30% since 1990. Debt, demographics and a move towards recycling could make it difficult for China to absorb the massive increase in industrial metals supply that has come on line during the past few decades.

Finally, no other economy can compensate for any lost demand growth in China. According to the IMF’s 2019 estimates, China’s economy still dwarfs its next largest emerging market peers: 4.8x India, 7.7x Brazil and 8.6x Russia. For their part, Brazil and Russia are highly dependent on China as source of demand for their natural resources. So, if China slows and natural resources prices sink, their currencies, along with many other emerging market currencies, will likely fall, further dampening demand for industrial metals.

Appendix: Measures of Chinese Industrial Growth and Aluminum Prices

Figure 8: Aluminum

{kind=link}

Figure 9: Copper

{kind=link}

Figure 10: Steel

{kind=link}

Figure 11: Iron Ore

{kind=link}

Base Metals

Our comprehensive suite of Base Metals products provide opportunities to mitigate the risk involved in the metals markets. Our contracts offer extensive trading opportunities, global price discovery, and price transparency with our sustainable and cost-competitive vehicles to manage price exposure.