https://www.cmegroup.com/content/dam/cmegroup/images/common/default/article-940x600.jpg

{kind=link}

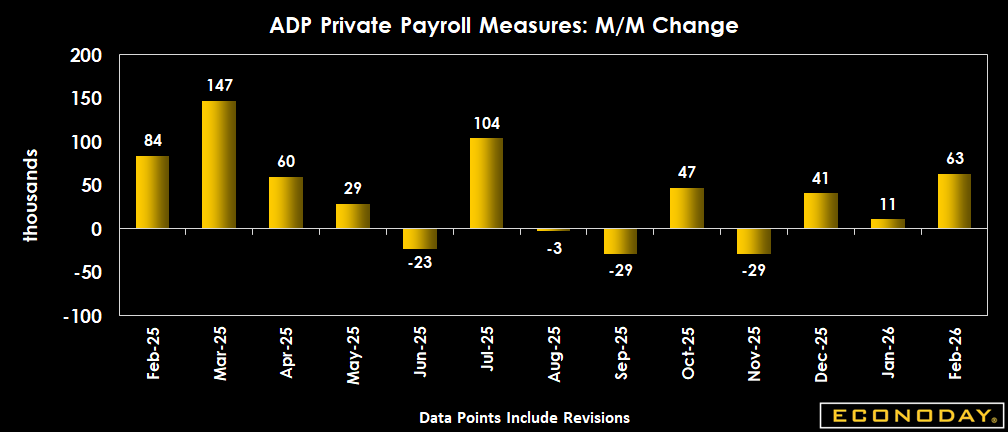

US: ADP Employment Report

| Consensus | Consensus Range | Actual | Previous | Revised | |

| Private Payrolls - M/M | 43,000 | 19,000 to 55,000 | 63,000 | 22,000 | 11,000 |

Highlights

Private-sector hiring was stronger than expected in February, as payrolls increased 63,000, above even the highest forecast of 55,000 in an Econoday survey.

Still, details show that the labor market isn't that easy to navigate, with gains highly concentrated in just a few sectors and"no widespread pay benefit from changing job". In addition, January's growth estimate was revised down to 11,000, half the initial 22,000 initially reported in the ADP national employment report.

Employment increased 47,000 in services and 16,000 in goods-producing industries.

For job stayers, the median pay increase was unchanged from January at 4.5 percent year-over-year, while pay growth slowed to 6.3 percent in February from 6.4 percent in January for job-changers. The pay premium for switching employers hit a record low, the report said.

Looking at February's breakdown by sector, the increase in service was concentrated in education and health services, up 58,000, followed by information, up 11,000. By contrast, professional and business services dropped 30,000. In gods-producing industries, gains were concentrated in construction, up 19,000, while manufacturing shed 5,000 jobs. Employment was up just 2,000 in natural resources and mining.

Payrolls increased the most in small businesses with less than 20 employees, which recorded a 58,000 gain, followed by large establishments of more than 500 employees, where hiring was up 10,000. Medium sized establishments (50-499 workers), by contrast, recorded a decline of 7,000.

Regionally, hiring only declined in the Midwest, by 4,000. The largest payroll increase was in the South, with 37,000, followed by the West (19,000) and the Northeast (11,000).

Market Consensus Before Announcement

Private payrolls expected up a meager 43K in February after 22K in January.

Definition

The national employment report from Automated Data Processing Inc. is computed from ADP payroll data and offers advance indications on the U.S. workforce. ADP's data cover more than 500,000 companies totaling more than 25 million employees. The report is produced by ADP Research Institute in collaboration with Stanford Digital Economy Lab.

Description

Market players have become accustomed to the excitement on employment Friday and realize the rich detail of the monthly employment situation can help set the tone for the entire month. While economists have improved their nonfarm payroll forecasts over the years, it is not unusual to see surprises on employment Friday. To that end, the ADP's national employment report can help improve the payroll forecast by providing information in advance of the employment report.

The employment statistics also provide insight on wage trends, and wage inflation is high on the list of enemies for the Federal Reserve. Fed officials constantly monitor this data watching for even the smallest signs of potential inflationary pressures, even when economic conditions are soggy. If inflation is under control, it is easier for the Fed to maintain a more accommodative monetary policy. If inflation is a problem, the Fed is limited in providing economic stimulus.

By tracking jobs, investors can sense the degree of tightness in the job market. If wage inflation threatens, it's a good bet that interest rates will rise; bond and stock prices will fall. No doubt that the only investors in a good mood will be the ones who watched the employment report and adjusted their portfolios to anticipate these events. In contrast, when job growth is slow or negative, then interest rates are likely to decline - boosting up bond and stock prices in the process.

{kind=link}