{kind=link}

| Consensus | Consensus Range | Actual | Previous | Revised | |

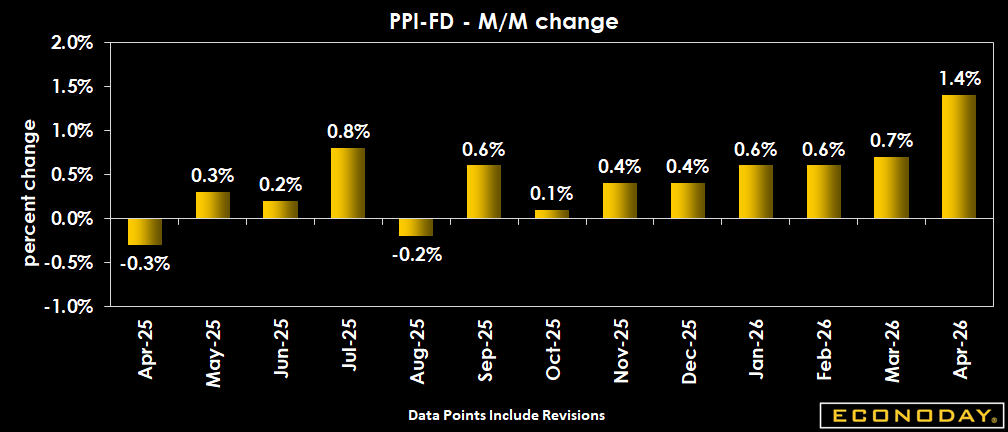

| PPI-FD - M/M | 0.5% | 0.4% to 0.7% | 1.4% | 0.5% | 0.7% |

| PPI-FD - Y/Y | 4.8% | 4.2% to 5.0% | 6.0% | 4.0% | 4.3% |

| Ex-Food & Energy - M/M | 0.3% | 0.2% to 0.3% | 1.0% | 0.1% | 0.2% |

| Ex-Food & Energy - Y/Y | 4.3% | 3.9% to 4.3% | 5.2% | 3.8% | |

| Ex-Food, Energy & Trade Services - M/M | 0.3% | 0.2% to 0.3% | 0.6% | 0.2% | |

| Ex-Food, Energy & Trade Services - Y/Y | 4.4% | 3.6% | 3.7% | ||

| PPI-FD Goods - M/M change | 2.0% | 1.6% | 1.9% | ||

| PPI-FD Goods - Y/Y change | 7.4% | 4.9% | 5.2% | ||

| PPI-FD Services - M/M change | 1.2% | 0.0% | 0.2% | ||

| PPI-FD Services - Y/Y change | 5.5% | 3.7% | 3.9% |

Highlights

Wholesale prices rose 1.4 percent in April, twice as much as March, and the fastest pace since March 2022. April's reading was also twice as much as the highest expectation in an Econoday survey of forecasters. The Producer Price Index was up 6.0 percent year-over-year, up from 4.3 percent the previous month, the highest rate since December 2022, also topping expectations. Even more concerning was the acceleration in price growth excluding food and energy, to 1.0 percent in April from 0.2 percent in March, also above expectations that had centered on 0.3 percent, for a 12-month gain of 5.2 percent.

Energy price increases actually slowed to 7.8 percent in April from 10.1 percent, although this marked the third consecutive monthly advance, for a year-over-year growth of 22.3 percent. Excluding energy alone, prices were up 1.0 percent on the month after 0.2 percent in March. Food, by contrast, rebounded 0.2 percent after contracting 0.6 percent. The index excluding food increased 1.4 percent after 0.8 percent, and 6.2 percent from a year earlier.

Prices excluding food, energy and trade services were up 0.6 percent in April after 0.2 percent, for a 12-month increase of 4.4 percent, the largest since February 2023.

As central banks, including the Federal Reserve, are assessing the extent to which energy price gains carry over to prices in the rest of the economy, today's report brings reasons to worry.

Services prices were up 1.2 percent on the month after 0.2 percent in March, accounting for nearly 60 percent of the overall price increase. Services increased 5.5 percent year-over-year.

Goods prices did not accelerate as much, rising 2.0 percent after 1.9 percent, for a 12-month gain of 7.4 percent.

At the retail level, April CPI report showed the inflationary impact of the Iran conflict, with another jump in energy prices, as well as a knock-on effect on other important commodities and categories like airfare (up 2.8 percent on a monthly basis). Core consumer prices (excluding food and energy) also rose noticeably in April, as the ongoing tariffs impact on apparel prices (up 0.6 percent month-over-month and +4.2 percent vs. last year), for example continues.

Market Consensus Before Announcement

PPI-FD seeing energy price effects with a big 0.5 percent rise expected on month and a whopping 4.8 percent on year.

Definition

The Producer Price Index (PPI) of the Bureau of Labor Statistics (BLS) is a family of indexes that measures the average change over time in the prices received by domestic producers of goods and services. PPIs measure price change from the perspective of the seller. Effective with the January 2014 PPI data release in February 2014, BLS transitioned from the Stage of Processing (SOP) to the Final Demand-Intermediate Demand (FD-ID) aggregation system. The headline PPI (for Final Demand) measures price changes for goods, services, and construction sold to final demand: personal consumption, capital investment, government purchases, and exports.

Description

The PPI measures prices at the producer level before they are passed along to final consumers. A portion of the inflation at the producer level gets passed through to the consumer price index (CPI). By tracking price pressures in the pipeline, investors can anticipate inflationary consequences in coming months.

While the CPI is the price index with the most impact in setting interest rates, the PPI provides significant information earlier in the production process. As a starting point, interest rates have an"inflation premium" and components for risk factors. A lender will want the money paid back from a loan to at least have the same purchasing power as when loaned. The interest rate at a minimum equals the inflation rate to maintain purchasing power and this generally is based on the CPI. Changes in inflation lead to changes in interest rates and, in turn, in equity prices.

The PPI comes in two key main versions: final demand (FD) and intermediate demand (ID). The final demand portion is composed of six main price indexes: final demand goods; final demand trade services; final demand transportation and warehousing services; final demand services less trade, transportation, and warehousing; final demand construction; and overall final demand.

The intermediate demand portion of the FD-ID system tracks price changes for goods, services, and construction products sold to businesses as inputs to production, excluding capital investment. There are two parallel treatments of intermediate demand, each constructed from the identical set of commodity price indexes. The first treatment organizes commodities according to commodity type, and the second organizes commodities using a stage-based, production flow model.

The PPI is considered a precursor of both consumer price inflation and profits. If the prices paid to producers increase, businesses are faced with either charging higher prices or taking a cut in profits. The ability to pass along price increases depends on the strength and competitiveness of the marketplace.

Under the prior PPI system, the producer price index was substantially more volatile than the consumer price index because the CPI included services while the PPI did not. Volatility has been reduced substantially in the PPI-FD due to the inclusion of services but the PPI still is more volatile than the CPI. Wages are a bigger share of the costs at the retail level than at the producer level and this plays a role in the CPI’s lower volatility. Also, the PPI does not include owners’ equivalent rent—a large and slow moving component in the CPI. Food and energy prices are major sources of volatility in the PPI, hence, the greater focus on the"core PPI" which excludes these two components.

The bond market rallies when the PPI decreases or posts only small increases, but bond prices fall when the PPI posts larger-than-expected gains. The equity market rallies with the bond market because low inflation promises low interest rates and is good for profits.

{kind=link}