https://www.cmegroup.com/content/dam/cmegroup/images/common/default/article-940x600.jpg

{kind=link}

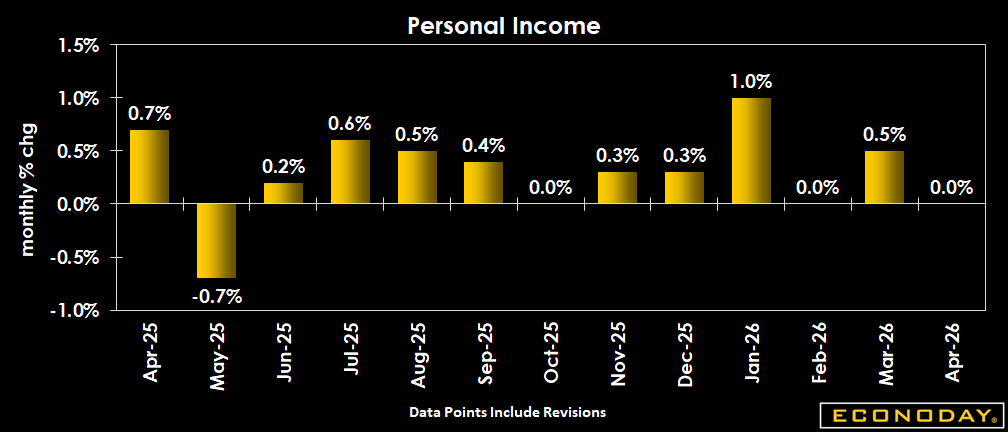

US: Personal Income and Outlays

| Consensus | Consensus Range | Actual | Previous | Revised | |

| Personal Income - M/M | 0.4% | 0.2% to 0.6% | 0.0% | 0.6% | 0.5% |

| Personal Consumption Expenditures - M/M | 0.5% | 0.3% to 0.9% | 0.5% | 0.9% | 1.0% |

| PCE Price Index - M/M | 0.5% | 0.4% to 0.6% | 0.4% | 0.7% | |

| PCE Price Index - Y/Y | 3.8% | 3.6% to 4.0% | 3.8% | 3.5% | |

| Core PCE Price Index - M/M | 0.3% | 0.2% to 0.3% | 0.2% | 0.3% | |

| Core PCE Price Index - Y/Y | 3.3% | 3.3% to 3.3% | 3.3% | 3.2% |

Highlights

Personal income was virtually flat in April after rising 0.5 percent in March, revised down from 0.6 percent, a weaker reading than expectations that had ranged between 0.2 percent and 0.6 percent in an Econoday survey.

In April, a decrease in farm proprietors' income was partly offset by an increase in compensation led by the increase was led by private wages. The USDA's Farmer Bridge Assistance Program closed application submissions in mid-April, leading to a decrease in payments to farmers.

Personal consumption expenditures increased 0.5 percent on the month, half the pace of the previous month.

The PCE deflator rose 0.4 percent month-over-month, a slowdown from 0.7 percent in March, although the growth pace picked up on a 12-month basis to 3.8 percent from 3.5 percent two months into the Middle East conflict. This was the largest 12-month gains since 4.0 percent in May 2023. Today's inflation report combined with the latest developments around the negotiations with Iran provide support to concerns reported in the FOMC Minutes among almost all participants that the Middle East conflict could persist for an extended period and that oil and other commodity prices could remain elevated for longer than expected.

The PCE price index excluding food and energy was up 0.2 percent on the month. On a 12-month basis, the index was up 3.3 percent, roughly as expected, reflecting yet another acceleration from 3.2 percent in March and 3.0 percent in February. This trend indicates that higher oil prices are feeding through other areas of the economy.

Against the backdrop of higher prices, higher spending and flat income, the saving rate came down from 3.2 percent in March to 2.6 percent in April, the lowest rate since 2.2 percent in June 2022.

Market Consensus Before Announcement

Moderate ongoing increases in spending and income expected. The focus will be PCE prices which are expected to be lifted by fuel costs to show a big 0.5 percent rise on the month and a 0.3 percent increase ex-food & energy.

Definition

Personal income represents the income that households receive from all sources including wages and salaries, fringe benefits such as employer contributions to private pension plans, proprietors' income, income from rent, dividends and interest and transfer payments such as Social Security and unemployment compensation. Personal contributions for social insurance are subtracted from personal income.

Personal consumption expenditures are the major portion of personal outlays, which also include personal interest payments and transfer payments. Personal consumption expenditures are divided into durable goods, nondurable goods and services. These figures are the monthly analogues to the quarterly consumption expenditures in the GDP report, available in nominal and real (inflation-adjusted) dollars. Economic performance is more appropriately measured after the effects of inflation are removed.

Each month, the Bureau of Economic Analysis also compiles the personal consumption expenditure price index, also known as the PCE price index. This inflation index measures a basket of goods and services that is updated annually in contrast to the CPI, which measures a fixed basket.

Description

The income and outlays data are another handy way to gauge the strength of the consumer sector in this economy and where it is headed. Income gives households the power to spend and/or save. Spending greases the wheels of the economy and keeps it growing. Savings are often invested in the financial markets and can drive up the prices of stocks and bonds. Even if savings simply go into a bank account, part of those funds typically is used by the bank for lending and therefore contributes to economic activity. In the past twenty years, the personal saving rate has diminished rapidly as consumers have spent a greater and greater share of their income. But that has reversed in part during the recession that began in 2008 as consumers have cut back on credit card use and have been rebuilding retirement accounts.

The consumption (outlays) part of this report is even more directly tied to the economy, which we know usually dictates how the markets perform. Consumer spending accounts for more than two-thirds of the economy, so if you know what consumers are up to, you'll have a pretty good handle on where the economy is headed. Investors can see how consumers are directing their spending, whether they are buying durable goods, nondurable goods or services. Needless to say, that's a big advantage for investors who determine which companies' shares they will buy.

The PCE price indexes have gained importance since the Fed announced a medium-term inflation goal of 2 percent based on the headline number on a year-on-year basis. The Fed forecasts inflation for both the headline PCE price index and the core rate (excluding food and energy).

Importance

Income is the major determinant of spending -- U.S. consumers spend roughly 95 cents of each new dollar. Consumer spending accounts directly for more than two-thirds of overall economic activity and indirectly influences capital spending, inventory investment and imports.

Interpretation

Increases (decreases) in income and consumption cause bond prices to fall (rally). As long as spending isn't inflationary, the stock market benefits because greater spending spurs corporate profits. Financial market participants pay somewhat less attention to personal consumption expenditures than to retail sales, which are released earlier in the month. However, they do closely monitor personal income and the PCE deflator.

Changes in personal income signal changes in consumer spending. For instance, a period of rapid income growth may signal future gains in personal consumption expenditures as well. Conversely, a period of declining income growth could signal an impending recession. While consumers often still must purchase necessities, discretionary purchases may decline, or moderate.

Consumers are more likely to increase spending when they see their stock portfolios increase in tandem with the stock market. When the stock market falls, spending is likely to decline because consumers feel less wealthy. Home prices and home equity have similar effects. Rising home prices boost the amount of equity consumers have in their homes. This allows access to Home Equity Line of Credit (HELOC) accounts. Plus consumers feel wealthier whether they have a HELOC account or not. When home prices decline, home equity falls and cuts into consumer spending.

Personal income is a comprehensive figure, but also incorporates taxes consumers must pay. By removing personal tax payments from personal income, we are left with disposable income. This is what consumers have left to spend on goods and services. Adjusting for inflation reveals growth in real disposable income.

On the inflation front, if PCE inflation is running below the Fed's goal of 2 percent inflation, that is seen as favorable toward Fed ease or neutral monetary policy. PCE inflation above 2 percent suggests that the Fed might be more inclined to raise policy rates.

{kind=link}