https://www.cmegroup.com/content/dam/cmegroup/images/common/default/article-940x600.jpg

{kind=link}

US: Employment Situation

| Consensus | Consensus Range | Actual | Previous | Revised | |

| Nonfarm Payrolls - M/M | 55,000 | 40,000 to 100,000 | 50,000 | 64,000 | 56,000 |

| Unemployment Rate | 4.6% | 4.5% to 4.6% | 4.4% | 4.6% | 4.5% |

| Private Payrolls - M/M | 55,000 | 40,000 to 85,000 | 37,000 | 69,000 | 50,000 |

| Manufacturing Payrolls - M/M | -10,000 | -15,000 to -3,000 | -8,000 | -5,000 | -2,000 |

| Participation Rate | 62.4% | 62.5% | 62.5% | ||

| Average Hourly Earnings - Y/Y | 3.6% | 3.6% to 3.6% | 3.8% | 3.5% | 3.6% |

| Average Workweek | 34.3hrs | 34.2hrs to 34.3hrs | 34.2hrs | 34.3hrs |

Highlights

The monthly data on employment point to a labor market with ongoing modest hiring albeit in a few narrow sectors with relatively little layoff activity to increase unemployment. Taken together, the picture is one where businesses are holding on to their current staffing levels but only bringing on new employees where they can find someone with the right skills and/or experience. The supply of those potential hires is limited, and the competitive environment is favorable to those workers.

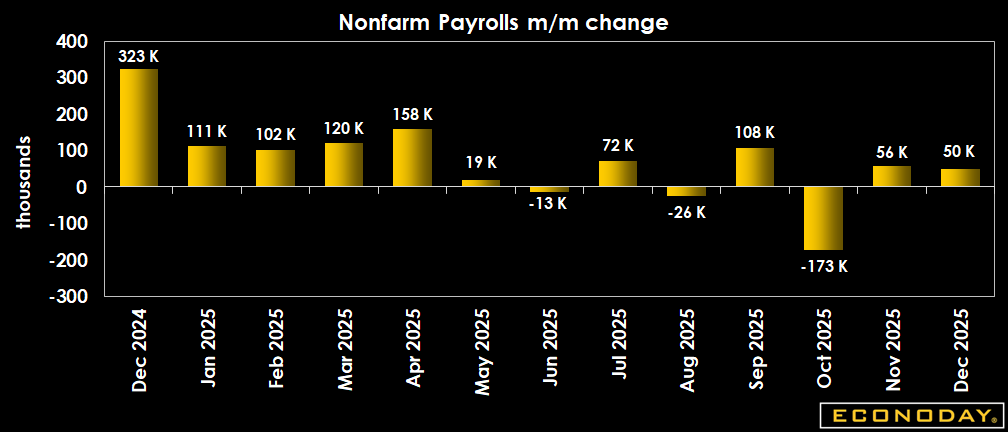

Nonfarm payrolls are up 50,000 in December, an increase not materially different from the consensus of up 55,000 in the Econoday survey of forecasters. However, the is a net downward revision to the prior two months of 76,000. This brings the monthly average change in nonfarm payrolls to a decrease of 22,000 compared to increases of 111,000 in the first quarter, 55, 000 in the second quarter, and 51,000 in the third quarter. Some of the weakness in the fourth quarter can be attributed to the government shutdown which encompassed October and the first days of November. However, even allowing for that, hiring continues its downward trend.

Private payrolls are up 37,000 in December. Goods-producers' payrolls are down 21,000 in December with declines in the three major categories. Mining and loggings is off 2,000, construction down 11,000, and manufacturing down 8,000. Service-providers' payrolls are up 58,000 with widespread small declines more than offset by increases of 41,000 in private education and health services and 47,000 in leisure and hospitality. These two sectors are the only ones consistently hiring in any number in recent months.

Government payrolls are up 13,000 in December mainly due to a rise of 18,000 in state and local government.

Average hourly earnings are up 0.3 percent in December from November and up 3.8 percent year-over-year. Earnings continue to rise steadily but the heated pace seen in the prior two years has cooled significantly.

The December report includes annual revisions to the household survey. Revisions are minor and run back five years.

The December unemployment rate is down a tenth to 4.4 percent and below the consensus of 4.6 percent in the Econoday survey. The December reading suggests that the rate has reached a plateau in the middle-4 percent range. The U-6 unemployment rate falls three-tenths to 8.4 percent in December. While it remains higher than readings in the first half of 2025, it points to less unemployment at the margins of the labor force.

The labor force is down 46,000 to 171.495 in December with the number of employed up 232,000 and unemployed down 278,000. The labor force participation rate is little changed at 62.4 percent in December from 62.5 percent in November.

Market Consensus Before Announcement

Payrolls seen up a moderate 55K with the jobless rate flat at 4.6 percent.

Definition

The most closely watched of all economic indicators, the employment situation is a set of monthly labor market indicators based on two separate reports: the establishment survey which tracks 650,000 worksites and offers the nonfarm payroll and average hourly earnings headlines and the household survey which interviews 60,000 households and generates the unemployment rate.

Nonfarm payrolls track the number of part-time and full-time employees in both business and government. Average hourly earnings track employee pay while the average workweek, also part of the establishment survey, tracks the number of hours worked. The report's private payroll measure excludes government workers.

The unemployment rate measures the number of unemployed as a percentage of the labor force. In order to be counted as unemployed, one must be actively looking for work. Other commonly known data from the household survey include the labor supply and discouraged workers.

Description

If ever there was an economic report that can move the markets, this is it! The anticipation on Wall Street each month is palpable, the reactions can be dramatic, and the information for investors is invaluable. By digging just a little deeper than the headline unemployment rate, investors can take more strategic control of their portfolio and even take advantage of unique investment opportunities that often arise in the days surrounding this report.

The employment data give the most comprehensive report on how many people are looking for jobs, how many have them, what they're getting paid and how many hours they are working. These numbers are the best way to gauge the current state as well as the future direction of the economy. Nonfarm payrolls are categorized by sectors. This sector data can go a long way in helping investors determine in which economic sectors they intend to invest.

The employment statistics also provide insight on wage trends, and wage inflation is high on the list of opponents of easy monetary policy. Fed officials constantly monitor this data watching for even the smallest signs of potential inflationary pressures, even when economic conditions are soggy. If inflation is under control, it is easier for the Fed to maintain a more accommodative monetary policy. If inflation is a problem, the Fed is limited in providing economic stimulus.

By tracking the jobs data, investors can sense the degree of tightness in the job market. If wage inflation threatens, it's a good bet that interest rates will rise; bond and stock prices will fall. No doubt that the only investors in a good mood will be the ones who watched the employment report and adjusted their portfolios to anticipate these events. In contrast, when job growth is slow or negative, then interest rates are likely to decline - boosting up bond and stock prices in the process.

Importance

The employment situation is the primary monthly indicator of aggregate economic activity because it encompasses all major sectors of the economy. It is comprehensive and available early in the month. Many other economic indicators are dependent upon its information. It not only reveals information about the labor market, but about income and production as well. In short, it provides clues about other economic indicators reported for the month and plays a big role in influencing financial market psychology during the month. Additionally, the Fed has made 6.5 percent unemployment a threshold for considering changes in policy - both for quantitative easing and the fed funds rate. And the Fed has emphasized that it is overall labor market conditions that matter - not just a specific number.

Interpretation

The bond market will rally (fall) when the employment situation shows weakness (strength). The equity market often rallies with the bond market on weak data because low interest rates are good for stocks. But sometimes the two markets move in opposite directions. After all, a healthy labor market should be favorable for the stock market because it supports economic growth and corporate profits. At the same time, bond traders are more concerned about the potential for inflationary pressures.

The unemployment rate rises during cyclical downturns and falls during periods of rapid economic growth. A rising unemployment rate is associated with a weak or contracting economy and declining interest rates. Conversely, a decreasing unemployment rate is associated with an expanding economy and potentially rising interest rates. The fear is that wages will accelerate if the unemployment rate becomes too low and workers are hard to find.

Nonfarm payroll employment indicates the current level of economic activity. Increases in nonfarm payrolls translate into earnings that workers will spend on goods and services in the economy. The greater the increase in employment, the faster is the total economic growth. When the economy is in the mature phase of an expansion, rapid increases in employment cause fears of inflationary pressures if rapid demand for goods and services cannot be met by current production.

When the average workweek trends up, it supports production gains in the current period and portends additional employment increases. When the average workweek is in a declining mode, it probably is signaling a potential slowdown in employment growth-or even outright declines in employment in case of recession.

Gains in average hourly earnings represent wage pressures. It is worth noting that these figures aren't adjusted for overtime pay or shifts in the composition of the workforce, which affects wages on its own. Market participants believe that a rising trend in hourly earnings will lead to higher inflation. But if increased wages are matched by productivity gains, producers likely will not increase product prices with wages because their unit labor costs are stable.

{kind=link}