{kind=link}

| Consensus | Consensus Range | Actual | Previous | |

| CPI - M/M | 0.3% | 0.2% to 0.3% | 0.3% | 0.2% |

| CPI - Y/Y | 2.4% | 2.4% to 2.6% | 2.4% | 2.4% |

| Ex-Food & Energy- M/M | 0.2% | 0.2% to 0.3% | 0.2% | 0.3% |

| Ex-Food & Energy- Y/Y | 2.5% | 2.4% to 2.5% | 2.5% | 2.5% |

Highlights

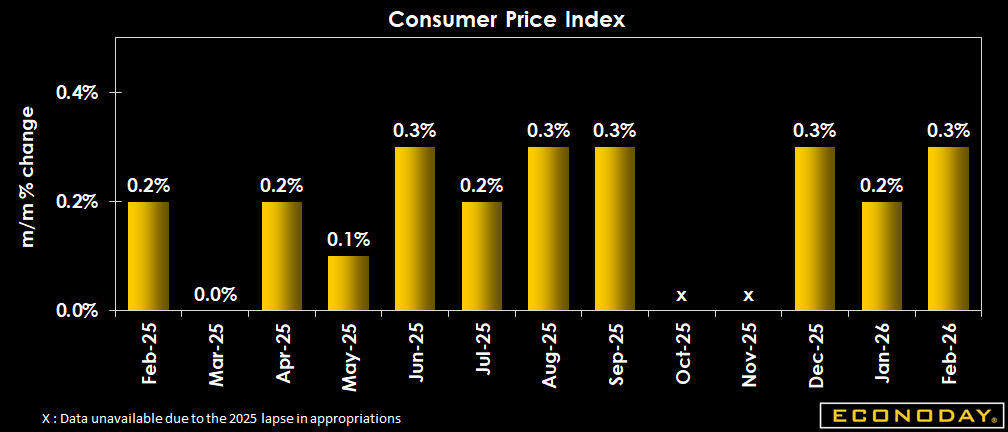

The February CPI report shows what is likely to be temporary stabilization in the pace of consumer price increases, with the headline and core numbers coming as expected. However, the impact of the ongoing war with Iran on energy prices, and the knock-on effect on the supply of other important commodities, as well as categories like airfare, should cause a spike in March consumer prices. Expect the Federal Reserve to remain on hold at its March 17-18 meeting to await clearer signals regarding the near-term path of inflation.

The Consumer Price Index in February rose 0.3 percent, up from the 0.2 percent pace set in January. The February CPI reading matched expectations for a 0.3 percent rise in the Econoday survey of forecasters.

Over the last 12 months, consumer prices are up 2.4 percent, compared to a 2.4 percent rise in January. Expectations in the Econoday survey were for also for a 2.4 percent increase.

Core CPI, excluding food and energy prices, is up 0.2 percent in February, following a 0.3 percent uptick in January. Consumer prices less food and energy rose 2.5 percent from February 2025, following a 2.5 percent year-over-year rise in January and as expected in the Econoday survey.

After a 0.2 percent increase in January, shelter costs maintained that rate of increase in February (and are up 3.0 percent year-over-year). Food prices rose 0.4 percent, after a 0.2 percent bump in January. Grocery prices are up 0.4 percent on a monthly basis in February, and +2.4 percent compared to a year ago, and restaurant prices rose 0.3 percent and surged 3.9 percent compared to February 2025.

Food prices overall increased by 3.1 percent compared to February 2025, following a 2.9 percent rise in January.

Energy costs rose 0.6 percent, following a 1.5 percent drop in January boosted by a 0.8 percent rise in gasoline prices, and an 11.1 percent surge in fuel oil prices.

Energy prices are up 0.5 percent year-over-year, following a 0.1 percent dip for the 12 months ending January.

Market Consensus Before Announcement

Inflation chugs along about the same as usual with CPI up 0.3 percent on the month and 2.4 percent on year versus 0.2 percent and 2.4 percent a month earlier.

Definition

The CPI is a measure of the change in the average price level of a fixed basket of goods and services purchased by consumers. Monthly changes in the CPI represent the rate of inflation for the consumer. Annual inflation is also closely watched.

The consumer price index is available nationally by expenditure category and by commodity and service group for all urban consumers (CPI-U) and wage earners (CPI-W). All urban consumers are a more inclusive group. The CPI-U is the more widely quoted of the two, although cost-of-living contracts for unions and Social Security benefits are usually tied to the CPI-W, because it has a longer history. Monthly variations between the two are slight.

The CPI is also available by size of city, by region of the country, for cross-classifications of regions and population-size classes, and for many metropolitan areas. The regional and city CPIs are often used in local contracts.

The Bureau of Labor Statistics also produces a chain-weighted index called the Chained CPI. This measures a variable basket of goods and services whereas the regular CPI-U and CPI-W measure a fixed basket of goods and services. The Chained CPI is similar to the personal consumption expenditure price index that is closely monitored by the Federal Reserve Board.

Description

The consumer price index is the most widely followed monthly indicator of inflation. An investor who understands how inflation influences the markets will benefit over those investors that do not understand the impact.

Inflation is an increase in the overall prices of goods and services. The relationship between inflation and interest rates is the key to understanding how indicators such as the CPI influence the markets- and your investments.

If someone borrows $100 dollars from you today and promises to repay it in one year with interest, how much interest should you charge? The answer depends largely on inflation as you know the $100 will not be able to buy the same amount of goods and services a year from now. The CPI tells us that prices rose 4.2 percent in the U.S. over 2007. To recoup your purchasing power, you would have to charge 4.2 percent interest. You might want to add one or two percentage points to cover default and other risks, but inflation remains the key factor behind the interest rate you charge.

Inflation (along with various risks) basically explains how interest rates are set on everything from your mortgage and auto loans to Treasury bills, notes and bonds. As the rate of inflation changes and as expectations on inflation change, the markets adjust interest rates. The effect ripples across stocks, bonds, commodities, and your portfolio, often in a dramatic fashion.

{kind=link}