{kind=link}

| Consensus | Consensus Range | Actual | Previous | |

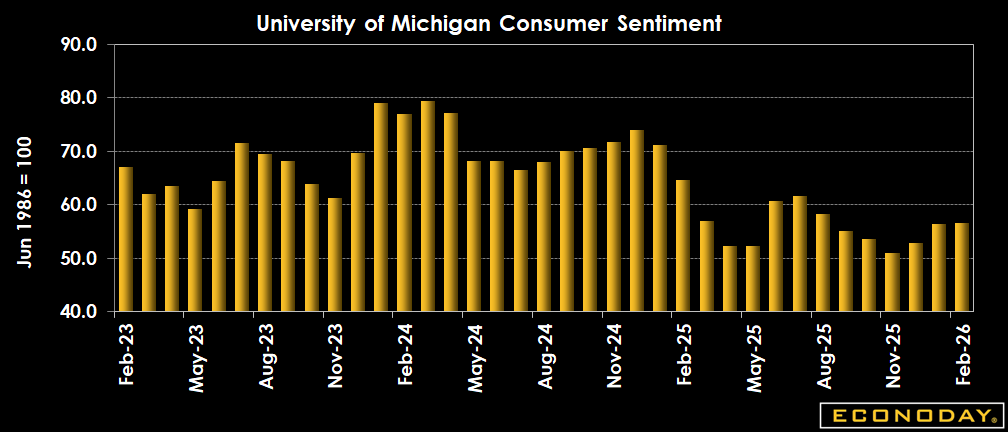

| Index | 57.0 | 54.3 to 57.3 | 56.6 | 57.3 |

| Year-ahead Inflation Expectations | 3.4% | 3.5% |

Highlights

U.S. consumer sentiment improved only slightly this month, with February's final reading coming in at 56.6 (revised down from 57.3) vs. 56.4 in January and 52.9 in December. This is below the consensus of 57.0 in the Econoday survey of forecasters. Stagnating confidence comes as consumers did not see any material improvement in economic conditions from January.

Sentiment is about 13 percent below a year ago and down 21 percent from January 2025.

A sizable month-to-month increase in sentiment for the largest stockholders was fully offset by a decline among consumers without stock holdings, the report noted. Similar divergences were seen across income and education, where higher-income or college educated consumers exhibited increases in sentiment while lower-income or less-educated counterparts did not.

Final year-ahead inflation expectations fell to 3.4 percent in February from 4.0 percent in January. This month's reading still exceeds those seen in 2024 and remains well above the 2.3-3.0 percent range seen in the two years pre-pandemic, the report said.

Long-run inflation expectations in February are steady at 3.3 percent from last month.

This is just above the 2.8 percent and 3.2 percent range seen in 2024. In 2019 and 2020, long-run inflation expectations were consistently below 2.8 percent, the report said.

Market Consensus Before Announcement

The final February report is expected to show sentiment index at 57.0 versus 57.3 in the preliminary February report compared with 56.4 in January final and a much stronger 64.7 a year ago.

Definition

The University of Michigan's Consumer Survey Center questions households each month on their assessment of current conditions and expectations of future conditions. Preliminary estimates for a month are released at mid-month and are based on about 420 respondents. Final estimates are released near the end of the month and are based on about 600 respondents.

Description

The pattern in consumer attitudes and spending is often the foremost influence on stock and bond markets. For stocks, strong economic growth translates to healthy corporate profits and higher stock prices. For bonds, the focus is whether economic growth goes overboard and leads to inflation. Ideally, the economy walks that fine line between strong growth and excessive (inflationary) growth.

This balance was achieved through much of the nineties and, in large part because of this, investors in the stock and bond markets enjoyed huge gains. It was during the late nineties that the consumer sentiment index hit its historic peak, reaching levels that were never matched during the subsequent 2001 to 2007 expansion nor during the long expansion following the Great Recession.

Consumer spending accounts for more than two-thirds of the economy, so the markets are always dying to know what consumers are up to and how they might behave in the near future. The more confident consumers are about the economy and their own personal finances, the more likely they are to spend. With this in mind, it's easy to see how this index of consumer attitudes gives insight to the direction of the economy. Just note that changes in consumer confidence and retail sales don't move in tandem month by month.

{kind=link}