{kind=link}

| Consensus | Consensus Range | Actual | Previous | Revised | |

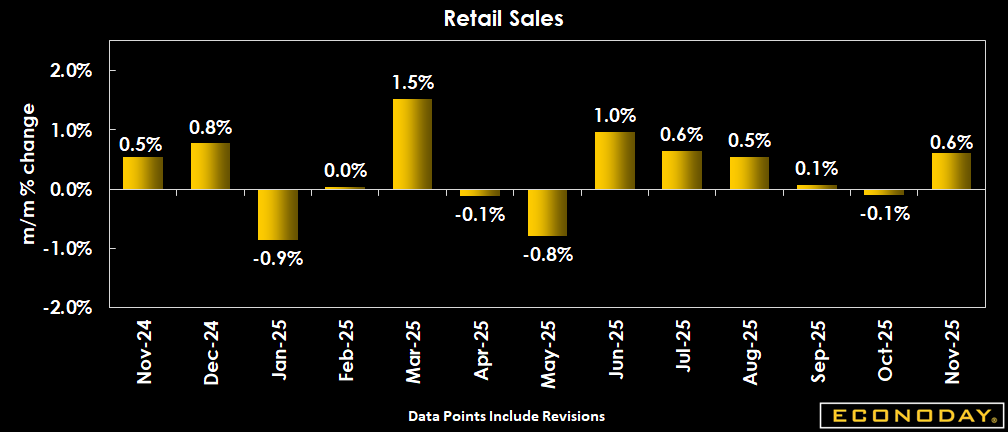

| Retail Sales - M/M | 0.2% | -0.5% to 0.4% | 0.6% | 0.0% | -0.1% |

| Ex-Vehicles - M/M | 0.3% | 0.1% to 0.4% | 0.5% | 0.4% | 0.2% |

| Ex-Vehicles & Gas - M/M | 0.2% | 0.1% to 0.4% | 0.4% | 0.5% | 0.4% |

Highlights

U.S. retail sales came in stronger than expected, and the underlying data is encouraging with solid core retail sales when gasoline and motor vehicles are stripped out. The report once again paints the picture of decent consumer spending combined with higher prices due to tariffs boosting sales revenues. This, combined with stubborn annual inflation numbers, will prompt the Fed to proceed cautiously on additional rate cuts in the absence of troubling labor market data.

U.S. November retail sales rebounded by 0.6 percent, following the revised 0.1 percent monthly dip reported for October (previously flat), and vs. the +0.2 percent consensus in the Econoday survey of forecasters.

Compared to a year ago, November retail sales are up 3.3 percent, compared to October's revised 3.3 percent increase (previously +3.5 percent).

Core retail sales, removing autos and gasoline sales, increased 0.4 percent last month matching the revised reading in October (previously reported as +0.5 percent). Core retail sales are up 4.4 percent on an annual basis in November compared to a 3.9 percent y/y jump in October (revised down from +4.2 percent).

Auto sales bounced back by 0.8 percent in November, not enough to erase October's 1.6 percent contraction, but fell 1.1 percent vs. last year. Activity remains sluggish, as rising prices for both new and used cars continue to weaken consumer demand.

Sales were up 0.9 percent for clothing stores, +1.9 percent for sporting goods, flat for electronics stores, and just a 0.1percent uptick in grocery sales. Building material & garden equipment and supplies dealer saw sales increase 1.3 percent. Furniture stores experienced a 0.1 percent decline, but miscellaneous store retailers saw a 1.7 percent jump, building on a 1.5 percent rise in October.

E-commerce sales rose 0.4 percent in November, following a 1.0 percent rise in October, and they are 7.2 percent higher than a year ago. This is another tariffs-impacted sector, where increased prices following the elimination of the de minimis exemption for imported goods below $800 has likely inflated sales data.

Excluding gasoline, retail sales increased 0.6 percent, after October's flat reading, and increased 3.3 percent from November 2024 vs. +3.4 percent on an annual basis in October.

Stripping out purchases of motor vehicles and parts, sales rose 0.5 percent compared to a 0.2 percent bump (previously +0.4 percent) in October. On an annual basis, retail sales ex-autos are up 4.3 percent, speeding up from October's 3.7 percent pace.

Market Consensus Before Announcement

Modest increases expected with sales up 0.2 percent.

* Originally scheduled for 12/17/2025

Definition

Retail sales measure the total receipts at stores that sell merchandise and related services to final consumers. Sales are by retail and food services stores. Data are collected from the Monthly Retail Trade Survey conducted by the U.S. Bureau of the Census. Essentially, retail sales cover the durables and nondurables portions of consumer spending. Consumer spending typically accounts for about two-thirds of GDP and is therefore a key element in economic growth. Of special attention is the control group; this is an input into the consumer spending component of GDP and excludes food services, autos, gasoline and building materials.

Description

Consumer spending accounts for more than two-thirds of the economy, so if you know how the consumer sector is faring, you'll have a pretty good handle on where the economy is headed. Needless to say, that's a big advantage for investors.

The pattern in consumer spending is often the foremost influence on stock and bond markets. For stocks, strong economic growth translates to healthy corporate profits and higher stock prices. For bonds, the focus is whether economic growth becomes excessive and leads to inflation. Ideally, the economy walks that fine line between strong growth and excessive (inflationary) growth. Retail sales not only give you a sense of the big picture, but also the trends among different types of retailers. Perhaps auto sales are especially strong or apparel sales are showing exceptional weakness. These trends from the retail sales data can help you spot specific investment opportunities, without having to wait for a company's quarterly or annual report.

Balance was achieved through much of the nineties. For this reason alone, investors in the stock and bond markets enjoyed huge gains during the bull market of the 1990s. Retail sales growth did slow down in tandem with the equity market in 2000 and 2001, but then rebounded at a healthy pace between 2003 and 2005. By 2007, the credit crunch was well underway and starting to undermine growth in consumer spending. Later in 2008 and 2009, the rise in unemployment and loss of income during the recession also cut into retail sales. Spending rebounded in 2010 and 2011 but was constrained by lingering high unemployment.

Importance

Retail sales are a major indicator of consumer spending trends because they account for nearly one-half of total consumer spending and approximately one-third of aggregate economic activity. The control group for retail sales (which excludes restaurants, vehicles, gasoline and building materials) is an input into GDP and offers a narrower look at nondiscretionary spending.

Interpretation

Strong retail sales are bearish for the bond market, but favorable for the stock market, particularly retail stocks. Sluggish retail sales could lead to a bond market rally, but will probably be bearish for the stock market.

Retail sales are subject to substantial month-to-month variability. In order to provide a more accurate picture of the consumer spending trend, follow the three-month moving average of the monthly percent changes or the year-over-year percent change. Retail sales are also subject to substantial monthly revisions, which makes it more difficult to discern the underlying trend. This problem underscores the need to monitor the moving average rather than just the latest one month of data.

In an attempt to avoid the more extreme volatility, economists and financial market participants monitor retail sales less autos (actually less auto dealers which include trucks, too.) Motor vehicle sales are excluded not because they are irrelevant, but because they fluctuate more than overall retail sales. In recent years, many analysts consider the core series to be total less autos and less gasoline service station sales. The latter is volatile due to swings in oil and gasoline prices.

Price changes affect the real value of retail sales. Watch for changes in food and energy prices which could affect two large components among nondurable goods stores: food stores and gasoline service stations. Large declines in food or energy prices could lead to declines in store sales which are due to price, not volume. This would mean that real sales were stronger than nominal dollar sales.

Since economic performance depend on real, rather than nominal growth rates, compare the trend growth rate in retail sales to that in the CPI for commodities.

{kind=link}