Trading the AIR Total Return futures

{kind=link}

Adjusted Interest Rate Total Return futures, or AIR TRFs, provide total return exposure with an overnight floating rate built in. AIR TRFs replicate the economics of an equity index swap but offer the benefit of being a listed, centrally cleared futures contract.

As a refresher, AIR Total Return futures are comprised of three components:

- S&P 500 Total Return Index performance

- Daily accrued financing

- Daily financing spread adjustment

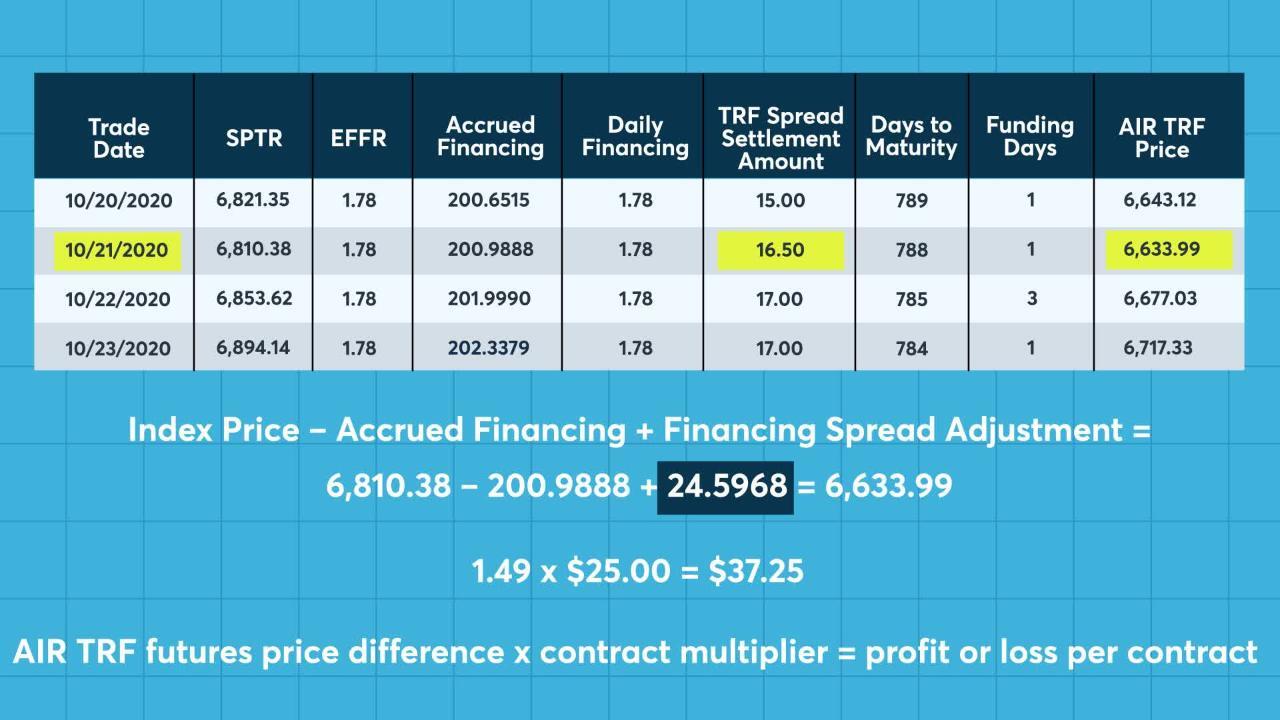

Trade Example

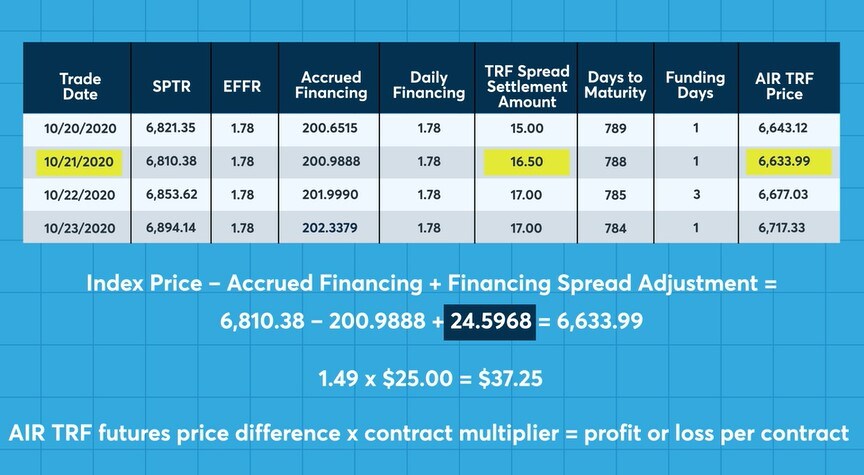

Assume the trade date is October 21, 2020, and a client bought the Dec 2022 AIR S&P 500 TRF at a BTIC price of 15.5 basis points.

{kind=link}

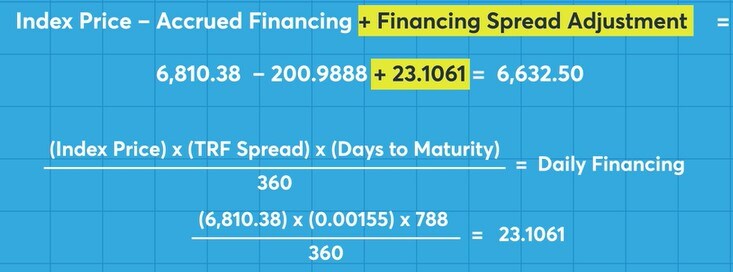

This would equate to an AIR TRF price of 6632.50. The financing spread adjustment, or FSA, was calculated as 23.1061.

{kind=link}

Assume the TRF spread settled on October 21 at 16.5 basis points. The daily settlement price of the AIR TRF futures contract would be 6,633.99. This positive price difference of 1.49 times the contract multiplier of $25 equals a profit per contract of $37.25.

{kind=link}

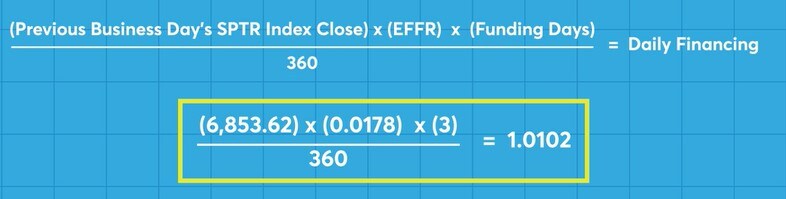

Assume on the next day, October 22, the accrued financing has increased by the daily financing value and is now equal to 200.9990. The daily financing amount is determined by (previous business day’s SPTR index close) x (EFFR) x (funding days)/360. The number of funding days in this case is three, as the settlement cycle accounts for the weekend.

{kind=link}

The daily financing amount is 1.0102. If the TRF spread settled at 17, the AIR TRF price would now be 6,677.03.

The additional change in contract value from the previous day’s settlement is 43.04 x $25 = $1076.

{kind=link}

Summary

This shows how the TRF spread is the traded component in the Adjusted Interest Rate (AIR) Total Return futures contract. The transparency of the equity financing level along with the built-in floating rate provide similar economics and transactional handshake to a total return swap. AIR Total Return futures offer a cost effective and capital-efficient vehicle for total return exposure.