Position Limits - Aggregation of Contracts and Table

{kind=link}

Position Limits are calculated on a net futures-equivalent basis by contract and include contracts that aggregate into one or more base contracts according to the aggregation ratio(s) as set forth in the Position Limit Tables. The aggregation of contracts for Spot Month, Single Month, and All Month are noted in the Table.

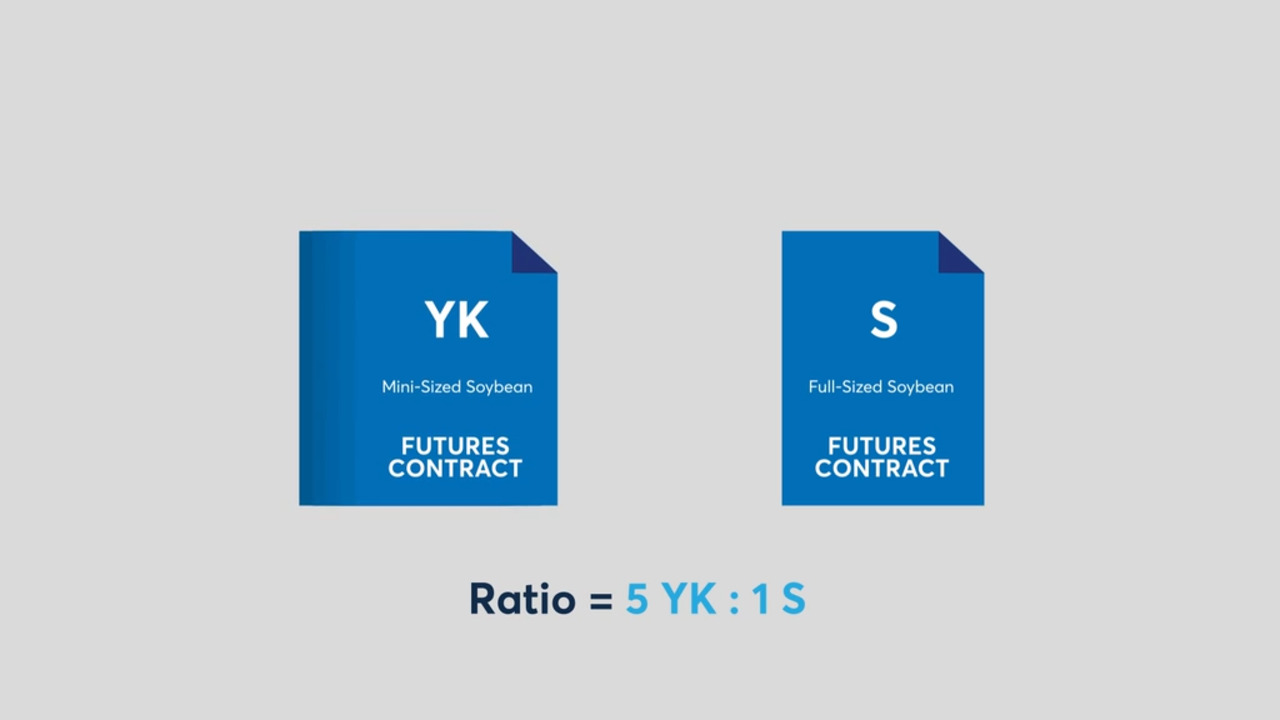

Using the spot month as an example, for a contract that aggregates into only one base contract during the spot month, the base contract will be identified in the “Spot Month Aggregate Into Futures Equivalent Leg (1)” column of the Table and will denote a positive correlation with the base contract. The aggregation ratio for the Leg (1) base contract will be identified in the “Aggregate Into Ratio Leg (1)” column of the Table.

For contracts that aggregate into two separate base contracts during the spot month, the base contract noted in the “Spot Month Aggregate Into Futures Equivalent Leg (1)” column of the Table will denote a positive correlation, and the aggregation ratio for the Leg (1) base contract will be identified in the “Aggregate Into Ratio Leg (1)” column of the Table. The base contract noted in the “Spot Month Aggregate Into Futures Equivalent Leg (2)” column of the Table will denote a negative correlation with respect to the base contract, and the aggregation ratio for the Leg (2) base contract will be identified in the “Aggregate Into Ratio Leg (2)” column of the Table.

If the portfolio also includes position in Options on futures, it would be aggregated into the underlying futures contracts in accordance with the Table on a delta equivalent value for the relevant Spot Month, Subsequent Spot Month, Single Month and All Month position limits. If a position exceeds position limits as a result of an option assignment, market participants are allowed to liquidate the excess position within one business day without being considered in violation. Additionally, if at the close of trading, a position that includes options exceeds position limits when evaluated using the delta factors as of that day’s close of trading but does not exceed the limits when evaluated using the previous day’s delta factors, then the position shall not constitute a position limit violation.

This is part of a course on position limits and accountability levels. For official regulatory guidance, reference the applicable Market Regulation Advisory Notice.