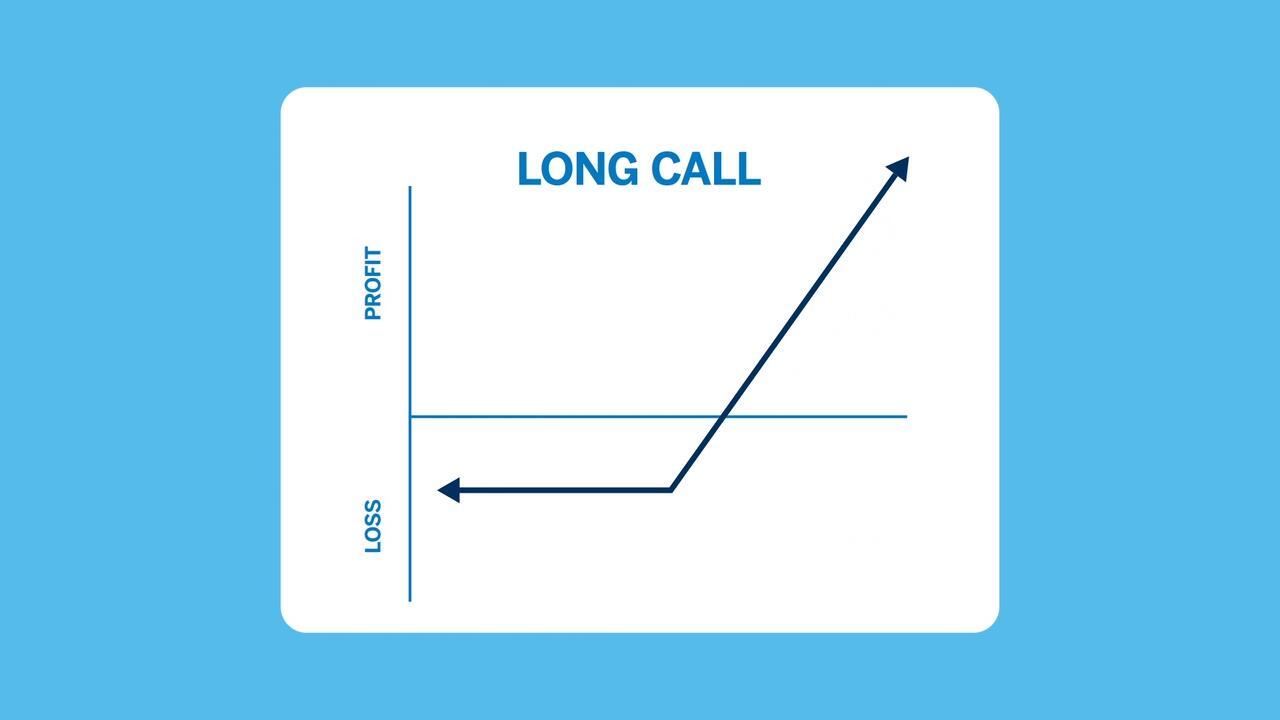

Long Call Scenarios

How Underlying Price and Volatility Affect an Option's Price

{kind=link}

As review, an option gives the owner the right, but not the obligation to buy or sell the underlying futures contract at a pre-determined price with a set expiration date. When you buy a call, you have established a bullish position - that is, you want the underlying contract to increase in value, or rally.

Changes in option prices are driven by multiple variables including the underlying price, interest rates, passage of time and changes in the expected volatility.

The following scenarios focus on how changes in the underlying price and implied volatility affect the option’s price.

When trading options, all variables need to be considered, and the combination of these variables may lead to different results. As you can see in the videos below, underlying price is the biggest driver of an option’s value, but implied volatility also has an impact on the premium.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

When trading options, all variables need to be considered, and the combination of these variables may lead to different results. As you can see in the video below, underlying price is the biggest driver of an options value, but the implied volatility also has an impact on the option premium.

{kind=link}

A trader purchased a gold 1300 call for 14.1. This is equal to $1410. The call has 41 days until expiration, implied volatility is around nine and the underlying price is 1295.90.

The underlying price increased from 1295.90 to 1305.90 and the call’s premium increased from 14.1 to 19.2. When the underlying price decreased from 1295.90 to 1285.90, the call’s premium decreased from 14.1 to 9.9.

The volatility increased from 9 to 10 and the call’s premium increased from 14.1 to 16. When the volatility decreased from 9 to 8, the options premium also decreased from 14.1 to 12.5.

The underlying price increased from 1295.90 to 1310.90. Volatility increased from 9 to 11. The call’s premium increased from 14.1 to 25.7.

The underlying price increased from 1295.90 to 1310.90. Volatility decreased from 9 to 7. The call’s premium increased slightly from 14.1 to 19.9.

The underlying price decreased from 1295.90 to 1285.90. Volatility increased from 9 to 11. The call’s premium decreased from 14.0 to 12.9.

The underlying price decreased from 1295.90 to 1290.90. Volatility decreased from 9 to 7. The call’s premium decreased from 14.1 to 8.7.