Understanding Options Expiration (Profit and Loss)

{kind=link}

The profit and loss of an option position at expiration is a function of the original premium and the difference in price between the futures contract and the strike price of the option.

Selling a Call Scenario

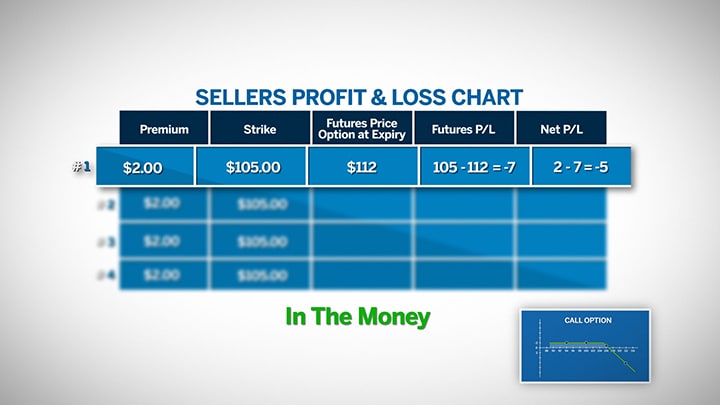

Suppose you sell the 105 call for $2 in premium. The maximum profit potential for this trade is $2. Let’s look at a few different possible outcomes for the futures price at expiration.

To understand the profit and loss, we look at the math for each of these potential scenarios. You sold the option and collected $2 in premium. For each scenario the premium column will be $2 and the strike price is $105. This is the price at which you are obligated to sell the futures contract if you are assigned.

{kind=link}

Sell Call Scenario One

In scenario one, the futures price at option expiry is $112. This option will be in the money and you would be assigned. You will sell the future for $105 creating an instantaneous $7 loss on the future. You collected $2 in premium and lost $7 on the future, so your net loss will be $5.

{kind=link}

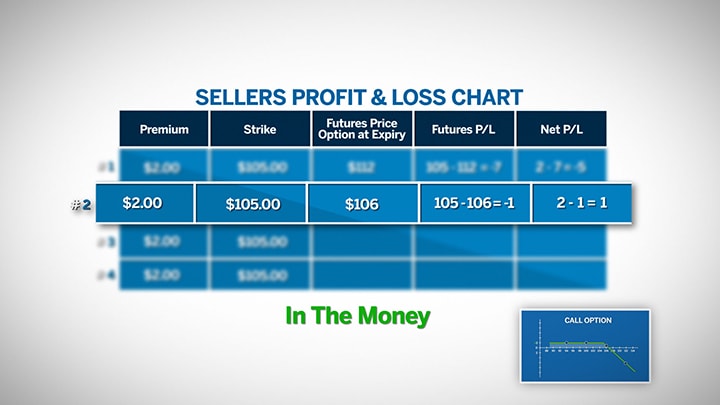

Sell Call Scenario Two

For scenario 2 we see the futures price at option expiry is $106. This option is also in the money and again you would be assigned. You will sell the future at the strike price of $105 and have a loss of $1 on the future. Since you collected $2 in premium you will have a net profit of $1.

{kind=link}

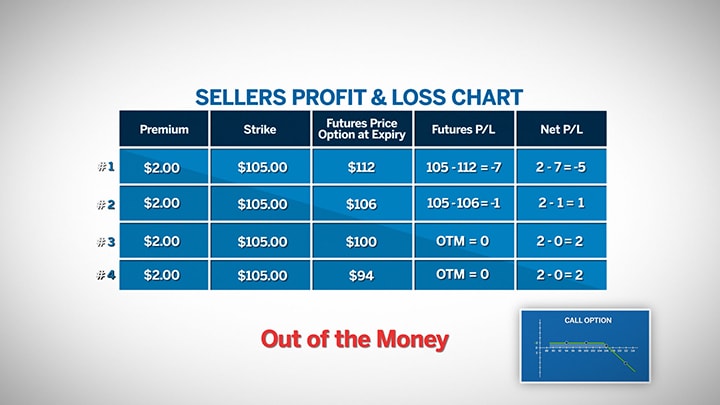

Sell Call Scenario Three and Four

In scenario 3, the futures price at option expiry is $100. This option is out of the money and will not be exercised. There will be no loss from futures. Therefore, your $2 collected in premium will become your total profit.

Scenario 4 has the futures price at $94. This example is like scenario 3; the option will be out of the money and will not be exercised. Again, your final net position will be a profit of $2.

{kind=link}

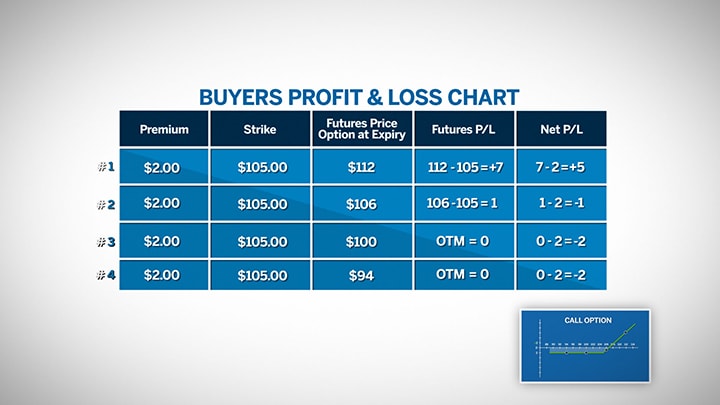

Buying a Call Scenario

Now let’s look at the same group of scenarios but from the buyer’s perspective.

In this case you buy a call at $105, and pay a $2 premium to the seller. We will look at your profit and loss potential using the same futures prices at option expiration.

Buy Call Scenario One

In scenario one, the futures price at option expiration will be $112. This option is in the money. You exercise the option at $105. With the futures at $112, this will result in a gain of $7. If you subtract the $2 premium paid for the option, your net profit will be $5.

Buy Call Scenario Two

For scenario two, the futures price at option expiration will be $106. Again, this option is still in the money. You exercise this option at $105 and make $1. You paid $2 in premium, so your net will be a loss of $1.

Buy Call Scenario Three and Four

Scenarios three and four are both out of the money options. In both cases you would not exercise the option. Your net loss has been capped at $2 which is the full premium paid for the option

{kind=link}

Summary

These scenarios show you two views of profit and loss from either side of the same transaction. When looking at profit and loss potential of an option position at expiration, you will need to consider the original premium and the difference in price between the futures contract and the strike price of the option.