{kind=link}

Will the U.S. be the home of LNG Price Formation

Will the US be the home of LNG Price Formation?

The nature of price formation in the global LNG market is increasingly the subject of both industry and academic attention. As the market shows greater appetite to gradually transition from oil indexation towards gas-to-gas pricing, many alternative price references have emerged as regional price signals reflecting respective markets; the question remains as to which region or market among the three – Europe, Asia, or the U.S. – is best positioned to host the core price-discovery benchmark.

This article examines how a U.S new business model is moving the LNG market toward greater competitiveness and efficiency by transforming the anatomy of LNG trading transactions, also referred to as the market microstructure. This has positioned the U.S to be the most likely anchor for price formation for the global LNG market.

Price formation in the LNG market is a complex process as the landscape is still evolving. Building a benchmark for LNG depends on the well-functioning, competitiveness, and efficiency of three endogenous and exogenous factors: supply chain, sound delivery system/infrastructure relevance, and market participation.

U.S. LNG developers are innovating in their contractual arrangements and project structuring. This has given birth to a new U.S. institutional model founded around three pillars: volume flexibility, destination optionality, and market competitiveness.

US LNG Supply Chain

The current natural gas supply level has positioned U.S among the world’s top gas producers. This has considerably reduced the marginal cost of producing LNG and has substantially lowered the price of an LNG cargo. Additionally, U.S. output is produced through new supply chain models. The commercial structure of the supply chain of an LNG project is very important in understanding the LNG market because it defines the return and risk allocation among the investors or stakeholders at each link of the chain.

LNG projects are capital intensive investments which require financing typically through forming joint ventures or partnerships. The decision to adopt any project structure depends on a confluence of various considerations including legal, fiscal, financing, commercial, and the risk appetite of participants. U.S. LNG developers have adopted innovative business models and novel claues to enhance flexibility and competitiveness.

1. Traditional Integrated Market Structure

LNG project structures have traditionally relied on a vertically-integrated model centered around ownership concentration. As such, project owners control assets throughout the supply chain: from upstream resources, the liquefication plants, to sometimes even the shipping element. Project developers share costs and revenues across the supply chain and hold the title of the natural gas from the wellhead to the sale of the LNG.

This Integrated market structure is based on long-term rigid agreements known as LNG sale and purchase agreements (SPAs), which typically contain destination restrictions that ensure that a specific gas volume is liquefied and shipped to a specific market via commercial transactions with long-term buyers such as utilities or gas companies. While this point-to point chain offers the buyer reliability of delivered volumes and secures the seller a constant cash-flow stream, this design is solely for supply security and is consumption driven. This model does not enable suppliers or buyers to capture any arbitrage opportunity as the market price moves.

2. U.S. Merchant Market Structure

Under the merchant market structure, a project developer owns the liquefaction facility and procures feedstock gas from producers via natural gas sales agreements at market prices. The merchant then liquifies the gas into LNG and subsequently sells it to different off-takers including portfolio players (aggregators), utilities, etc. under LNG SPAs. This business model is driven by a series of arm’s-length transactions that aim to capture any potential gain based on the competitiveness of spread between the input (gas) and the output (LNG).

3. U.S. Tolling Model

Under the U.S. tolling model, the liquefaction plant does not take title of the LNG. Instead, it processes feedstock gas supplied by the LNG buyer/off-taker for a tolling fee based on a negotiated rate. This is analogous to the role of the natural gas pipeline which does not own gas but provides transportation services to shippers. Among the benefits of this project structure is the flexibility and diversity in ownership throughout the supply chain. The LNG plant operator is not tied to any particular upstream source and marketer.

Under both market frameworks, each component of the supply chain operates independently and efficiently through competitive market offerings. In addition, the ownership structure is also diverse.

4. Equity or Tellurian Market Model

This market model was recently introduced by two main project developers: Tellurian and LNG Canada in 2018. This structure offers the buyer an equity stake in the project (i.e. 65-70% in the case of Tellurian), with its integrated components: upstream equity gas, through liquefaction to shipping, marketing and trading. This project structure looks at return and risk across the supply chain instead of looking at each chain link separately. LNG buyers buy equity and receive LNG in proportion to their stake ownership. Designing such a novel model was an attempt to attract investors with equity ownership to secure financing in a low-priced environment that currently favors the buyer.

Volumetric Flexibility & Destination Optionality

The U.S. model fundamentally relies on volumetric and destination optionality, which is the cornerstone of spot trading. The U.S. SPA is based on an enhanced version of the take-or-pay (ToP) contract structure. This contract construct stipulates that the buyer is contracted to lift an annual quantity called the “annual contract quantity” or “ACQ” at a pre-determined price or else to pay any shortfalls. With enough advance notice – usually two months – the ACQ is subject to downward/upward adjustment rights or cancellation rights which can be exercised by the buyer based on global seasonal demand. The contract structure of SPAs offers flexibility to both the buyer and the seller. The buyer has the optionality to lift LNG or not, depending on current demand, without breaching any contractual obligations. The seller will collect cash flows either as LNG sale proceeds or as cancellation fees, irrespective of whether the buyer takes delivery of LNG or not. The embedded destination flexibility of U.S. SPAs allows cargoes to be redirected where it is economically favorable depending on spot price signals. This means they can be sold multiple times before they are lifted from the terminal. These factors have contributed to the rise of LNG spot trading and created new permutations between buyers and sellers.

New Developments of LNG Cargo Trading

1. Rise of Portfolio Optimization

Significant volumes of contracted U.S. LNG are owned by portfolio optimizers. These aggregators are generally large energy companies (examples Shell, BP, Total) which own upstream assets or capacity and have long term off-take agreements. These aggregators are driven by margin optimization and act as market-makers. They engage in short-term trading to capture price arbitrages using sophisticated strategies like buying cargoes on term contracts and selling on a spot basis or vice versa. LNG portfolio optimizers play a key role in reshaping the microstructure of LNG trade as they act as market makers. Their importance is analogous to the role played by traditional markers in the natural gas market back in 1990s. Portfolio optimizers’ ability to raise capital at lower costs enhances their marketing capabilities and enables them to be the conduit between the primary market and the secondary/resale market. This has led to a progressive increase in LNG spot trading, which is also referred to as the swing market.

2. Short Term Trade Duration

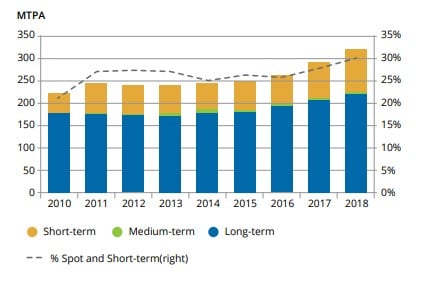

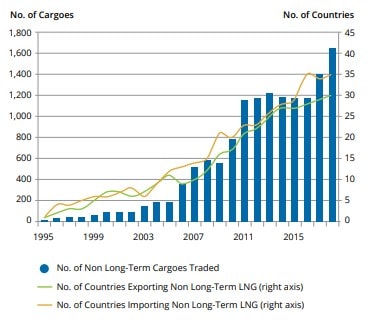

While the LNG market has traditionally relied on long-term contracts, spot1 trading has been growing for the second consecutive year and reached 99 MT in 2018. This represents an increase of 31% of global trade. However, the largest growth came from the U.S. where approximately 70% of Sabine Pass exports were traded spot in 2017 due largely to the flexibility of U.S LNG volume which facilitated cargo diversions coupled with the increasing activity of portfolio optimizers who own significant capacity in U.S. Gulf Coast (“USGC”). Figure 1 and Figure 2 show that cargoes traded with short-term duration are getting momentum while the medium term is increasing at a slower pace.

Figure 1: Short, Medium and Long-Term Trade, 2010-2018

{kind=link}

Source: IGU

Figure 2: Short-term/Spot Trading by Number of Cargoes & Countries

{kind=link}

Source: IGU

3. U.S. Tolling Model

Under the U.S. tolling model, the liquefaction plant does not take title of the LNG. Instead, it processes feedstock gas supplied by the LNG buyer/off-taker for a tolling fee based on a negotiated rate. This is analogous to the role of the natural gas pipeline which does not own gas but provides transportation services to shippers. Among the benefits of this project structure is the flexibility and diversity in ownership throughout the supply chain. The LNG plant operator is not tied to any particular upstream source and marketer.

Under both market frameworks, each component of the supply chain operates independently and efficiently through competitive market offerings. In addition, the ownership structure is also diverse.

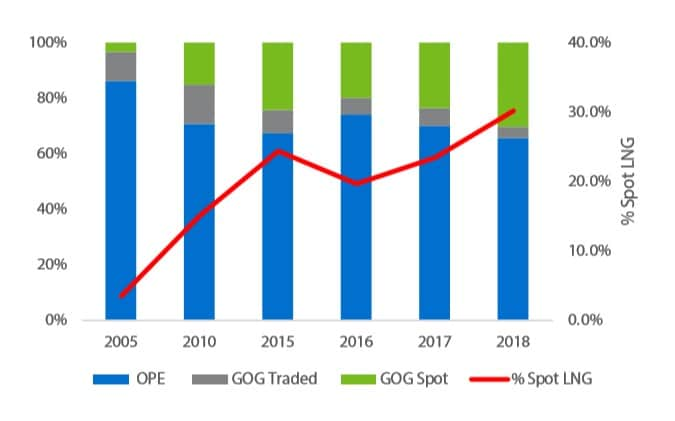

Figure 3: World Price Formation 2005 to 2018 – Spot LNG Imports

{kind=link}

Source: IGU

US SPAs introduced a new pricing approach based on a Henry Hub-linked LNG formula. Cheniere was the first US supplier to introduce a Henry Hub-linked LNG formula. This formula is based on off-takers that are contracted to lift LNG and pay an approximate fixed fee between $2.25 to $3.5 per MMBtu plus a charge of 115% of the Henry Hub price. The fixed “take-or-pay” fee is paid irrespective of lifted volume and can be considered as a sunk cost. The Henry Hub price and 15% charge represent the cost of procuring feedstock gas that is variable depending on the volume lifted. Shipping and re-gasification costs are covered by the downstream participant or off-taker.

An important implication of such structure is that the trading determination process is driven by the spread or margin between Henry Hub versus regional spot LNG prices and the variable costs (shipping, regas) while ignoring the fixed fee which is considered as a sunk cost. In another word, this pricing structure can essentially be viewed as a spread option where the strike is the variable costs (shipping, liquification, and regas). Given the destination optionality embedded in U.S. SPAs, off-takers can elect to take any contracted LNG if the economics of exporting gas are favorable or the spread option is in-the-money

Interconnectivity & Infrastructure Relevance

The development of price benchmarks in energy in general is intrinsically linked to the physical market and its commercial implications. Well-developed infrastructure and the proximity to supply ensure three elements: (1) alignment to the balance of supply and demand, (2) smoothness of price discovery formation, and (3) enhancement of price response.

Most U.S. projects are situated in the Gulf of Mexico, except Cove Point which is in the northeast. The Gulf of Mexico has logistical and infrastructural advantages and encompasses one of the most developed energy infrastructures in the world. The region has a concentration of facilities throughout the gas supply chain, including production upstream, gathering and processing plants, extensive pipeline system, storage, industrial access. In addition, the U.S. Gulf Coast possesses a highly-skilled workforce.

The competitiveness of U.S. LNG exports was also enhanced by the recent Panama Canal expansion, which has substantially reduced the voyage time, distance and costs of LNG vessels to travel from the USGC to the Pacific Basin. According to the U.S. Energy Information Administration (“EIA”), the newly expanded canal will be able to handle 90% of the world’s current LNG tankers with a shipping capacity of 3.9 Billion cubic feet (“Bcf”). The expansion considerably reduces the voyage time to Japan from 34 days to 20 days and shortens the distance from 16,000 to 9,000 miles compared to traversing the Suez Canal or around the Cape of Good Hope, which adds 12-13 days to the shipping time and more cost. With respect to the voyage to South America, transit through the Panama Canal shortens the duration from 20 days to 8-9 days and from 25 days to 5 days going to Chile and Colombia/Ecuador respectively. Therefore, the USGC has both physical capabilities and robust supply, which allows it to attract the strong physical trade volume needed for benchmark creation.

Conclusion

Oil indexation is losing its luster and becoming an archaic mechanism which is less likely to survive against hub pricing in the long run. With the US LNG institutional model profoundly changing LNG contractual, pricing, and trading apparatus, the USGC has the potential to become a major physical hub for global LNG price formation due its strategic location and easy access to flexible supply.

References

- Deals under 2 years