{kind=link}

Why Cushing Matters: An Update on the WTI Benchmark

In 2023, global oil markets have been easing, a sharp contrast to 2022 which was marked by high volatility and record low inventories. High frequency data is pointing to oil inventory builds around the globe, though market experts disagree on how long this may last. For now, growing production has caught up to demand levels dampened by weaker economic conditions and a mild winter. The arbitrage price signals have responded to the shift in market fundamentals to redirect barrels to flow into storage.

The shift in the oil market is reflected in the price signals from the NYMEX Light Sweet Crude Oil Futures contract (also called “WTI futures”), which is based on physical delivery of WTI-type crude oil at the Cushing hub. At futures expiration, the exchange matches the buyers and sellers who elect to make or take delivery of physical oil. The delivery requirement of WTI futures is a direct link to the underlying physical market.

A regulated futures contract provides each buyer and seller with a financial guarantee for their trades. Even during the most extreme market conditions, WTI futures ultimately provide for convergence between the futures and cash markets, performing the critical function as the central clearing mechanism for buyers and sellers in the crude oil market. This paper provides further information on the strengths of Cushing as both a trading and storage hub, most notably its pipeline connectivity, storage logistics, and price discovery role as a global benchmark. These strengths remain key as market participants hedge price risk in the volatile global oil markets.

Overview of Cushing logistics

At the heart of the global pricing network, the Cushing hub provides the physical delivery mechanism for the NYMEX WTI futures contract. When the WTI futures contract was first listed in 1983, Cushing was already a vibrant hub for cash market trading of crude oil with a network of pipelines, refineries, and storage terminals: the obvious choice for the delivery point. Today, Cushing has grown to become the key nexus for the global crude oil market, with over 30 inbound and outbound pipelines and 16 major storage terminals.

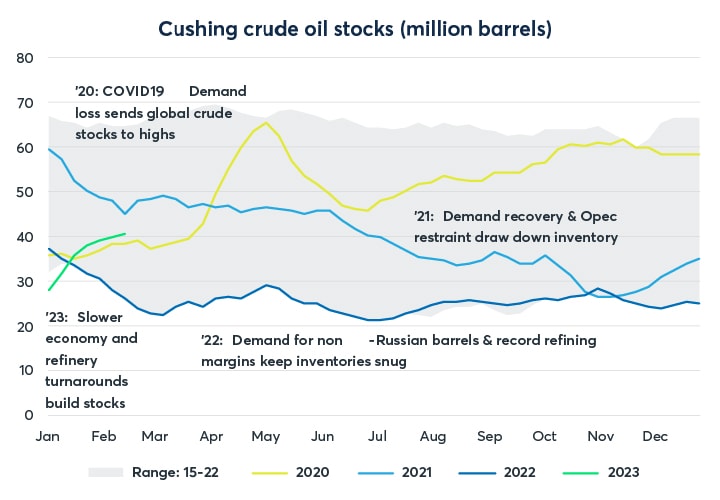

According to the U.S. Energy Information Administration (“EIA”) as of March 2022, the working storage capacity in Cushing is 78 million barrels, with 94 million barrels of total shell capacity. Many industry sources cite Cushing shell capacity in excess of 100 million barrels. Cushing stock levels follow a pattern that should be familiar to most watchers of global crude markets. Stocks rose rapidly to a historical high in the spring of 2020, when COVID-19 halted global fuel demand and refineries slowed or shut. Inventories around the world swelled at an unprecedented rate, calling on the tanker fleet and SPR facilities to absorb excess volumes. The excess inventory that built up during COVID gradually drew down over 2021 as refinery demand returned and Cushing reached a low point of 21 million barrels in the middle of 2022. After remaining snug for most of 2022, global inventories have been on the upswing in 2023.

{kind=link}

The pipeline infrastructure in the Cushing market is expansive. According to RBN Energy, there are 20 inbound pipelines, 16 outbound pipelines, and more than 30 intra-Cushing pipelines connecting production from most major North American onshore basins with the larger refining and export markets in the Gulf Coast and Midcontinent refineries. Nearly 4 million barrels per day (b/d) of inbound pipeline capacity to Cushing delivers crude oil streams produced in Canada and the U.S. shale oil areas, including the Bakken, Niobrara, and Permian Basins.

Key crude oil pipelines inbound to Cushing

| INCOMING PIPELINES | CAPACITY (b/d) | OWNER |

| Flanagan South (Canada/Bakken) | 660,000 | Enbridge |

| Keystone (Canada / from Steele City, NE) | 590,000 | TC Energy |

| Basin Pipeline (Permian) | 450,000 | Plains |

| Pony Express Pipeline (Niobrara/Bakken) | 450,000 | Tallgrass |

| Saddlehorn Pipeline (DJ Basin) | 290,000 | Magellan/Plains etc |

| STACK Pipeline (Cashion) | 250,000 | Plains, PSX |

| Glass Mountain | 210,000 | Navigator Energy/BlackRock |

| Spearhead Pipeline (Canada/Bakken) | 193,000 | Enbridge |

| Mississippian Lime Pipeline | 175,000 | Plains |

| Centurion North Pipeline (Permian) | 170,000 | Lotus Midstream |

| Grand Mesa Pipeline (DJ Basin) | 150,000 | NGL Energy Partners |

| White Cliffs Pipeline (Niobrara) | 100,000 | Energy Transfer |

| STC Pipeline (Stroud to Cushing) | 90,000 | U.S. Development |

| Enable & Springer to Cushing lines | 64,000 | CVR |

| Great Salt Plains | 53,000 | GSM |

*TOTAL In-Bound Capacity: 3.9 Million barrels per day

It is not just the storage or pipeline capacity that make Cushing the critical hub for the global oil benchmark, but also the interconnectivity between a diverse mix of operators at Cushing. The network of over 30 pipelines within Cushing provide unrivaled flexibility and optionality to segregate, batch, and blend barrels, allowing participants to respond to market conditions and meet the needs of the global refining network. Cash market trading within Cushing reflects this liquidity. Argus recorded 1.3 million barrels per day of spot month transactions at Cushing for March 2023 delivery, exceeding those for any other pricing point, and up 17% from a year ago.

Outbound pipeline capacity from Cushing has continued to expand, now up to over 3.3 million b/d. A portion of the outbound pipelines directly or indirectly feed Midwest refineries, while the largest pipelines flow onward to the U.S. Gulf Coast. Energy Transfer’s Cushing South pipeline is the latest addition to the Cushing-to-Gulf Coast lines, adding 120,000 b/d by 2022. The Gulf Coast markets have grown in increasing prominence with the rise in U.S. export supplies, which have quadrupled in the last five years and catapulted the U.S. to become the largest supplier of light sweet crude oil to the globe.

Key crude oil pipelines outbound from Cushing

| OUTGOING PIPELINES | CAPACITY | OWNER |

| Seaway Pipeline (to Houston Area) | 950,000 | Enterprise |

| Keystone MarketLink (to Houston Area) | 700,000 | TC Energy |

| Ozark (to Wood River, IL) | 360,000 | MPLX |

| Red River Pipeline (to Longview) | 235,000 | Plains |

| Diamond Pipeline (to Memphis) | 200,000 | Plains |

| Osage (to Eldorado, KS) | 175,000 | Holly Energy Partners |

| BP#1 (to Chicago) | 180,000 | BP |

| Cushing Connect (to Tulsa, OK) | 160,000 | Plains, Holly Energy Partners |

| Cushing to Broome/Ellis Lines | 131,000 | Plains, CVR |

| CushPo (to Ponca City, OK) | 130,000 | Phillips66 |

| Cushing South (to Houston area) | 120,000 | Energy Transfer |

| Borger Express | 90,000 | Navigator |

| Sunoco (to Tulsa) | 70,000 | Sunoco |

| Line O (to Borger, TX) | 38,000 | Phillips66 |

*Total Outbound Capacity: 3.3 Million barrels per day

Unlike Cushing, which packs all the terminals and connectivity into about 5,000 acres, the U.S. Gulf Coast network is geographically vast. As far as crude oil distribution is concerned, it stretches about 600 miles long, between Corpus Christi and New Orleans, with the greater Houston area roughly at the center. These three points all offer clusters of storage terminals and refining capacity, as do key points in between them: Port Arthur/Nederland, Texas; Lake Charles and St. James, Louisiana. The geographic dispersion means another network of pipelines connects many of these terminals with each other, and implies the need for price differences between the main locations that reflect shipment costs and fluctuate with regional supply/demand shifts. Within the Gulf Coast, values of the same grade of crude oil at different terminals can vary due to differences in connectivity and/or quality.

On the other hand, the physically concentrated nature of tankage within Cushing ensures that the price of a barrel at Cushing is consistent across the hub. The WTI futures contract allows for delivery through the Enterprise, Plains or Enbridge facilities in Cushing or at any facility with pipeline access to them. The terminals are key junction points in Cushing, capable of facilitating the transfer of tens of millions of barrels of crude oil every month. A commercial company that elects to take delivery after the expiration of the WTI futures contract must have storage and/or pipeline capacity connected to one of the NYMEX delivery locations in Cushing. From there, the firm can elect to take the oil into storage or into a pipeline with connectivity to PADD 2 refineries and to the Gulf Coast market.

The physical-delivery requirement of WTI futures provides a direct link to the underlying physical market, and futures also provide the security of a financially guaranteed clearinghouse for buyers and sellers. Further, Cushing terminal operators require firms to submit nominations for crude oil flows ahead of the delivery cycle in order to ensure the deliveries scheduled on and off exchange flow unencumbered.

Spot market conditions reflected in WTI prices

Companies have relied on the WTI futures contract to hedge their production or consumption of crude oil through major global events such as the Gulf War and the Great Financial Crisis. In just the last three years, unprecedented global market fundamentals have put intense stress on the oil industry as companies responded to volatile arbitrage price signals and hedged the price risk associated with COVID-19 in 2020, and Russia’s invasion of Ukraine and subsequent trade disruptions in 2022.

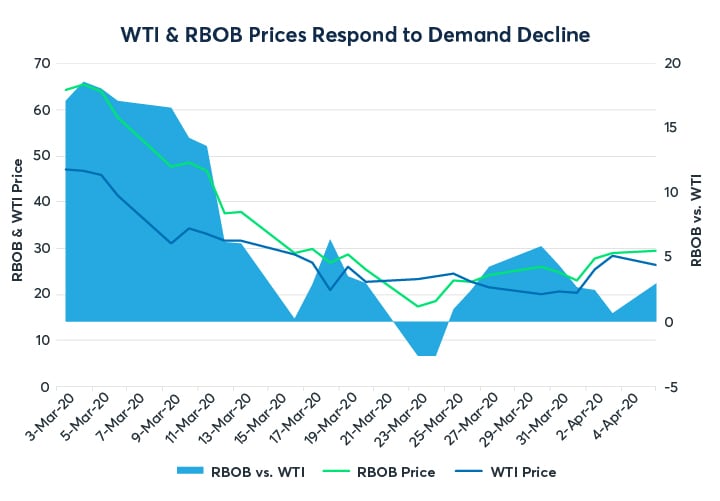

Energy demand destruction from COVID-19 first surfaced in early 2020 in the refined products markets, with international travel restrictions hampering jet fuel demand in January. This was followed by a sharp decline in New York Harbor RBOB gasoline futures contract (“RBOB futures”) when U.S. driving activity curtailed abruptly in March. The futures market for RBOB gasoline forecasted demand concerns early when prices traded at a 20-year low of $0.376 on March 23, 2020. As it became apparent that driving would be significantly curtailed, flat-price RBOB futures prices started to decline at a faster pace than crude oil prices.

https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/why-cushing-matters-a-look-at-the-wti-benchmark-chart2-720x500.jpg

Source: CME Group

{kind=link}

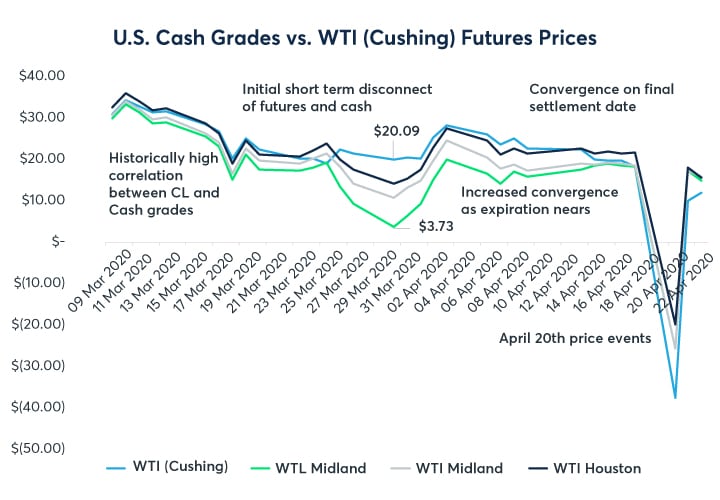

In response to the sharp drop in refined products prices vs. crude oil, the oil refining companies cut back on their processing of crude oil to match declines in product demand, leading to sharp declines in crude use, and increasing the utilization of U.S. crude oil storage. As the marginal barrel of supply to the global energy market, U.S. exports also fell.

Consistent with the decline in crude demand and increased call on storage, U.S. domestic crude oil cash markets also fell rapidly. By late March 2020, WTI Midland and WTI Houston were trading at widening discounts to the WTI futures benchmark, highlighting the imbalances in the U.S. crude oil market. This price arbitrage led market participants to direct barrels to flow into storage at Cushing. The chart below shows the general price volatility of the U.S. domestic crude oil grades during the March and April 2020 timeframe. Ultimately, WTI futures provided for convergence between the futures and cash markets at expiry on April 21, 2020, with a final settlement price of $10.01.

https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/why-cushing-matters-a-look-at-the-wti-benchmark-chart3-720x500.jpg

Source: CME Group

{kind=link}

It is not just the storage or pipeline capacity that make Cushing the critical hub as the delivery point for the global oil benchmark, but also the interconnectivity between a diverse mix of operators at Cushing.

{kind=link}

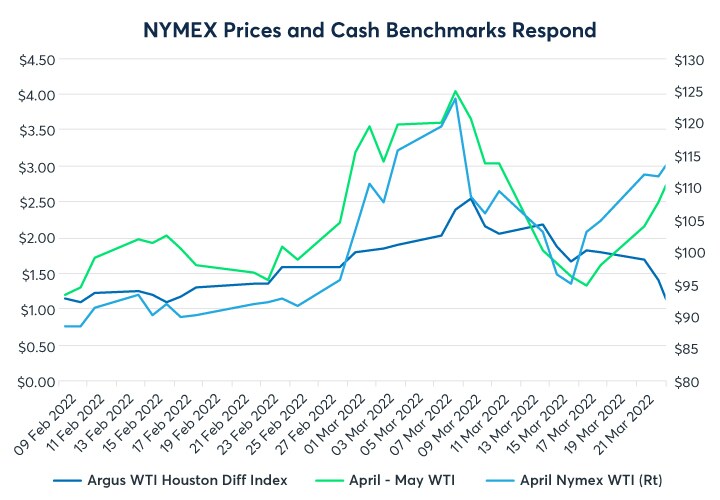

By 2022, global oil fundamentals had more than recovered from the COVID oversupply, with inventories of crude oil and refined products well below 5-year averages. The Russian invasion of Ukraine in late February triggered another disruption at a time when there was little supply buffer to absorb it: demand for non-Russian supplies of crude oil and diesel jumped sharply. Arbitrage signals pulled additional U.S. crude oil into the European market and sharply widening ULSD margins encouraged refiners to maximize their processing of crude oil, increasing demand further.

In early March, crude cash market prices rallied to post-COVID highs, with WTI Houston at $2.54. These premiums to NYMEX WTI indicated oil being pulled away from Cushing. NYMEX WTI for prompt April delivery settled at $123.70, and at a record premium to the next nearby contract of $4.05 per barrel on March 8. The strength in WTI prices helped to temporarily slow export demand; cash values and NYMEX spreads declined into expiration as international buyers looked elsewhere or delayed purchases.

https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/why-cushing-matters-a-look-at-the-wti-benchmark-chart4-v2-720x500.jpg

Source: CME Group

{kind=link}

Despite the emergency supplies that the International Energy Agency members added, crude oil markets remained under stress through the summer. High natural gas prices contributed to record incentives for diesel production, and refineries responded by maximizing their demand for crude oil. Crude and product flows readjusted in response, and in preparation for further trade restrictions in the winter.

Looking ahead

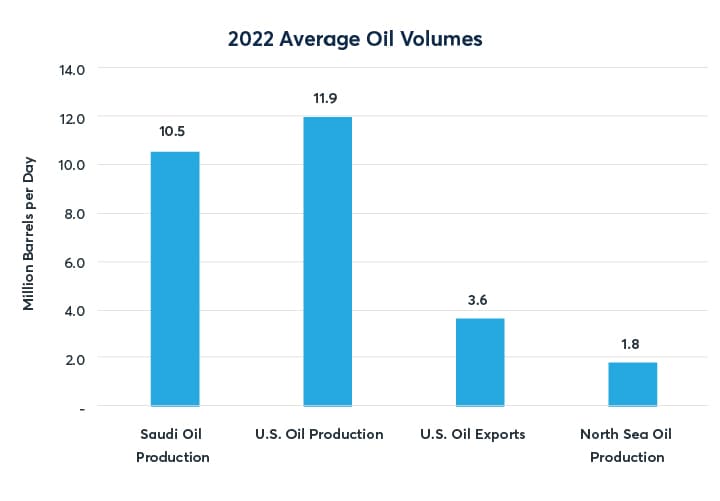

Global oil production growth expectations remain largely concentrated in the North American shale basins, ensuring that the Cushing hub will see even greater volumes of crude oil in the coming years. No change highlights the significance of the growth in U.S. oil volumes to the global market more clearly than the decision by Platts to reflect cargoes of WTI Midland in its North Sea Dated Brent crude oil benchmark beginning in June 2023. The extensive U.S. network of pipelines, terminals, and export capacity will continue to allow increasing volumes of exports at a time when light sweet North Sea production is seen in long-term decline.

{kind=link}

Launched 40 years ago, the CME Group WTI futures contract continues to work as designed, providing producers with the ability to avoid downside price risk, and consumers with upside price protection. Our futures prices reflect the fundamentals in the physical crude oil market, declining in price and increasing in contango when global supply outstrips demand, and rising in price and backwardation when global supply is tight. WTI futures perform its critical function as the central clearing mechanism for buyers and sellers in the crude oil market, and provide a transparent, fair, and robust benchmark price. The volatile world events impacting oil fundamentals in recent years demonstrate that the need for a reliable oil price benchmark has never been greater.