{kind=link}

Understanding SOFR Futures

The launch of Secured Overnight Financing Rate (SOFR) futures represented a significant and successful structural transformation in the global financial markets, completely redefining how short-term interest rate (STIR) risk is managed. SOFR futures and options now serve as the undisputed heavyweight of the global rates industry, providing market participants with unparalleled liquidity. At CME Group, the SOFR futures and options complex offers deeply liquid markets, which represent trillions of dollars in risk actively managed through these contracts.

This note reviews the SOFR benchmark, describes our Three-Month SOFR futures and One-Month SOFR futures, examines how both complement our established Interest Rate futures complex and discusses spread trading functionalities.

Secured Overnight Financing Rate

When SOFR was first published by the Federal Reserve Bank of New York (FRBNY) in April 2018, it was a brand-new alternative rate chosen to replace USD LIBOR. Today, roughly eight years later, it is arguably the most robust and heavily traded benchmark in the world, underpinned by more than $3 trillion in daily transaction volume. The sheer scale of trades, futures and investments linked to SOFR today is a direct result of how it is built: it is not based on estimates or expert judgment, but firmly rooted in massive, real-world overnight Treasury repo transactions.

The SOFR value for any U.S. government securities market business day (“business day”) is published by the Federal Reserve Bank of New York (FRBNY) around 8:00 a.m. New York time on the following business day.1 SOFR comprises a broad enough universe of overnight Treasury repo trade activity to make it a benchmark for all seasons, firmly rooted in transaction data from three diverse transaction sources.2

- Tri-party Treasury general collateral (GC) repo transactions cleared and settled by Bank of New York Mellon (BNYM), excluding repo transactions made through the Fixed Income Clearing Corporation (FICC) General Collateral Financing (GCF) repo market and excluding transactions in which the Federal Reserve is a counterparty.

- Tri-party Treasury GC repo transactions made through the FICC GCF repo market, for which FICC acts as central counterparty.

- Bilateral Treasury repo transactions cleared through the FICC Delivery-versus-Payment (DVP) service.

The FRBNY ranks the total aggregated volume of repo transactions from the lowest to highest rate and calculates the transaction-weighted median. This ensures the final benchmark is highly resilient to outliers and always represents an exact interest rate where real business was conducted, while adhering to the IOSCO Principles.3

The trade-volume-weighted median methodology brings at least three advantages: 1) It is a more robust statistic than alternatives such as, for example, the trade-volume-weighted arithmetic average; 2) The value it produces is almost always an interest rate level that has been observed, at which business most likely has been conducted; and 3) It aligns with the calculation methodology for the daily effective federal funds rate (EFFR) and for the daily overnight bank funding rate (OBFR), which was adopted by the Federal Reserve in March 2016.4

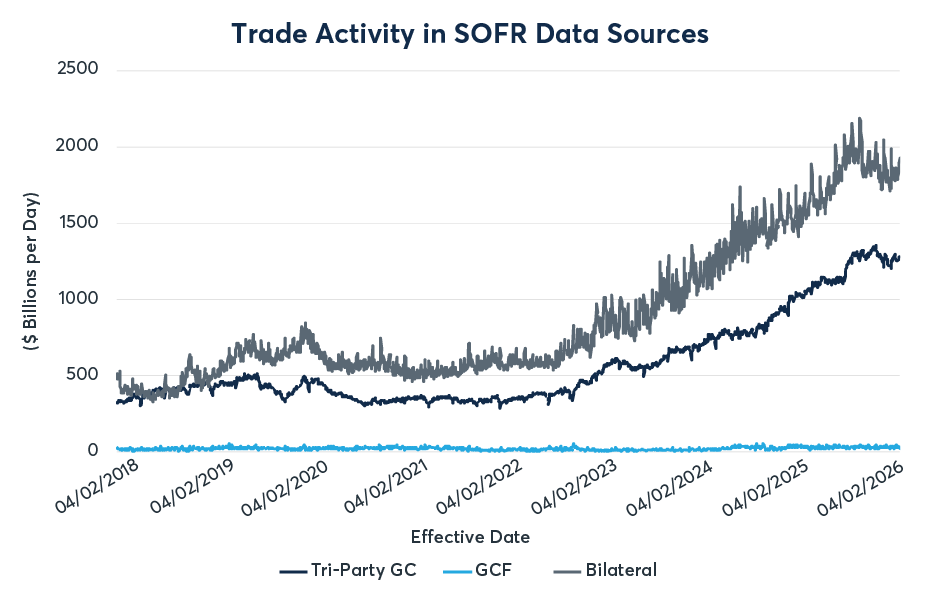

SOFR’s underlying transaction pool is massive. From January 2, 2026, to June 1, 2026, the average daily trading volumes ran $1.28 trillion in BNYM tri-party Treasury GC repo, $31 billion in FICC GCF Treasury repo, and $1.855 trillion in FICC DVP bilateral Treasury repo, making the total average traffic flow $3.166 trillion per day (Exhibit 1).

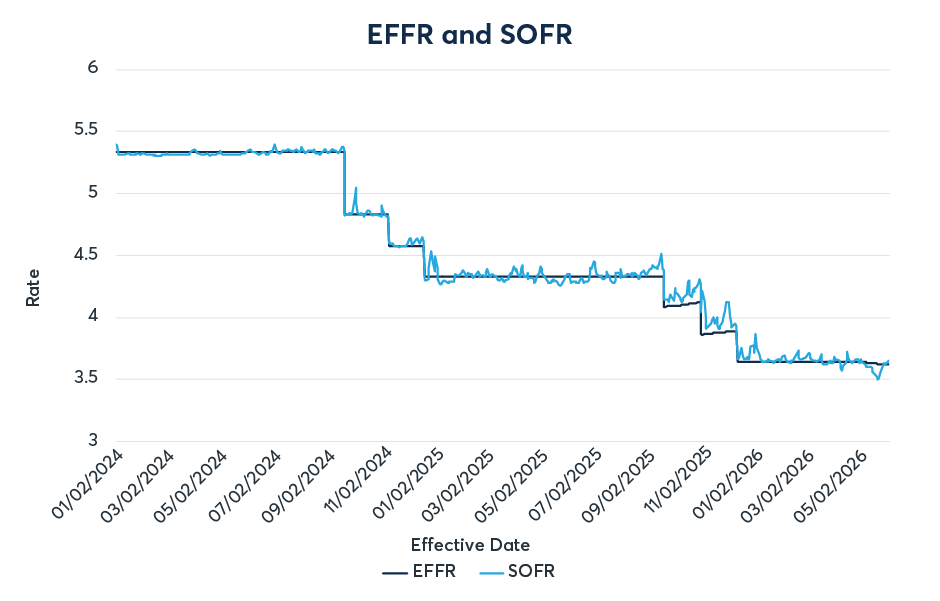

Although SOFR and EFFR follow similar trends (Exhibit 2), they diverge in their short-term behavior, with SOFR exhibiting more pronounced volatility. Between January 2024 and June 2026, the median absolute daily change in SOFR was one basis point while, in EFFR, it was zero. In other words, SOFR often fluctuates by only a handful of basis points (bps) each day, while EFFR is much more stable in the periods between FOMC meetings.

Following consultation beginning in July 2024, the FRBNY made two modifications to the calculation methodology, both regarding the centrally cleared DVP segment of the repo market. The first modification removed transactions between affiliated institutions while the second modification removed a consistent 20% of lowest-rate transaction volume (specials), thus eliminating the day-to-day variability in the share of DVP that is removed.

Changes were implemented as of November 25, 2024, based on transaction data of November 22, 2024.5

Exhibit 1 -- Trade activity ($ billions per day) in SOFR data sources, April 2, 2018 through June 1, 2026

{kind=link}

Source: FRBNY

Exhibit 2 -- Daily EFFR and SOFR values (basis points per annum), Jan 2, 2024 through June 1, 2026

{kind=link}

Source: FRBNY

Three-Month SOFR Futures

Exhibit 3 summarizes contract specifications for Three-Month SOFR (SR3) futures.

Exhibit 3 -- CME Three-Month SOFR Futures Contract Specifications

| Trading unit |

Compounded daily SOFR interest during contract reference quarter, such that each basis point per annum of interest = $25 per contract. Reference quarter: For a given contract, interval from (and including) third Wed of third month preceding delivery month, to (and not including) third Wed of delivery month. |

| Price basis |

Contract-grade IMM Index = 100 minus R. Example: Contract price of 96.1550 IMM index points signifies R = 3.845 percent per annum. R = business-day compounded Secured Overnight Financing Rate (SOFR) per annum during contract reference quarter Reference quarter: For a given contract, interval from (and including) third Wed of third month preceding delivery month, to (and not including) third Wed of delivery month. |

| Contract size | $25 per basis point per annum (or $2,500 per contract-grade IMM index point) |

| Minimum price increment (MPI) |

Contracts with four months or less until termination of trading: 0.0025 IMM Index points (¼ basis point per annum) equal to $6.25 per contract All other contracts: 0.005 IMM index points (½ basis point per annum) equal to $12.50 per contract |

| Termination of trading | Trading terminates on the business day prior to the third Wednesday of contract delivery month. |

| Delivery |

By cash settlement, by reference to final settlement price, on the third Wed of delivery month (first U.S. government securities market business day following last day of trading). Final settlement price: Contract-grade IMM Index (100 minus R) evaluated on the basis of realized SOFR values during contract reference quarter: R = [ Πi {1+(di /360)*(ri /100)} – 1 ] x (360/D) x 100 n = Number of U.S. government securities market business days in the reference quarter i ~ Running variable indexing U.S. government securities market business days during reference quarter Πi=1…n denotes the product of values indexed by the running variable, i = 1,2,…,n. ri = SOFR value for ith U.S. government securities market business day di = Number of calendar days to which ri applies D = Σi di (i.e., number of calendar days in reference quarter) |

| Delivery months |

Nearest 39 quarterly months (Mar, Jun, Sep, Dec) and the nearest six serial months. For each contract, contract month is the month in which the reference quarter begins. Example: For a “Sep” contract, reference quarter starts on IMM Wed of Sep and ends with termination of trading on the first U.S. government securities market business day before IMM Wed of Dec, the contract delivery month. |

| Trading venues and hours |

Globex pre-open: Sunday 4:00 p.m. – 5:00 p.m. Central Time (CT) Monday – Thursday 4:45 p.m. – 5:00 p.m. (CT) Globex: Sunday 5:00 p.m. - Friday - 4:00 p.m. CT with a daily maintenance period from 4:00 p.m. - 5:00 p.m. CT ClearPort: Sunday 5:00 p.m. - Friday 5:45 p.m. CT with no reporting Monday - Thursday from 5:45 p.m. - 6:00 p.m. CT |

| Globex algorithm | Allocation (A Algorithm, with Top Order Allocation = 100% and Pro Rata Allocation = 100%) |

| Block trade minimum size |

Asian trading hours 500 contracts European trading hours 1,000 Regular trading hours 2,000 / 4,000* / 8,000* *Block trades above a certain threshold submitted during RTH may be granted an expanded reporting window of 15 minutes provided that: The block threshold for trades on contract expiration months up to and including two years two months (26 months) is 8,000 contracts. The block threshold for trades on contract expiration months beyond two years two months (26 months) is 4,000 contracts. |

| Block reporting window |

Asian trading hours 15 mins European trading hours 15 Regular trading hours 5 / 15* |

| Product codes |

CME: SR3 Bloomberg: SFR Cmdty <GO> |

Contract names, codes and critical dates

Three-Month SOFR (SR3) futures are financially settled based on daily SOFR benchmark rates that are compounded in-arrears over each contract’s three-month reference period. We expand on that calculation in the next section below. As a result of compounding in-arrears the final settlement price of each expiry is not known until the end of the reference period.

Contract names are based on the month in which the reference period begins, rather than when the contract expires some three months later. For example, the September 2026 SR3 futures contract (SR3U6) references the compounded overnight SOFR rates beginning on the third Wednesday of September 2026, and ends on, but not including, the third Wednesday of December 2026. Contract codes reflect the contract names in the usual way whereby the contract named month determines the letter code in the IMM convention (Mar - H, Jun - M, Sep - U, Dec - Z etc.).

For those familiar with the now retired Eurodollar futures, it is worth noting that these contract month naming conventions are aligned in that the forward looking reference period of Eurodollars matches the backward looking reference period for SOFR, the major difference being that for SOFR contracts the final settlement date is at the end of such period.

{kind=link}

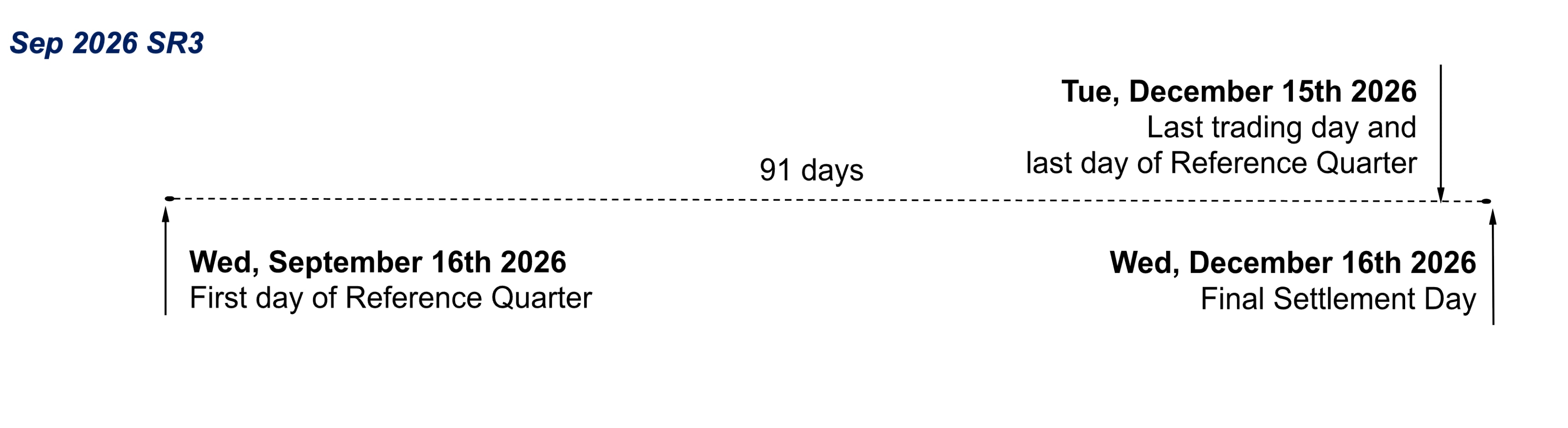

Last trading day

The last day of trading in an expiring SR3 contract is the first business day before the third Wednesday of the contract delivery month (i.e., the business day first preceding the last day of the contract reference quarter). Example: For the September 2026 SR3 contract, the scheduled last day of trading is Tuesday, December 15, 2026, as depicted above.

Final settlement price

The final settlement price is 100 contract price points minus the daily compounded SOFR interest during the contract reference quarter, rounded to the nearest 1/100 of one basis point per annum. The derivatives marketplace computes an expiring contract’s final settlement price on the morning of the third Wednesday of the contract delivery month, after FRBNY has published the SOFR value based on trade activity for the final day of the contract’s reference quarter (typically the preceding Tuesday, more generally the first preceding business day).

Example: Consider the December 2025 SR3 contract. The contract reference quarter spans 91 days, from (and including) Wednesday, December 17 (the third Wednesday of December), until (and not including) Wednesday, March 18 (the third Wednesday of March). Exhibit 4 details the contract final settlement price calculation on Wednesday, March 18, when FRBNY would have published the SOFR value for Tuesday, March 17.

Exhibit 4 -- Daily compounding of SOFR values for December 2025 SR3 futures

(Highlighted dates = business days immediately preceding U.S. government securities market holidays)

| Date | Days | SOFR | Daily interest accumulation factor | Cumulative factor |

| 12/17/2025 | 1 | 3.69 | 1.0001025 | 1.0001025 |

| 12/18/2025 | 1 | 3.66 | 1.000101667 | 1.000204177 |

| 12/19/2025 | 3 | 3.66 | 1.000305 | 1.000509239 |

| 12/22/2025 | 1 | 3.68 | 1.000102222 | 1.000611514 |

| 12/23/2025 | 1 | 3.66 | 1.000101667 | 1.000713242 |

| 12/24/2025 | 2 | 3.66 | 1.000203333 | 1.000916721 |

| 12/26/2025 | 3 | 3.76 | 1.000313333 | 1.001230341 |

| 12/29/2025 | 1 | 3.77 | 1.000104722 | 1.001335192 |

| 12/30/2025 | 1 | 3.71 | 1.000103056 | 1.001438386 |

| 12/31/2025 | 2 | 3.87 | 1.000215 | 1.001653695 |

| 01/02/2026 | 3 | 3.75 | 1.0003125 | 1.001966712 |

| 01/05/2026 | 1 | 3.7 | 1.000102778 | 1.002069692 |

| 01/06/2026 | 1 | 3.66 | 1.000101667 | 1.002171569 |

| 01/07/2026 | 1 | 3.65 | 1.000101389 | 1.002273178 |

| 01/08/2026 | 1 | 3.64 | 1.000101111 | 1.002374519 |

| 01/09/2026 | 3 | 3.64 | 1.000303333 | 1.002678572 |

| 01/12/2026 | 1 | 3.64 | 1.000101111 | 1.002779954 |

| 01/13/2026 | 1 | 3.65 | 1.000101389 | 1.002881625 |

| 01/14/2026 | 1 | 3.64 | 1.000101111 | 1.002983027 |

| 01/15/2026 | 1 | 3.66 | 1.000101667 | 1.003084997 |

| 01/16/2026 | 4 | 3.65 | 1.000405556 | 1.003491804 |

| 01/20/2026 | 1 | 3.64 | 1.000101111 | 1.003593268 |

| 01/21/2026 | 1 | 3.63 | 1.000100833 | 1.003694464 |

| 01/22/2026 | 1 | 3.64 | 1.000101111 | 1.003795949 |

| 01/23/2026 | 3 | 3.65 | 1.000304167 | 1.00410127 |

| 01/26/2026 | 1 | 3.66 | 1.000101667 | 1.004203353 |

| 01/27/2026 | 1 | 3.66 | 1.000101667 | 1.004305447 |

| 01/28/2026 | 1 | 3.64 | 1.000101111 | 1.004406994 |

| 01/29/2026 | 1 | 3.65 | 1.000101389 | 1.00450883 |

| 01/30/2026 | 3 | 3.68 | 1.000306667 | 1.004816879 |

| 02/02/2026 | 1 | 3.69 | 1.0001025 | 1.004919873 |

| 02/03/2026 | 1 | 3.69 | 1.0001025 | 1.005022877 |

| 02/04/2026 | 1 | 3.65 | 1.000101389 | 1.005124775 |

| 02/05/2026 | 1 | 3.65 | 1.000101389 | 1.005226684 |

| 02/06/2026 | 3 | 3.64 | 1.000303333 | 1.005531602 |

| 02/09/2026 | 1 | 3.63 | 1.000100833 | 1.005632994 |

| 02/10/2026 | 1 | 3.65 | 1.000101389 | 1.005734954 |

| 02/11/2026 | 1 | 3.65 | 1.000101389 | 1.005836924 |

| 02/12/2026 | 1 | 3.65 | 1.000101389 | 1.005938905 |

| 02/13/2026 | 4 | 3.66 | 1.000406667 | 1.006347986 |

| 02/17/2026 | 1 | 3.71 | 1.000103056 | 1.006451696 |

| 02/18/2026 | 1 | 3.73 | 1.000103611 | 1.006555976 |

| 02/19/2026 | 1 | 3.67 | 1.000101944 | 1.006658589 |

| 02/20/2026 | 3 | 3.66 | 1.000305 | 1.006965619 |

| 02/23/2026 | 1 | 3.66 | 1.000101667 | 1.007067994 |

| 02/24/2026 | 1 | 3.67 | 1.000101944 | 1.007170659 |

| 02/25/2026 | 1 | 3.67 | 1.000101944 | 1.007273335 |

| 02/26/2026 | 1 | 3.67 | 1.000101944 | 1.007376021 |

| 02/27/2026 | 3 | 3.68 | 1.000306667 | 1.007684949 |

| 03/02/2026 | 1 | 3.71 | 1.000103056 | 1.007788797 |

| 03/03/2026 | 1 | 3.7 | 1.000102778 | 1.007892375 |

| 03/04/2026 | 1 | 3.67 | 1.000101944 | 1.007995124 |

| 03/05/2026 | 1 | 3.66 | 1.000101667 | 1.008097604 |

| 03/06/2026 | 3 | 3.65 | 1.000304167 | 1.008404233 |

| 03/09/2026 | 1 | 3.65 | 1.000101389 | 1.008506474 |

| 03/10/2026 | 1 | 3.64 | 1.000101111 | 1.008608445 |

| 03/11/2026 | 1 | 3.64 | 1.000101111 | 1.008710427 |

| 03/12/2026 | 1 | 3.65 | 1.000101389 | 1.008812699 |

| 03/13/2026 | 3 | 3.65 | 1.000304167 | 1.009119546 |

| 03/16/2026 | 1 | 3.7 | 1.000102778 | 1.009223261 |

| 03/17/2026 | 1 | 3.65 | 1.000101389 | 1.009325585 |

Data source: FRBNY

Date = the starting date for the overnight period, the end date is represented by the subsequent date in the table which is the next good business day

“Days” = # actual days between the start and end date of each overnight period

Daily Interest Accumulation Factor = 1 + (Days/360) x (SOFR/100)

Example Daily Interest Accumulation Factor on:

Fri, Feb 27th 2026 = 1 + (3/360) x (3.68/100) = 1.000306667

Cumulative Factor = Product of Daily Interest Accumulation Factor and the running Cumulative Factor

Final Settlement Rate:

[Cumulative Factor on the last day of the period less 1] x (360 / total # days in IMM period (usually 91)) x 100

Example: [ 1.009325585 - 1 ] x (360/91) x 100 = 3.68924253 pct/yr

Round to the nearest 1/100th bp: 3.6892

Final Settlement Price: 100 - 3.6892 = 96.3108

As Exhibit 4 suggests, the computational conventions for compounding of daily SOFR values closely resemble those that apply in standard U.S. dollar overnight index swaps (OIS), in which each OIS contract’s floating rate leg is based on business-day-compounded rates. That is, SOFR will accrue as simple interest over weekends and U.S. government securities market holidays and as compound interest otherwise.7

Futures final settlement prices and SOFR revisions

FRBNY normally publishes the SOFR value based on the prior day’s transaction data each morning, at around 8:00 a.m. New York time. If the FRBNY discovers errors in the underlying data intraday (as provided to it by either BNYM or DTCC Solutions), it may publish a revised SOFR value at approximately 2:30 p.m. New York time. This is subject to two restrictions: (1) FRBNY will issue a revised SOFR value only on the same day as the initial rate value was published, and no later, and (2) it will issue a revised SOFR value only if the size of the revision exceeds one basis point per annum. Any time a SOFR value is revised, FRBNY will include a footnote to identify the revision, however these revisions have been exceedingly rare historically.8

FRBNY’s revision policy interacts with SR3 futures final settlement prices in two ways. First, for all but the last business day in an expiring contract’s reference quarter, the contract final settlement price calculation will incorporate any revised values that FRBNY has issued. Second, for the last business day of the expiring contract’s reference quarter, the SOFR value that enters into calculation of the final settlement price shall be the value first published by FRBNY, irrespective of any revised SOFR value that FRBNY might publish at 2:30 p.m. that day.

Price = 100 minus rate

The SR3 contract price takes the familiar IMM index form, derived by subtracting from 100 the value (either expected or actual) of the contract’s three-month SOFR interest exposure, as described above.

Example: Suppose it is early August. Consider the nearby September SR3 contract, which comes to final settlement in December. If the consensus view among market participants is that daily SOFR interest will compound between mid-September and mid-December (i.e., during the contract reference quarter) at an annualized rate of 3.5%, then the futures contract price should trade at or around 96.50 (equal to 100.00 minus 3.50).

If any newly arrived information or change in market circumstances prompts market participants to revise their expectations for SOFR by the time of the contract reference quarter, then the contract price will move to reflect these new expectations.

1 basis point = $25

Gains or losses on a contract position are calculated simply by determining the number of interest rate basis points (bps) by which the contract price has moved, then multiplying by the value of one bp per contract. Each basis point of contract interest is worth $25. Thus, a helpful heuristic for the SR3 contract size is $2,500 x the contract IMM Index.

Minimum price increment = Either ¼ bp or ½ bp

The price of a SR3 contract trades in increments of either ¼ bp or ½ bp, depending on the contract’s proximity to its final settlement date. For contracts with four months or less until the last day of trading, the minimum price fluctuation is ¼ bp (equal to $6.25 per contract). For all other contracts, the minimum price fluctuation is ½ bp (equal to $12.50 per contract). SOFR packs and bundles are an exception, in that they are subject to a minimum price increment of ¼ bp uniformly for all expiries.

Example: Consider the September 2026 SR3 contract. Its reference quarter starts on (and includes) Wednesday, September 16, 2026, and ends on (and excludes) Wednesday, December 16, 2026. Its minimum price increment is ½ bp through close of trading on Friday, August 14, 2026. When trading resumes on Sunday, August 16, 2026, for trade date Monday, August 17, its minimum price increment is ¼ bp.

Contract listings = Approximately 10 years of expiries

SR3 listings are comprised of quarterly and serial expiries. There are four listed quarterly IMM expiries (March, June, September, December) every year. Each year along the curve is by convention referred to in terms of “colors” - the nearby four forward-starting quarterly expiries comprise the “white” year, followed by the “red,” “green,” “blue,” “gold” years and beyond. In total there are 39 quarterly expiries listed that span 10 years, which are complemented by an additional six serial contracts that are listed for months between the quarterly expiries in the nearby year.

One-Month SOFR futures

Exhibit 5 -- One-Month SOFR futures contract specifications

| Trading unit | Average daily SOFR interest during futures contract delivery month, such that each basis point per annum of interest is worth $41.67 per futures contract. |

| Price basis |

Contract-grade IMM Index = 100 minus R. R = arithmetic average of SOFR during contract delivery month. Example: Contract price of 96.3875 IMM index points signifies R = 3.6125 percent per annum. |

| Contract size | $41.67 per basis point per annum (or $4,167 per contract-grade IMM index point) |

| Minimum price increment (MPI) |

0.005 IMM index points (½ basis point per annum) equal to $20.835 per contract, provided that:

|

| Termination of trading | Trading terminates on the last business day of the contract month. |

| Delivery | By cash settlement, by reference to final settlement price, on the first U.S. government securities market business day following the last day of trading. Final settlement price: Contract-grade IMM index evaluated at R = arithmetic average of daily SOFR during delivery month. |

| Delivery months | Nearest 25 calendar months. |

| Trading venues and hours |

Globex pre-open: Sunday 4:00 p.m. – 5:00 p.m. Central Time (CT) Monday – Thursday 4:45 p.m. – 5:00 p.m. (CT) Globex: Sunday 5:00 p.m. - Friday - 4:00 p.m. CT with a daily maintenance period from 4:00 p.m. - 5:00 p.m. CT ClearPort: Sunday 5:00 p.m. - Friday 5:45 p.m. CT with no reporting Monday - Thursday from 5:45 p.m. - 6:00 p.m. CT |

| Globex algorithm | Split FIFO and Pro-Rata (K Algorithm, with Top Order Allocation = 100% and Pro Rata Allocation = 100%) |

| Block trade minimum size |

Asian trading hours 125 contracts European trading hours 250 Regular trading hours 500 |

| Block reporting window |

Asian trading hours 15 mins European trading hours 15 Regular trading hours 5 |

| Product Codes |

CME: SR1 Bloomberg: SER Comdty <GO> |

Last trading day

The last day of trading in an expiring SR1 contract is the last business day of the contract delivery month. Example: For November 2026 SR1 futures, the scheduled last day of trading is Monday, November 30.

Final settlement price

The final settlement price is 100 contract price points minus the arithmetic average of daily SOFR interest during the contract delivery month, with the average value rounded to the nearest 1/10 of one bp per annum. Normally, the derivatives marketplace will compute an expiring contract’s final settlement price on the morning of the first business day following the end of the expiring contract’s delivery month. Example: For November 2026 SR1 futures, the delivery month ends on (and includes) Monday, November 30, 2026, and determination of the final settlement price is scheduled to occur on Tuesday, December 1, 2026, after FRBNY has published the SOFR value based on trade activity for Monday, November 30, 2026.

Similar to SR3 futures, determination of the final settlement price for an expiring SR1 futures will incorporate any revised values that FRBNY publishes for all but the last business day in the contract delivery month.

Price = 100 minus rate

The SR1 futures contract price is quoted in IMM Index form, equal to 100 price points minus the expected value of average daily SOFR interest during the contract delivery month.

Example: If market participants generally expect the average level of daily SOFR to be 3.718% during the month of October, then the price of October SR1 futures should trade in the neighborhood of 96.280 or 96.285 (i.e., around 96.282, equal to 100.000 minus 3.718). If the October SR1 futures contract is eligible to trade in ¼ bp minimum price increments, then the price more likely would trade at or around 96.2800 or 96.2825 (as before, either side of 96.282).

1 basis point = $41.67

Gains or losses on a contract position are calculated simply by determining the number of bps by which the contract price has moved, then multiplying by the value of one bp. Each bp of contract interest is worth $41.67. Thus, a helpful heuristic for the SR1 contract size is $4,167 x the contract IMM index.

Price increments = Either ¼ bp or ½ bp

The SR1 contract price trades in increments of either ¼ bp or ½ bp, depending on the proximity of the contract final settlement date. The minimum price increment is ½ bp, worth $20.835 per contract, up to the start of the first day of the delivery month. From the first day of the delivery month until termination of trading, the contract minimum price increment is ¼ bp, worth $10.4175 per contract.

Additionally, in cases where the first day of the delivery month is a Tuesday, Wednesday, Thursday or Friday, the contract minimum price increment reduces to ¼ bp at the start of Globex trading on the Sunday preceding the first day of the delivery month.

Examples: For June 2026 SR1 futures, the first day of the delivery month is Monday, June 1. Thus, the minimum price increment is ½ bp until the start of Globex trading on Sunday, May 31 (i.e., for trade date Monday, June 1). From then until termination of trading in the contract, the minimum price increment is ¼ bp.

For July 2026 SR1 futures, by contrast, the first day of the delivery month is Wednesday, July 1. In this case, the minimum price increment is ½ bp until the start of Globex trading on Sunday, June 28. From that point – the start of the Monday, June 29 trade date – until trading terminates in the contract on Friday, July 31, the minimum price increment is ¼ bp.

Contract listings = Nearest 25 calendar months

At any given time, the derivatives marketplace lists 25 contracts for trading, one for each of the nearest calendar months. By implication, a newly listed SR1 futures contract trades for 25 months until it goes to final settlement.

Complementarity between SR1 and SR3

Prior to the start of the contract’s reference quarter, the SR3 futures contract rate – the “rate” portion of the “100 minus rate” contract price – gauges market expectation of business-day-compounded SOFR during the reference quarter, expressed as an interest rate per annum. After the nearby contract enters its reference quarter, the contract rate becomes a mix of (i) known SOFR values (i.e., published values for all days from start of the reference quarter to the present) and (ii) market expectations of SOFR values for all remaining days in the reference quarter that lie ahead.

As the expiring contract progresses through its reference quarter, the forward-looking expectational component of its price plays a diminishing role in fair valuation. In general, progressively decreasing uncertainty about the contract’s final settlement price means steadily diminishing contract price volatility.

Market practitioners familiar with 30-Day Federal Funds futures will recognize this dynamic immediately. As an expiring Fed Funds contract makes its way through its delivery month, contract users know increasingly more of the daily EFFR values that will determine the contract’s final settlement price. Room for price volatility in the contract shrinks accordingly.

Seen in this light, the SR1 futures strip makes a useful complement to SR3 futures for market participants who seek finer granularity in framing expectations of SOFR values, or who seek finer resolution of SOFR volatility.

Spread trading with SOFR futures

For SR3 futures, Globex enables trading of standardized intramarket calendar spreads and combinations, including butterflies, condors and other such structures. Likewise for SR1 futures, Globex intramarket calendar spreads and strategies are enabled, similar to those available for Fed Fund futures.

In addition, a diverse array of Globex intermarket spreads are also available among SR1 and SR3 futures, connecting these markets with Fed Funds futures, ESTR futures and others.9

Exhibit 6 – Selection of futures intermarket spreads: SOFR, 30-Day Federal Funds (ZQ), ESTR, and 13-Week T-Bill (TBF3)

| Globex symbol example | Front leg | Back leg | Leg ratio (# contracts) | Minimum price increment (fraction of 1 bp) | Implied pricing (Y/N) | # Spread months listed | |

| SR1:ZQ |

July 2026: SR1N6-ZQN6 |

SR1 | ZQ | 1:1 | 0.25 | Y | 25 |

| ESR:SR3 |

June 2026 ESRM6-SR3M6 |

ESR | SR3 | 1:1 | 0.125 | Y | 1 |

| 0.25 | 16 | ||||||

| SR3:TBF3 |

June 2026 SR3M6-TBF3M6 |

SR3 | TBF3 | 1:1 | 0.25 | Y | 1 |

| 0.50 | 5 |

In addition to the above listed spreads, we also offer other combinations which are not 1:1 spreads but, rather, account for the different sizes of each contract. Notable examples include the SR1:SR3 spread (One-Month against Three-Month SOFR futures) and the SR3:ZQ spread (Three-Month SOFR against 30-Day Federal Funds futures).

Intercommodity spread basics

The SR1:ZQ spread comprises purchase (sale) of one One-Month SOFR futures contract and sale (purchase) of one 30-Day Federal Funds futures contract. Each leg is weighted at $41.67 per bp in the corresponding underlying interest rate.

Similarly, the (i) SR3:ESR and (ii) SR3:TBF3 spreads consists of the purchase (sale) of one Three-Month SOFR futures and the sale (purchase) of (i) one Three-Month ESTR futures or (ii) one 13-week Treasury Bill futures, with each leg weighted at $25 per bp in the respective underlying interest rate.

Implied pricing functionality links the liquidity between the Globex orderbook for these spreads and the orderbooks for their component contracts.

One-Month SOFR (SR1) futures vs. 30-Day Federal Funds (ZQ) futures spreads quarter tick eligible

For the Globex SR1:ZQ spread, the price display convention is “SR1 price minus ZQ price.” When SOFR values underlying the SR1 contract are lower than the EFFR values underlying the ZQ contract, the price of SR1 contracts would be expected to be higher than the price of the ZQ contract and one can expect SR1:ZQ spread prices to be positive. Example: For a hypothetical SR1 contract final settlement price of 96.3925 and a hypothetical ZQ final settlement price of 96.375, the spread price would be 96.3925 minus 96.375 = 0.0175 price points = 1.75bps.

On June 15, 2026, CME Group adjusted the minimum price increment (MPI) for the spread between SR1 and ZQ making it ¼ tick (bp) eligible, where previously it had been at a ½ basis point. This change allows traders to express more granular views on the magnitude of the SOFR-EFFR basis and meaningfully reduces the cost of execution in this market. Moreover, this change reflects the lower volatility structure of the spread between these highly correlated rates, in contrast to the outright markets for each leg which remain at ½ tick minimum increments.10

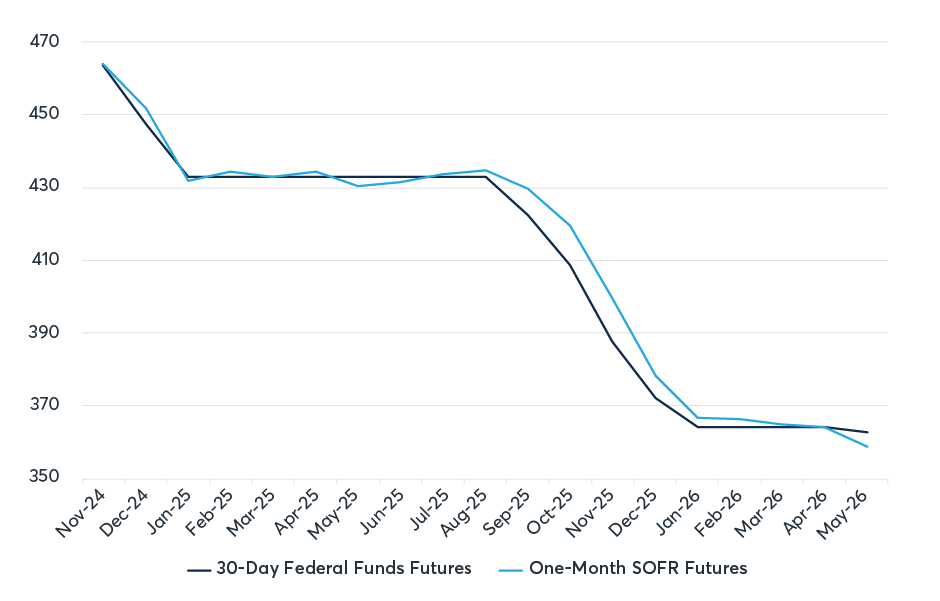

The lines in Exhibit 7 trace the implied contract rates, based on final settlement prices, for each of the months between November 2024 and May 2026, inclusive. As one can observe, while both rates are very correlated, they exhibit a slight and variable basis between each other.

Exhibit 7 -- Contract interest rates at futures final settlement (basis points per year): Fed Funds and SR1, November 2024 through May 2026

{kind=link}

Source: CME Group

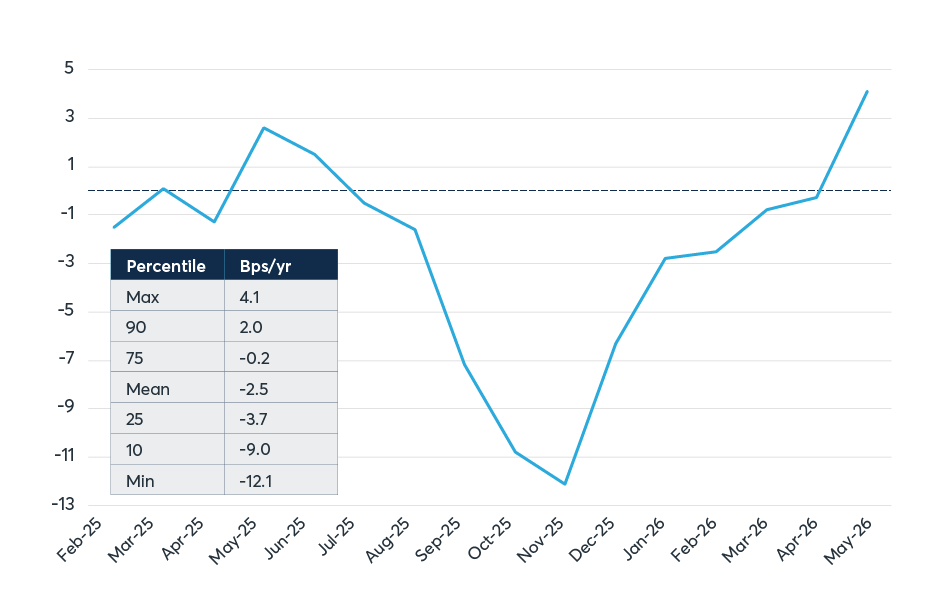

Although month-averaging smoothes much of SOFR’s comparatively higher day-to-day volatility, some residual effect persists. In Exhibit 7, the average absolute change from one-month-average level to the next is approximately six bps for EFFR and 7.5 bps for SOFR. This difference is even more pronounced outside of rate hiking and cutting cycles. During the relatively quiet period between February 2025 and August 2025, average monthly EFFR figures did not change at all, while SOFR’s absolute monthly change averaged around two bps.

Exhibit 8 highlights two other comparative features that warrant mention, including:

- Over the period presented, monthly SOFR levels ran an average of 2.6 bps above monthly EFFR.

- This period was also interesting in that it displayed both months where SOFR was above EFFR and months where the reverse was true. This evidences the fact that developments in USD funding markets can have significant impacts on the basis between both rates.

Exhibit 8 -- Contract interest rate spreads at futures final settlement (basis points per annum): Average monthly EFFR rate minus average monthly SOFR rate, February 2025 through May 2026

{kind=link}

Source: CME Group

Product codes

| One-Month SOFR futures | Three-Month SOFR futures | One-Month SOFR futures vs. 30-Day Federal Funds futures | |

| Globex | SR1 | SR3 | SR1-ZQ |

| Bloomberg | SER <Comdty> | SFR <Comdty> | SERFF <Comdty> |

| CQG | SR1 | SR3 | SZI0 |

| DTN, Inc | @SR1 | @SR3 | @SR1/@FF |

| Fidessa (ION) | SR1 | SR3 | SR1 |

| FIS Global | SR1 | SR3 | SR1 |

| ION Group | SR1 | SR3 | SR1 |

| Itiviti | SR1 | SR3 | SR1 |

| Refinitiv | 0#S1R: | 0#SRA: | S1R-FF |

| Trading Technologies | SR1 | SR3 | SR1 |

| Vela Trading Systems | SR1 | SR3 | SR1 |

Appendix -- Technical details of SOFR intercommodity spreads on Globex

| Product | MDP 3.0: tag 6937-Asset | iLink: tag 55 Symbol MDP 3.0 tag 1151 – Security Group | Future Tag 762 Security SubType | MDP 3.0 Market Data Channel |

|

One-Month SOFR Inter-Exchange Spread vs. 30-Day Fed Funds futures |

SR1 | SY | IS | 312 |

|

One-Month SOFR futures vs. Three-Month SOFR futures Reduced Tick Inter-Commodity Ratio Spread |

SR1 | SS | EF | 312 |

|

30-Day Fed Funds futures vs. Three-Month SOFR futures Reduced Tick Inter-Exchange Ratio Spread |

ZQ | SY | EF | 348 |

Contact Us

For more information about SOFR and SOFR futures, please visit www.cmegroup.com/sofr or contact…

Mark Rogerson | +44 7590 950 256 | mark.rogerson@cmegroup.com

Jonathan Kronstein | +1 312 213 9657 | jonathan.kronstein@cmegroup.com

Arthur Dimitrov Lobao | +1 773 382 6806 | arthur.lobao@cmegroup.com

Brendan Lee | +1 646 709 5934 | brendan.lee@cmegroup.com

1. For data and more information about SOFR and other FRBNY reference rates, visit Reference Rates, at: https://www.newyorkfed.org/markets/reference-rates and see Statement Regarding the Initial Publication of Treasury Repo Reference Rates, Statements and Operating Policies, 28 February 2018, which is available at: https://www.newyorkfed.org/markets/opolicy/operating_policy_180228

2. See Additional Information about Reference Rates Administered by the New York Fed, April 6th 2026, which includes a detailed overview of the Treasury repo market, and which is available at: https://www.newyorkfed.org/markets/reference-rates/additional-information-about-reference-rates.

3. See Frost, Joshua, Presentation at the Alternative Reference Rates Committee Roundtable, FRBNY, New York, 8 November 2017, which is available at: https://www.newyorkfed.org/newsevents/speeches/2017/fro171108; and Lorie K Logan, The Role of the New York Fed as Administrator and Producer of Reference Rates, Remarks at the Annual Primary Dealer Meeting, FRBNY, New York, January 9, 2018, which is available at: https://www.newyorkfed.org/newsevents/speeches/2018/log180109

4. See FRBNY, Statement Regarding the Calculation Methodology for the Effective Federal Funds Rate and Overnight Bank Funding Rate, Operating Policy Statement, 8 July 2015, which is available at: https://www.newyorkfed.org/markets/opolicy/operating_policy_150708

5. Statement Regarding Modification to the SOFR Methodology: https://www.newyorkfed.org/markets/opolicy/operating_policy_241023

6. Or on the next following business day, if the third Wednesday happens to be a U.S. government securities market holiday.

7. EFFR and SOFR are subject to slightly different holiday schedules – EFFR relies on the Federal Reserve's calendar, while SOFR follows SIFMA's government securities calendar. This divergence becomes most apparent around holidays such as Good Friday.

For EFFR, FRBNY produces a value for every weekday, excluding days on which the Fedwire Funds Service is closed (https://www.federalreserve.gov/paymentsystems/fedfunds_about.htm). As a rule, such excluded days also are identified as banking holidays by FRBNY (https://www.newyorkfed.org/aboutthefed/holiday_schedule.html).

For SOFR, FRBNY produces a value for every weekday, excluding days recommended by SIFMA for observance as US government securities market holidays. The SIFMA holiday calendar includes all Fedwire Funds Service holidays, plus Good Friday and any ad hoc National Day of Mourning. See https://www.sifma.org/resources/general/holiday-schedule/ and https://www.sifma.org/wp-content/uploads/2017/11/market-response-statement.pdf

8. See FRBNY, Additional Information about Reference Rates Administered by the New York Fed, last updated 6 April 2026, which is available at: https://www.newyorkfed.org/markets/reference-rates/additional-information-about-reference-rates

9. See Short-Term Interest Rate (STIR) futures Inter-Commodity Spreads on Globex for more details: https://www.cmegroup.com/trading/interest-rates/files/stir-inter-commodity-spreads-overview.pdf

10. See Change to Minimum Price Increment and Security SubType for One-Month SOFR versus Fed Fund Intercommodity Spread - June 14 for more details: https://www.cmegroup.com/notices/electronic-trading/2026/05/20260525.html#ctmpiassfosvffis