{kind=link}

Three-Month SOFR Futures Rates and Future SOFR Levels

Three-Month SOFR Futures Contract Rates and Future SOFR Levels

The price of any CME Three-Month SOFR (SR3) futures contract is quoted and dealt in terms of the familiar IMM Index -- 100 minus R – where R is the contract interest rate. After trading terminates in an expiring contract, the final settlement price is determined by the exchange as 100 minus R, with R set equal to compounded daily Secured Overnight Financing Rate (SOFR) interest during the contract reference quarter, expressed as a money market interest rate per annum.1

Example: For June 2018 SR3 futures (SR3M8), the contract reference quarter spans 91 days, starting on (and including) the third Wednesday of June, 20 June 2018, and ending on (and not including) the third Wednesday of September, 19 September 2018.

The contract interest rate conveys information about expected future values of SOFR --

- At any moment prior to the start of the reference quarter, R implies a unique hypothetical constant value of daily SOFR during the reference quarter.

- During the reference quarter, the daily SOFR values that enter into final settlement price determination become known, one by one. On any given day, market participants can combine such published SOFR values with the futures contract price to infer a unique hypothetical constant value of daily SOFR for the remainder of the reference quarter.

In what follows, three examples illustrate why this is so and how it works.

Basics

The Federal Reserve Bank of New York (FRBNY) produces a SOFR value for every weekday, excluding those days flagged by the Securities Industry and Financial Markets Association (SIFMA) as US government securities market holidays.2 The final settlement price of an expiring SR3 contract is based on SOFR values for all US government securities market business days (business days) occurring within the contract reference quarter. The compounding scheme employed in determining the final settlement price adheres to broadly accepted industry conventions,3 according to which:

- compounding of interest applies only to business days;

- simple interest applies to any day that is not a business day, at a rate of interest equal to the SOFR value for the first preceding business day; and

- simple interest accrues on the basis of a standard 360-day money market year (ie, actual/360).

Example: For any standard weekend, the SOFR value for Friday, r, applies as simple interest to the ensuing Saturday and Sunday. Thus, the interest amount that accrues over the weekend is assumed to equal Principle Amount x (r/100) x (3/360).

The link between the contract interest rate and expected future values of SOFR is rooted, in turn, in the method for setting the SR3 contract final settlement price.

To see how, consider the composition of the contract reference quarter for SR3M8. It comprises:

- one 4-day holiday weekend (Labor Day),

- 12 regular 3-day weekends (Friday + Saturday + Sunday),

- one 1-day holiday observance (Independence Day) entailing two days of simple interest, and

- 49 true overnight intervals.

The resultant relationship between the contract interest rate R and the hypothetical constant daily SOFR value during the contract reference quarter , r, is:

1+(91/360)(R/100) =

(1+(4/360)(r/100)) x (1+(3/360)(r/100))12 x (1+(2/360)(r/100)) x (1+(1/360)(r/100))49

Example 1 -- Tuesday, 19 June

On the day before its reference quarter begins, SR3M8 is priced at 98.075 points, making a contract interest rate of 1.925 pct (equal to 100 minus 98.075). Setting R = 1.925, the solution of the polynomial above is r = 1.92043 pct, the implied constant daily SOFR during the reference quarter.

Example 2 -- Friday, 22 June

FRBNY has published SOFR values for each of the first two days of SR3M8’s reference quarter:

Wed, 20 Jun = 1.87 pct

Thurs, 21 Jun = 1.87 pct

Assume SR3M8’s daily settlement price is 98.065 points on Thursday, 21 June, making a contract interest rate of 1.935 pct (equal to 100 minus 98.065). Each of the two published SOFR values applies to a true overnight interval (with no intervening weekend days or holidays), leaving 47 true overnight intervals in the remainder of the reference quarter. Thus, the relationship between the contract interest rate and hypothetical constant daily SOFR for the remaining 89 days in the reference quarter (r89) is:

1+(91/360)(1.935/100) =

(1+(1/360)(1.87/100))2 x

x (1+(4/360)(r89 /100)) x (1+(3/360)(r89 /100))12 x (1+(2/360)(r89 /100)) x (1+(1/360)(r89 /100))47

where entries in red font indicate known information (either the SR3M8 contract interest rate or published daily SOFR values). Solving the polynomial – the entries in black font – produces the implied expected constant daily SOFR for the rest of the reference quarter, r89 = 1.93174 pct.

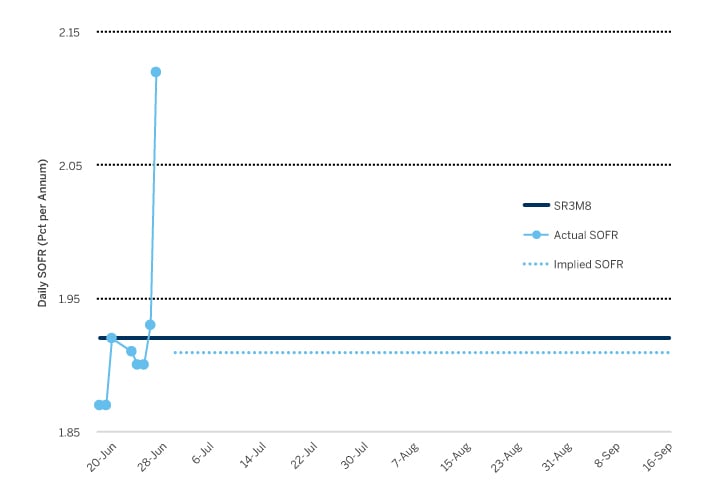

Example 3 -- Monday, 2 July

Suppose that:

- SR3M8 trades at a price of 98.075, for a contract interest rate of 1.925 pct, which implies, in turn, a constant daily SOFR value of 1.92043 pct for the entire reference quarter.

- FRBNY has published SOFR values for each of the first eight US government securities market business days of the reference quarter:

Wed, 20 Jun = 1.87 pct

Thurs, 21 Jun = 1.87 pct

Fri, 22 Jun = 1.92 pct

Mon, 25 Jun = 1.91 pct

Tue, 26 Jun = 1.90 pct

Wed, 27 Jun = 1.90 pct

Thurs, 28 Jun = 1.93 pct

Fri, 29 Jun = 2.12 pct These span 12 calendar days, comprising six true overnight intervals and two standard 3-day weekends. The applicable SOFR value is 1.92 pct for one of those weekends and 2.12 pct for the other.

If, as before, we partition the general polynomial relationship to reflect those intervals for which we possess information (in red font) and those for which we do not (in black font), we can estimate the implied constant daily SOFR value (r79) that market participants collectively expect to prevail during the remaining 79 days of the reference quarter:

1+(91/360)(1.925/100) =

(1+(1/360)(1.87/100))2 x (1+(3/360)(1.92/100)) x (1+(1/360)(1.91/100)) x

x (1+(1/360)(1.90/100))2 x (1+(1/360)(1.93/100)) x (1+(3/360)(2.12/100)) x

x (1+(4/360)(r79 /100)) x (1+(3/360)(r79 /100))10 x (1+(2/360)(r79 /100)) x (1+(1/360)(r79 /100))43

The solution is r79 = 1.914675 pct. Exhibit 1 illustrates.

Exhibit 1 – Daily SOFR Values for 2 July through 18 September Implied by SR3M8 Contract Rate on 2 July and True Daily SOFR Values for 20 June through 29 June

{kind=link}

Data Sources: CME Group, Federal Reserve Bank of New York

In general…

For SR3 futures for a given contract month, the final settlement price is the contract-grade IMM Index, 100 minus R, with R evaluated on the basis of realized SOFR values during contract reference quarter:4

| R | = | [ Πi=1…n ( 1+(di /360)(ri /100) ) – 1 ] x (360/D) x 100 |

| n | = | Number of US government securities market business days in the reference quarter |

| i | ~ | Running variable indexing US government securities market business days during reference quarter |

| Πi=1…n | denotes the product of values indexed by the running variable, i = 1,2,…,n. | |

| ri | = | SOFR value for ith US government securities market business day |

| di | = | Number of calendar days to which ri applies |

| D | = | Σi di (ie, number of calendar days in reference quarter) |

Recast in the form we’ve used in the preceding examples, this becomes:

1 + (D/360)(R/100) = Πi=1…n ( 1+(di /360)(ri /100) )

For any instance in which we know the contract interest rate R and the values of ri for the first k business days of the contract reference quarter, we can obtain the implied expected constant value of daily SOFR for the reference quarter’s remaining n-k business days by solving the following equality for r:

( 1 + (D/360)(R/100) ) = Πi=1…k ( 1+(di /360)(ri /100) ) x Πi=k+1…n ( 1+(di /360)(r /100) )

or equivalently

( 1 + (D/360)(R/100) ) / Πi=1…k ( 1+(di /360)(ri /100) ) = Πi=k+1…n ( 1+(di /360)(r /100) )

where, as before, entries in red font indicate information we know, and entries in black font impound the variable r for which we solve.

Please refer to www.cmegroup.com/sofr for One-Month SOFR futures and Three-Month SOFR futures contract specifications, press releases, and SOFR educational resources.

References

- See CME Rule 46002.C. (“Price Basis and Minimum Price Increments”) and Rule 46003.A.1. (“Definition of Reference Quarter”) in CME Rulebook, Chapter 460 (“Three-Month SOFR Futures”), available at: http://www.cmegroup.com/rulebook/CME/IV/400/460.pdf

Also see CME Group, Understanding SOFR Futures, 14 May 2018, available at:

http://www.cmegroup.com/education/articles-and-reports/understanding-sofr-futures.html - US government securities market holidays recognized by SIFMA comprise all Fedwire Funds Service holidays, plus Good Friday and any ad hoc National Day of Mourning. For more information, see https://www.sifma.org/resources/general/holiday-schedule/ and https://www.sifma.org/wp-content/uploads/2017/11/market-response-statement.pdf

- See especially International Swaps and Derivatives Association, Inc, Supplement 57 to the 2006 ISDA Definitions – USD-SOFR-COMPOUND, 16 May 2018, available at: https://www.isda.org/book/supplement-57-to-the-2006-isda-definitions/

- See CME Rule 46003.A.2. (“Definition of Final Settlement Price”) in CME Rulebook, Chapter 460 (“Three-Month SOFR Futures”).

Contact Us

For more information, please contact:

Jonathan Kronstein

+1 312 930 3472

jonathan.kronstein@cmegroup.com

David Reif

+1 312 648 3839

david.reif@cmegroup.com

Neither futures trading nor swaps trading are suitable for all investors, and each involves the risk of loss. Swaps trading should only be undertaken by investors who are Eligible Contract Participants (ECPs) within the meaning of Section 1a(18) of the Commodity Exchange Act. Futures and swaps each are leveraged investments and, because only a percentage of a contract's value is required to trade, it is possible to lose more than the amount of money deposited for either a futures or swaps position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles and only a portion of those funds should be devoted to any one trade because traders cannot expect to profit on every trade. All references to options refer to options on futures.

Any research views expressed those of the individual author and do not necessarily represent the views of the CME Group or its affiliates. The information within this presentation has been compiled by CME Group for general purposes only. CME Group assumes no responsibility for any errors or omissions. All examples are hypothetical situations, used for explanation purposes only, and should not be considered investment advice or the results of actual market experience.

All matters pertaining to rules and specifications herein are made subject to and are superseded by official rulebook of the organizations. Current rules should be consulted in all cases concerning contract specifications

CME Group is a trademark of CME Group Inc. The Globe Logo, CME, Globex and Chicago Mercantile Exchange are trademarks of Chicago Mercantile Exchange Inc. CBOT and the Chicago Board of Trade are trademarks of the Board of Trade of the City of Chicago, Inc. NYMEX, New York Mercantile Exchange and ClearPort are registered trademarks of New York Mercantile Exchange, Inc. COMEX is a trademark of Commodity Exchange, Inc. All other trademarks are the property of their respective owners.

Copyright © 2018 CME Group. All rights reserved.

SOFR Home

Return to the SOFR homepage for more information regarding contract specs, educational resources, and more.