{kind=link}

Options Strategies in Livestock: Part Two

Options Strategies in Livestock: Part 2

In Part 1 of this series, the growth factors behind the proliferation of agricultural options spread strategies in grains were evaluated using a series of trade volume data from 2017, 2018, and 2019. In Part 2 of this paper, we will focus on exploring the trends driving the utilization of options strategies in CME’s Livestock options complex and attempt to compare and contrast the most utilized strategies in the Live Cattle, Feeder Cattle, and Lean Hog options using data from 2017 through September 2020.

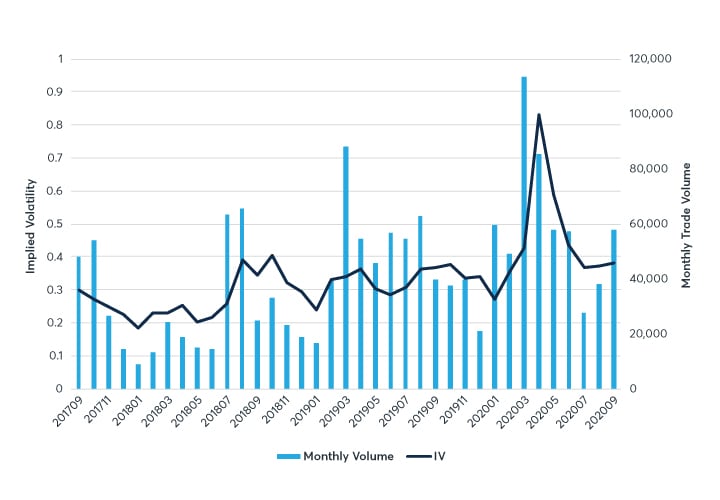

Since options were first offered electronically in 2012 on CME Group’s electronic platform, CME Globex, option spread strategy volumes have grown over 86 percent and account for 45 percent of total executed options volume today. This is slightly lower than the 50 percent observed in grains. However, this growth shows option spread strategies have become an increasingly popular tool in the Livestock option trader’s toolkit. To make executing these strategies easier, Globex has the ability to enter options spreads as one order through the Request for Quote (RFQ) functionality.

Figure 1: Livestock Option Spread Strategy Percent of Total Option Executed Volume

{kind=link}

Source: CME Group

Outright vs. Option Spread Strategy

While an outright represents an option that is bought or sold individually without the simultaneous placement of an offsetting hedge, an option spread strategy represents an options position that involves buying or selling multiple strikes and/or expirations on the same commodity. Utilized in the proper manner, option spread strategies can provide market participants added flexibility, lower cost, and more specified risk management characteristics when compared to outright strategies.

Who uses option spread strategies?

A broad spectrum of customers use agricultural option spreads. Depending on volatility levels and time of year, certain strategies may become more popular to optimize risk/reward profiles and mitigate risk. Additionally, for the cost-conscious risk manager, options strategies can effectively reduce margin requirements through creation of a defined risk profile. The rise of option analytical tools such as QuikStrike have allowed customers to build, view, and test option spreads making it easier for new traders to understand option spreads.

Asked why his customers like to trade spread options, George Haralambakis, founder of Bakis Commodities ‒ a Chicago-based livestock derivatives broker and advisory firm states, “Buying an option outright is viable and cost-effective risk management strategy but an option spread can be less expensive and still offer specific protection.”

Lean Hogs:

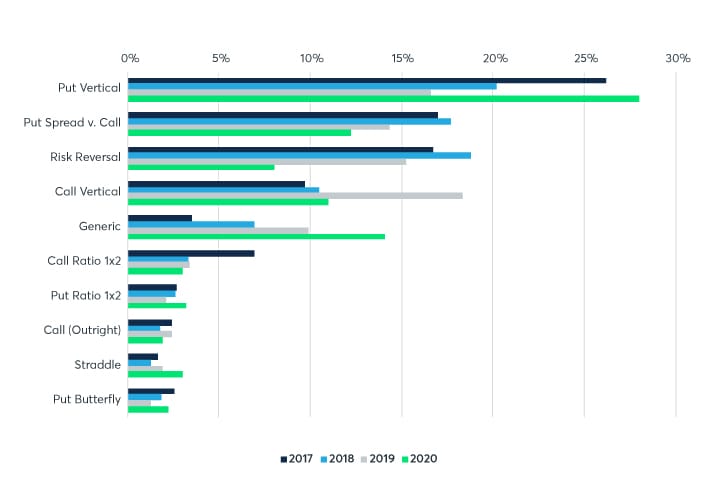

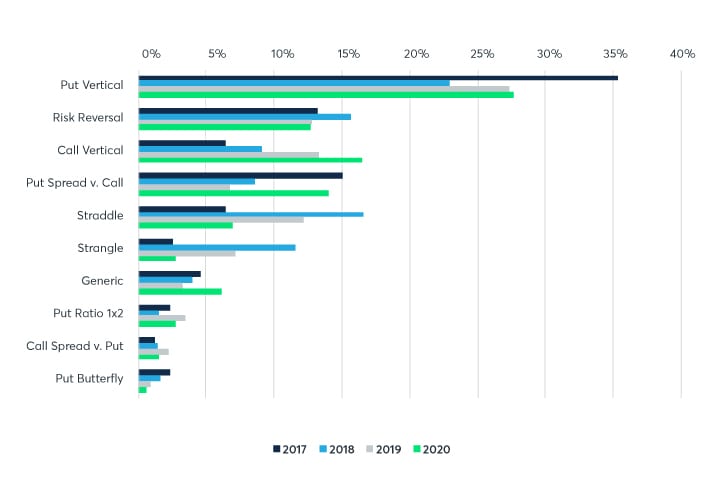

Figure 2: Top 10 Lean Hog Spread Option Strategies

{kind=link}

Source: CME Group

The most popular Lean Hog option spread strategies from 2017 through September 2020 (86 percent of total spread volume) include: Put Verticals, Put Spread vs. Calls, Risk Reversals, Call Verticals, Call Ratio 1x2s, Put Ratio 1x2s, Covered Calls, Straddles, and Put Butterflies. Of these, Put Verticals, Put Spread vs. Calls (three-way), and Risk Reversals make up the greatest proportion of Lean Hog spread volume. This could indicate the natural hedger in Lean Hogs has a propensity for using options strategies that mitigate downside price risk. Conversely, most of the prolific strategies in grain options demonstrated an inclination towards upside price risk management.

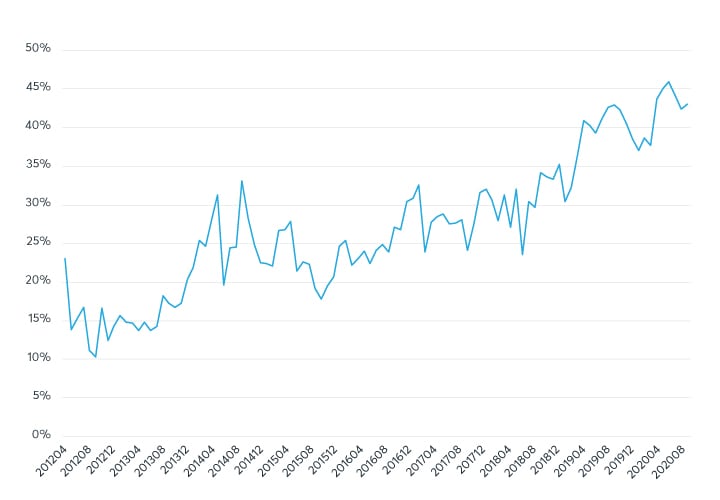

Figure 3: Monthly Lean Hog Put Verticals Volume vs. 30-day Implied Volatility

{kind=link}

Source: CME Group & Quikstrike

The 2019 and 2020 marketing years have experienced unprecedented volatility in Lean Hog options following the emergence of African Swine Fever (ASF) in China, the US-China Trade War, and the COVID-19 pandemic. As shown in Figure 3 above comparing monthly Put Vertical trading volume to implied volatility, option spread volumes tend to increase during periods of heightened volatility when option premiums are driven higher. Using one part of an options spread strategy to fund the other, these mechanisms offer downside coverage at more affordable premium costs vs. an outright put. In the case of Put Verticals, similar to Call Verticals, they offer market participants the ability to participate in upward or downward price movement at a known level of risk for a limited return by simultaneously buying and selling two different put options at the same time.

Live Cattle:

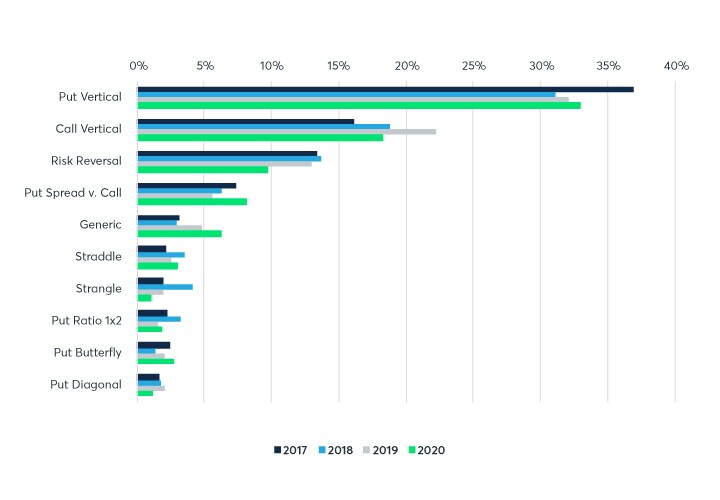

Figure 4: Top 10 Live Cattle Spread Option Strategies

{kind=link}

Source: CME Group

The most popular Live Cattle option spread strategies from 2017 through September 2020 (87 percent of total option spread volume) include: Put Verticals, Call Verticals, Risk Reversals, Put Spread vs. Calls, Straddles, Strangles, Put Ratio 1x2s, Put Butterflies, and Put Diagonals. Like Lean Hog volumes, Put Verticals lead the spread options volume in Live Cattle. However, Call Verticals rank much higher, averaging about 20 percent of the total Live Cattle spread option volume over the past four years. This could be indicative of the Live Cattle market structure in which commercial entities have price risk in both directions, purchasing live cattle and selling processed meat products.

Like the other livestock products, Live Cattle exhibits a mix of strategies affiliated with downside price risk management. The seasonal options skew in Figure 5 below provides a bit of insight behind this trend. Options skew compares the implied volatility of a call to the implied volatility of a put with both the call and put being the same distance away from the current price of the underlying. In this case, Figure 4 uses a 15-delta 60-day constant maturity with data going back to 2007.

Figure 5: Average Seasonal Livestock Complex Skew (2007- October 2020)

{kind=link}

Source: Quikstrike

Live Cattle, Feeder Cattle, and Lean Hogs have all experienced a historically larger put skew leading to low delta (1-20) puts exhibiting a higher implied volatility compared to equal distant calls or at-the-money options. Higher implied volatility of lower delta puts directly impacts the risk-reward profile of a Put Vertical strategy. In Lean Hogs, the seasonal skew shows a tendency to bottom out towards Q3, tying into the historically seasonal depression of pork prices following the end of summer grilling and gap period prior to holiday demand picking up. As seen in Figure 5, the average put skew over the last 13 years has the 15-delta put at a five to six percent higher implied volatility compared to a 15-delta call around August and October. On the other hand, both Live Cattle and Feeder Cattle maintain relatively stable skew throughout the season.

Feeder Cattle:

Figure 6: Top 10 Feeder Cattle Spread Option Strategies

{kind=link}

Source: CME Group

The most popular Feeder Cattle option spread strategies from 2017 through September 2020 (91 percent of total option spread volume) include: Put Verticals, Risk Reversals, Call Verticals, Put Spread vs. Calls, Straddles, Strangles, Put Ratio 1x2s, Call Spread vs. Puts, and Put Butterflies.

Standing apart from Lean Hogs and Live Cattle, Risk Reversals are typically the second most utilized option spread strategy in Feeder Cattle. Trey Warnock, Risk Manager at Amarillo Brokerage Company ‒ Texas-based firm specializing in agricultural risk management and commodity investments offers, “Risk Reversals are possibly one of the most widely used option strategies amongst medium to smaller (feeder cattle) operators. Buying a put and selling a call often can be done at a reasonable price that gives the cattle feeder or stocker operator a decent floor and a fair amount of upside potential.”

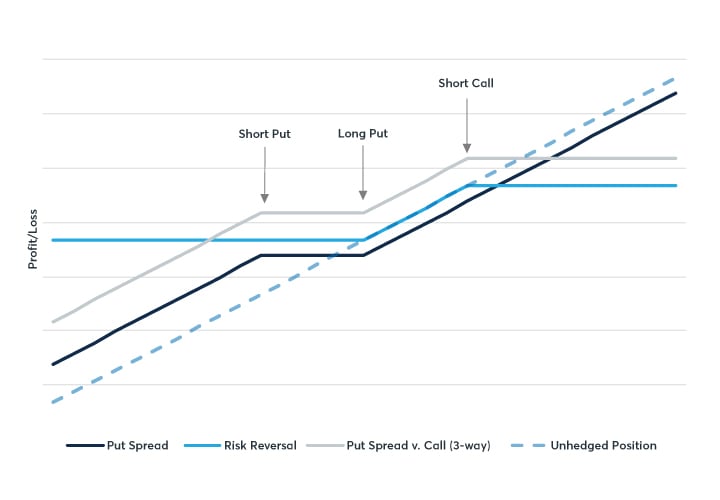

Figure 7: Risk-Reward Profile of Put Spread vs. Three-Way vs. Risk Reversal with Long Cash Exposure

{kind=link}

Source: CME Group

Figure 7 compares the different risk profiles of the top three strategies used to hedge a long cash position (Put Spread/Three-Way/Risk Reversal). All three strategies benefit from time decay of the short option, while providing offsets as the underlying futures price declines from the long put. Using different combinations of long and short options hedgers can create hedges and express a view on the market depending on their risk appetite.

Speaking to a Put Spread vs. a Call, also known as a Three-Way, Warnock adds further “For many of the same reasons a producer would buy a put or a Put Spread or a Risk Reversal, he might use a Three-Way. For most folks (not all) buying a put is the goal, but often times it is too expensive, so hedgers will choose to sell a put below (executing a Put Spread), sell a call above (executing a Risk Reversal), or sell a put below and call above (executing a Three-Way).” In the end, all three achieve downside coverage while reducing the overall cost of the strategy versus an outright put. On top of this, margin requirements are typically less with options than futures making them an attractive offer for the cost-conscious market participant.

Conclusion

It should be emphasized that these results are sensitive to the sample period and future relationships and characteristics could look very different. Nevertheless, as options spread strategies continue to proliferate throughout the agricultural markets and become an increasingly utilized instrument in the hedger’s toolkit, it would be worth noting how implied volatility, skew, and underlying fundamentals impact some of the strategies discussed above.

For more information and further insights on option strategies. please visit CME Group’s Options Strategy course.