{kind=link}

Exploring options on One-Month SOFR futures

Option applications:

- Hedge pricing risk and trade volatility at the short-end of the surface using options on One-Month SOFR.

- Trade outright against options on 30-Day Federal Funds and other futures.

- Specify levels with 6.25 basis point strikes

Following the successful launches of SOFR futures and options on Three-Month SOFR futures, CME Group launched options on One-Month SOFR futures (SR1 options) on May 4, 2020. SR1 options can be executed on three venues: open outcry, CME Globex, and as a block trade submitted via CME ClearPort.

In nearly all respects, the design of SR1 options mirror standard options on 30-Day Federal Funds futures (Fed Funds options). This paper provides in-depth descriptions of the SR1 options contract specifications, comparisons of SR1 and Fed Funds futures prices and a potential trading application.

Contract specifications

Exhibit 1 summarizes the contract specifications. In general, the option contract features closely mimic the CME’s extant suite of Fed Funds options. A noteworthy difference is the number of expiries: four SR1 compared to 24 Fed Funds expiries.

Exhibit 1

Contract specifications for options on One-Month SOFR futures

(All times of day are Chicago time.)

| Underlying instrument[text-align: left] | Each option is exercisable into one specified CME One-Month SOFR futures contract. |

| Expiries[text-align: left] | First four serial months (Jan, Feb, Mar, etc.) |

| Strike price listing[text-align: left] | Strike prices will be listed in increments of 6.25 basis points (0.0625) for the first ten strikes above and below the at-the-money strike, and 12.5 basis points (0.1250) for the next five higher/lower strike prices outside this range. At-the-money exercise price is the Option exercise price closest to previous daily settlement price of the option’s Underlying Instrument. |

| Minimum option premium increment[text-align: left] | One-quarter of one basis point (0.0025), or $10.4175 per contract |

| Termination of trading[text-align: left] | Trading in expiring options terminates at close of trading – typically 4 p.m. – on last day of trading. Last day of trading is the last business day of the contract month. |

| Option exercise[text-align: left] | American style. Option may be exercised by purchaser on any day that option is traded. Option purchaser’s clearing member firm must notify CME Clearing of intention to exercise no later than 5:30 p.m. on day of exercise. All expiring options outstanding and unexercised at Termination of Trading shall expire at 5:30 p.m. on last day of trading and, absent contrary instruction, shall be automatically exercised. |

| Position accountability and reportability[text-align: left] | Reportability threshold: 600 contracts Single-month and all-month accountability thresholds: 3,000 contracts |

| Trading and clearing hours[text-align: left] | Open Outcry: 7:20 a.m. to 2 p.m., Mon-Fri CME Globex: 5 p.m. to 4 p.m., Sun-Fri with a 60-minute break each day beginning at 4 p.m. CME ClearPort: 5 p.m. to 4 p.m., Sun-Fri with a 60-minute break each day beginning at 4 p.m. |

| CME Globex Algorithm[text-align: left] | Threshold pro-rata with lead market maker (LMM) (Q Algorithm) Top order allocation = 25%. Top order min = 50 contracts. Top order max = 1,500 contracts |

| Block trade minimum threshold level[text-align: left] | 250 contracts during Asian Trading Hours (4 p.m.–12 a.m., Mon-Fri on business days and at all weekend times) (subject to a 15-minute reporting window) 500 contracts during European Trading Hours (12 a.m.– 7 a.m., Mon-Fri on business days) (subject to a 15-minute reporting window) 1,000 contracts during Regular Trading Hours (7 a.m.–4 p.m., Mon-Fri on business days) (subject to a 5-minute reporting window) |

| Commodity code[text-align: left] | CME Globex: SR1 CME ClearPort: SR1 Open Outcry: S1O Clearing: SR1 |

Termination of trading

Termination of trading in any expiring option is scheduled to occur at close of trading on the last business day of the contract month.

Underlying instrument

Each option is exercisable into a specified CME One-Month SOFR futures (“futures”) contract.

Exercise price arrays

SR1 options offer exercise prices in increments of 6.25 basis points (0.0625 IMM Index point) and 12.5 basis points (0.125 IMM Index point).

The exercise prices for the 6.25 basis point increments will be listed daily 10 exercise prices above and below the nearest-to-the-money exercise price. For example, assume the prior day’s activity produced a nearest-to-the-money exercise price of 95.00. The 6.25 basis point increments would have produced a highest exercise price of 95.625 and the following exercise prices that are 25 basis points (0.25 IMM Index point) above the nearest-to-the-money: 95.0625, 95.125, 95.1875, 95.25. The 6.25 basis point increments would have produced a lowest exercise price of 94.3750 and the following exercise prices that are 25 basis points (0.25 IMM Index point) below the nearest-to-the-money: 94.9375, 94.8750, 94.8125, 94.75.

The exercise prices for the 12.5 basis point increments will be listed daily five exercise prices above and below the nearest 6.25 basis point increment. For example, assume the prior day’s activity produced a nearest-to-the-money exercise price of 95.00. The 12.5 basis point increments would have produced the following exercise prices that are above the highest 6.25 basis point increment: 95.75, 95.875, 96.00, 96.125, 96.25. The 12.5 basis point increments would have produced the following exercise prices that are below the lowest 6.25 basis point increment: 94.25, 94.125, 94.00, 93.875, 93.75.

Minimum option premium increment

For users of Fed Funds options, the pricing of SR1 options is familiar. They are based on 100 basis points (1.00 IMM Index point) representing $4,167 per contract. Equally, 0.01 IMM index point represents $41.67 per contract. Generally, with a few exceptions, the smallest price increment for SR1 options is a ¼ basis point (0.0025 IMM index point) equal to $10.4175 per contract.

Option exercise

SR1 options utilize the American-style option exercise. Therefore, the option buyer has the right to exercise the option on any day they are traded.

Comparing underlying One-Month SOFR and Fed Funds futures prices

Traders should be mindful of potential differences in SOFR and Fed Funds volatilities as they are developing option pricing models. Based upon One-Month SOFR and Fed Funds futures price data from May 2018 through Dec. 10, 2020, the rolling front serial contract months produced the following 20-day historical volatilities (annualized) and correlation of daily price changes:

Exhibit 2

One-Month SOFR and Fed Funds futures, 20-day historical volatility and correlation

| Product | Product code | Historical volatility |

| 30 Day Federal Funds futures | ZQ | 0.29% |

| One-Month SOFR futures | SR1 | 0.31% |

| Correlation | ||

| 0.9667 |

Rolling front serial contract month

Data source: CME Group

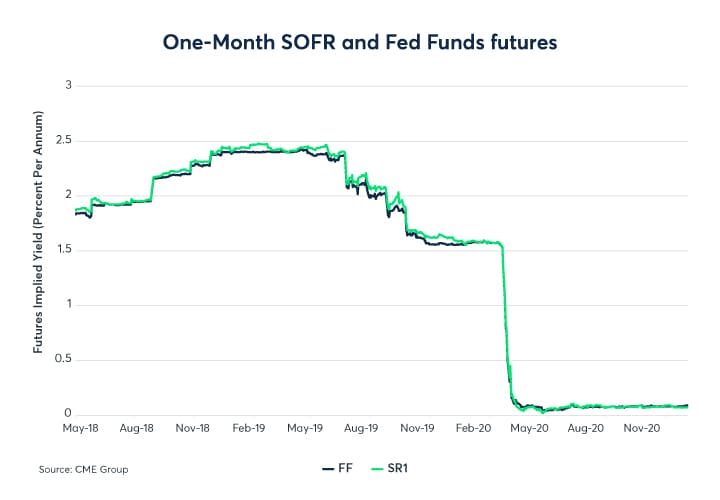

The high correlation and similar volatilities demonstrate Fed Funds (FF) futures and options are an appropriate hedge for One-Month SOFR (SR1) futures and options. Nevertheless, the difference in the chart of the implied yields shows the complementary nature of these products since the launch of SOFR futures in May 2018. The underlying effective federal funds and repo markets clearly have factors that may drive one and not the other. Please refer to Exhibit 3 below for the history of implied yields for FF and SR1 futures prices since May 2018.

Exhibit 3

One-Month SOFR and Fed Funds futures

Implied yields of the nearby contract, May 2018-Dec. 10, 2020

https://www.cmegroup.com/content/dam/cmegroup/education/images/2020/one-month-sofr-futures-fig01.jpg

{kind=link}

Data source: CME Group

Managing risk with One-Month SOFR options

Suppose you are concerned that year-end balance sheet pressures will lead to higher repo rates and lower SOFR futures prices. In 2018, overnight SOFR rose more than 50 basis points at year-end, from 2.46% to 3% on Dec. 31.

On Dec. 11, 2020, the Dec 2020 One-Month SOFR (SR1Z0) futures settled at 99.9275 (0.0725%), nearly identical to the latest SOFR print of 0.08% for Dec. 11. If similar circumstances occur, overnight SOFR would rise to 0.58%, projecting a final settlement price of 99.903 (0.097%) for SR1Z0 futures.

On Dec. 14, SR1Z0 99.9375 puts had a prior day settlement price of 2.5 basis points ($104.18 = ((0.025 X 100) X $41.67), giving them an implied volatility of 46.4% with 17 days to trade. Assuming a final futures settlement price of 99.903, the 99.9375 puts would have intrinsic value of 3.45 basis points ($143.76 = (0.0345 X 100) X $41.67) at expiration. Combining these puts with short positions in lower strike puts should produce more favorable outcomes.

Expanding the options

One-Month SOFR options are an ideal complement to manage front end funding risk and volatility exposures. Trade them outright or against the similarly construction Federal Funds futures. With continued monetary and fiscal policy providing unique risk to the front-end of the curve, One-Month SOFR options further complement the range of risk management tools available to manage interest rate volatility.