{kind=link}

JPY Downtrend Continues with US Yields on the Rise

The surge in US bond yields has been the main theme so far in 2021. The COVID 19 vaccine rollout has been one of the main contributors, and with the pace picking up, things are starting to look more optimistic globally. Concurrently, global stimulative fiscal policy measures remain in place and the Biden administration’s $1.9 trillion pandemic aid package will continue to boost these going forward.

{kind=link}

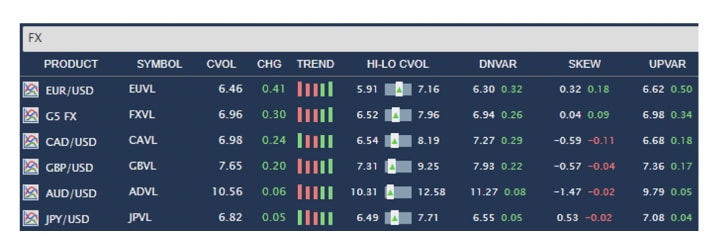

Changes in bond yields are one of the main contributors to FX market movements, and the yield on the benchmark UST 10Y has been pushed to its highest level in almost a year in the last few weeks. The above chart shows 1m ATM FX volatility across all currency pairs; vol is towards the lower end of the 1 M range but showing a ‘green’ trend.

JPY/USD is the pair most highly correlated to US yields, and JPY/USD volumes may be attributed to the recent move higher in US yields; higher yields would be associated with a higher USD and a lower JPY. JPY is still the worst-performing G10 currency this year, which is likely due to the return to deflation and Japans low yields making the JPY a popular funding currency for the carry trade; it’s cheap to borrow in JPY and earn interest in USD. Vols are slowly starting to creep back up but not breaking the upside, and investors can protect from a carry unwind by buying JPY calls.

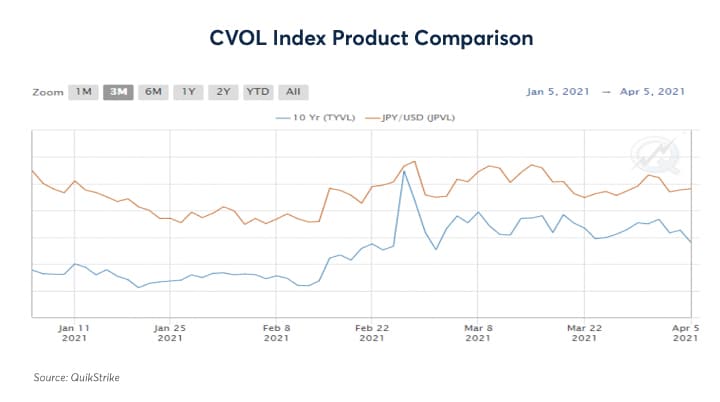

The CVOL chart below shows the correlation between JPY/USD and the UST 10Y price volatility over Q1 2021.

{kind=link}

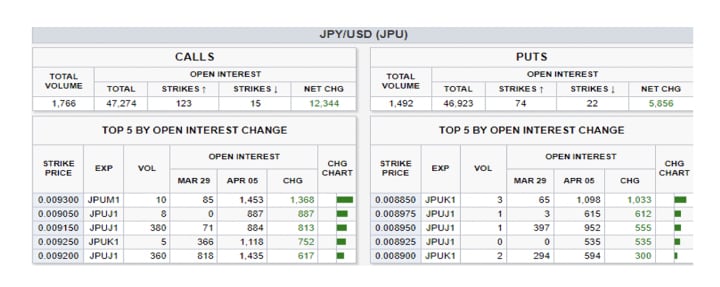

JPY/USD open interest change over the last week across the most active strikes – net OI change for JPY calls was over double the OI change for puts.

{kind=link}

Largest series by volume traded per currency pair over the previous two weeks

The most actively traded strikes were currency calls/USD puts with the largest volume in EUR/USD. In total, 55% of larger volume trades (over 400 lots) were calls and 45% were puts.

| Currency Pair | Contract | Call/Put | Strike | Total Volume (lots) |

| JPY/USD | June 21 | Call | 0.00930 | 1472 |

| CAD/USD | April 21 | Call | 0.8000 | 1230 |

| EUR/USD | May 21 | Call | 1.1800 | 2476 |

| GBP/USD | Sept 21 | Call | 1.4250 | 988 |

| AUD/USD | May 21 | Call | 0.7750 | 1207 |

Interesting spread trade strategies seen over the past 10 days:

- EUR/USD – double bullish position combination – a buy of 1.25-1.28 call spread for December expiry plus a buy of March 22 1.26 call; a bullish play in €375 million notional

- EUR/USD – a shorter-term bearish play with a 1.18-1.11 put spread for September expiry in over €200 million notional

- GBP/USD – a June 1.41-1.4350 1x2 – GBP bullish strategy in over $100 million notional