{kind=link}

Increasing Volatility Spurs Hedging Opportunities in Asian Rice

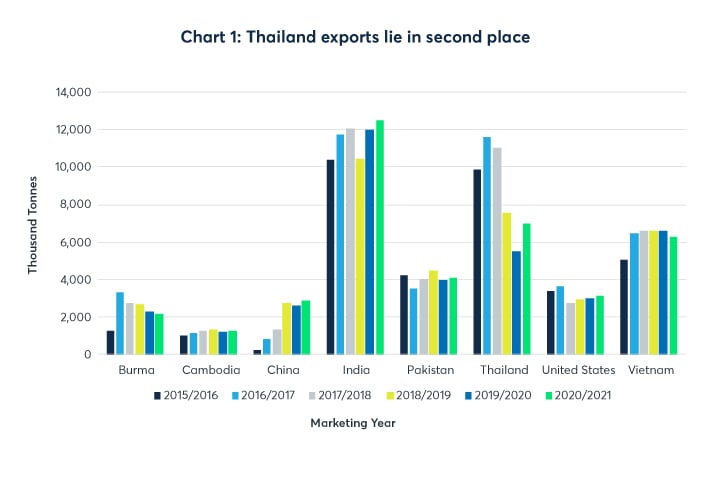

Thailand remains one of the world’s top rice producers and is the second largest exporter of rice behind India. The United States Department of Agriculture (USDA) suggests that Thailand remains on track to produce around 19 million tonnes of rice in the marketing year 2020-2021, a rise of 17% compared to 12 months earlier. Exports for the 2020-2021 marketing year are expected to reach around seven million tonnes, the USDA shows1.

Chart 1: Thailand exports lie in second place

{kind=link}

Source: USDA

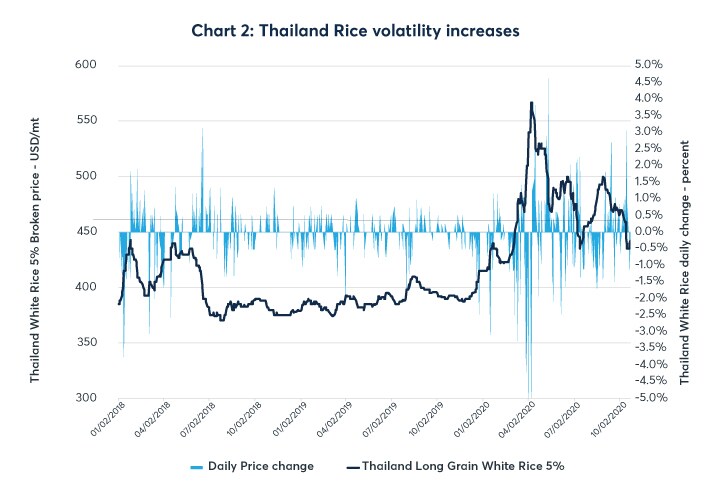

Much of the Asian rice market has typically been based on a series of fixed price deals between farmers and exporters to traders and end-consumers. During less volatile markets, this provided price certainty to both the supply side and the end-consumer. However, growing price volatility in rice markets has caused supply chains shorten to just a few weeks as market participants struggle to manage an increasing number of counterparty credit risk exposures. These issues are further complicated by the lack of hedging mechanism to manage price risk exposure beyond the CBOT Rough Rice futures contract2.

This increasing volatility prompted requests for financial instruments such as futures to manage the growing price risk. This article examines how market participants can use the CME Group financially settled Thailand Long Grain White Rice (Platts) futures to hedge exposure to Thailand physical rice prices.

Chart 2: Thailand Rice volatility increases

{kind=link}

Source: S&P Global Platts

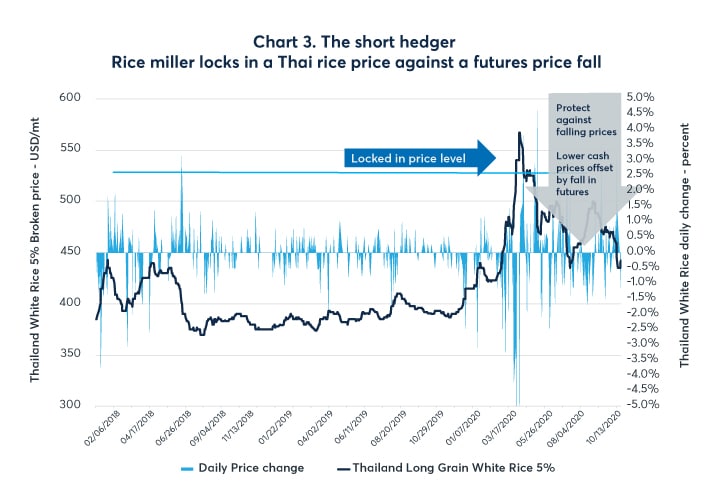

Short hedge example – a rice miller/exporter wants protection from falling prices

In April 2020, a rice miller/exporter agrees with a buyer to sell 5,000 tonnes of white rice for FOB delivery in August at a market price to be determined close to delivery. The rice miller/exporter is concerned about the impact of falling prices. By turning to the futures market, they can hedge their position thereby protecting against downside price movements in the physical market and can sell forward.

The chart below shows the historical Platts cash prices for Thailand Long Grain White Rice 5% broken FOB Bangkok since 2018. The example below shows how the rice miller/exporter could have protected themselves from the impact of falling prices by hedging with Thailand Long Grain White Rice (Platts) futures.

Chart 3: The short hedger Rice miller locks in a Thai rice price against a futures price fall

{kind=link}

Source data: S&P Global Platts

- In April 2020, the rice miller creates a hedge (short hedge) against a decline in Thailand long grain white rice market prices by selling 5,000 tonnes equivalent of August 2020 Thailand Long Grain White Rice futures (200 lots 3 ) at a price of $525/tonne, thereby locking in their sale price to a buyer at $525/tonne. They now hold a SHORT futures position.

- In early August, the rice miller agrees with the buyer to fix the delivery price of physical Thailand rice. Between April and August, the Thailand long grain white rice price has fallen to $440 per tonne.

- As the rice miller has now agreed with the buyer to supply the Thailand long grain white rice at $525 per tonne, they close out their equivalent 200 lot short futures position by buying back the 5,000 tonnes of Thailand Long Grain White Rice futures at $440 per tonne.

Short hedger example cash flow summary

Futures of 5,000 tonnes (200 contracts)

Sells April futures @ $525/tonne

Buys April futures @ $440/tonne

Futures gain of $85/tonne

Physical of 5,000 tonnes

Prices April physical at $440/tonne

EXAMPLE NET SALE PRICE WITH FUTURES = $440/tonne physical + $85 futures gain = $525/tonne (=August Thailand long grain white rice price in April)

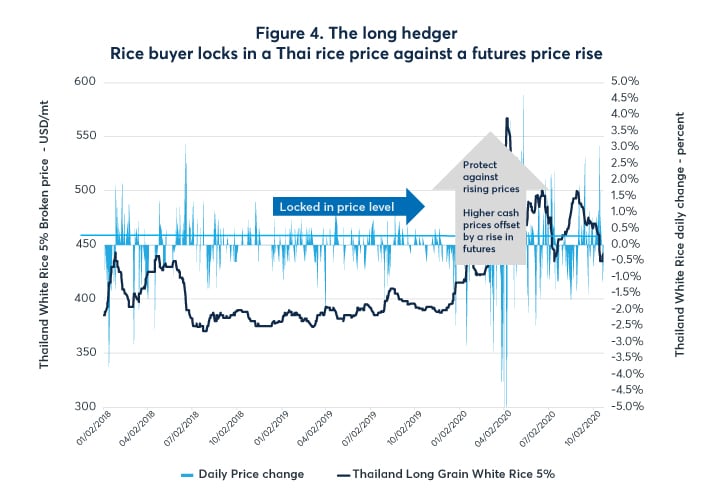

Long hedge example – a rice buyer wants protection from rising prices

Assume that in late June 2020, a buyer agrees with a rice miller/exporter to buy 5,000 tonnes of Thai rice for FOB delivery in September 2020 at a market price to be determined close to delivery. The buyer is concerned that Thai Rice prices will rise between June and September so wants to lock in a price to protect a profit margin in their retail business. By using Thailand Long Grain White Rice (Platts) futures to hedge, the buyer can protect against upside price movements in the physical markets and is able to buy forward.

The chart below shows the historical Platts cash market prices for Thailand Long Grain White Rice FOB Bangkok since 2018. The example below shows how a rice buyer could have protected themselves against the impact of rising prices by hedging with Thailand Long Grain White Rice (Platts) futures.

Chart 4: The long hedger Rice buyer locks in a Thai rice price against a futures price rise

{kind=link}

Source data: S&P Global Platts

- In June 2020 the buyer creates a hedge (long hedge) against a possible rise in the Thai rice market by buying 5,000 tonnes equivalent of Thailand Long Grain White Rice (Platts) futures for September 2020 (200 lots) at a price of $460 per tonne, thereby locking in their purchase price from the rice miller/exporter at $460 per tonne. They now hold a LONG futures position.

- In late August the trader agrees with the buyer to fix the delivery price of physical Thailand rice. Between June and August 2020, the Thailand long grain white rice price has risen to $560 per tonne.

- As the buyer has now agreed with the rice miller/exporter to buy the Thai rice at $560 per tonne, they close out their equivalent 200 lot short futures position by selling (back) the 5,000 tonnes of Thailand Long Grain White Rice futures at $560 per tonne.

Long hedger example cash flow summary – a rice buyer

Futures of 5,000 tonnes (200 contracts)

Buys March futures @ $460/tonne

Sells March futures @ $560/tonne

Futures gain of $100/tonne

Physical of 5,000 tonnes

Prices August physical at $560/tonne

EXAMPLE NET SALE PRICE WITH FUTURES = $560/tonne physical - $100 futures gain = $460/tonne (= September Thailand long grain white rice price in June)

Reasons for using Thailand Long Grain White Rice (Platts) futures at CME Group

As well as being able to protect against adverse price movements in the physical Thailand rice markets and buy/sell forward, the Thailand Long Grain White Rice futures contract comes with the safety and security of being cleared by CME Clearing, thus making the CME Clearing House the counterparty to each trade.

Key features of the Thailand Long Grain White Rice futures include:

- Effective price risk management for Thailand long grain white rice cash markets

- No physical delivery – cash-settled using Platts assessments

- Physical booked cargos can be hedged up to 12 months out

- Price settlements provided by CME Group daily 12 months out

- Numerous brokers provide access to the market

- Clearing addresses counterparty risk and widens the number of potential counterparties

| Contract Title | Thailand Long Grain White Rice (Platts) futures |

| Contract Size | 25 metric tonnes |

| Price Quotation | US dollars and cents per metric tonne |

| Tick Size (Minimum Fluctuation) | US $0.50 per metric tonne (US $12.50 per contract) Final settlement price fluctuation is $0.01 per metric tonne |

| Product Code | TRF |

| Trading Hours |

ClearPort: Sunday 5:00 p.m. – Friday 5:45 p.m. CT with a 15-minute maintenance window each day Monday – Thursday from 5.45 p.m. to 6.00 p.m. CT CME Globex: Monday – Friday 8:30 a.m. – 1:20 p.m. Central Time/CT. Pre-open: Monday-Friday 08:00 a.m. – 08:30 a.m. CT |

| Settlement time | 12:00 p.m. GMT |

| Listed Months | 12 months, starting with January 2021 |

| Settlement Method | Financially settled |

| Final Settlement Price | The final settlement price for each contract month shall be equal to the arithmetic average of the “Thailand Long Grain White Rice 5% broken FOB” price assessments published by Platts for each day that it is determined during the contract calendar month, rounded to the nearest $0.01. |

| Termination of Trading | Trading shall cease on the last business day of the contract month, which is also a Platts publication date for the price assessment. |

| Block minimum | Five lots ‒ subject to a 15-minute reporting window |

1 USDA Rice exports 2020/2021 (Rice, Production, Exports, Thailand, 2020 and 2021) https://www.cmegroup.com/psdonline/app/index.html#/app/advQuery

2 CME/CBOT Rough Rice futures contract specification https://www.cmegroup.com/trading/agricultural/grain-and-oilseed/rough-rice_contract_specifications.html

3 1 futures lot = 25 tonnes