{kind=link}

Increasing Volatility Drives Increased Opportunities for Hedging in Waste oils

Renewable fuels are set to play a significant role in the energy transition. Used cooking oil, a waste oil product extracted from the restaurant and takeaway trade, is one of the key feedstocks for both renewable distillates and biofuels. This article examines how commercial firms with renewable fuel exposure can use the futures markets to hedge their price risk exposure.

From 2021 onwards, the European Renewable Energy Directive (RED II) legislates for greater quantities of waste oil feedstocks in transport and other industrial uses. Given the potential rise in demand, shortages of waste feedstocks look likely.

Several European bio refineries that use alternative feedstocks such as palm oil and some vegetable oils are expected to turn to the waste segment as they strive to reduce net carbon emissions. The European CIF ARA UCO price is the main liquidity for all international origins and traded prices have captured the growing volatility in the market.

Equally volatile market conditions have been seen in the UCOME market for biodiesel, with end-buyers seeking to target a relatively small supply pool of feedstock.

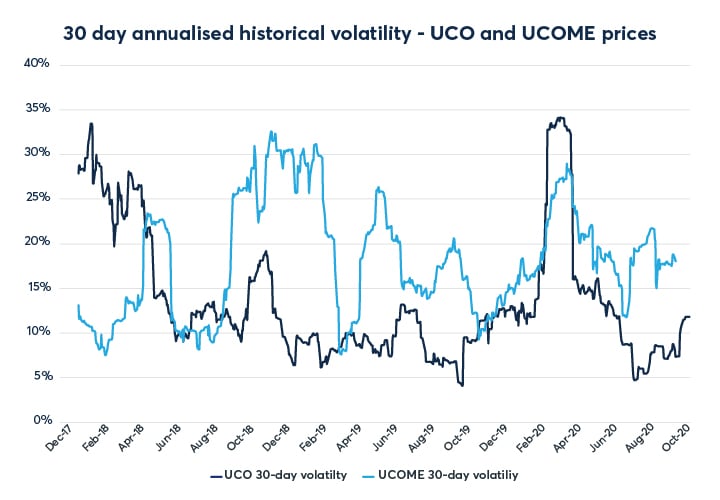

Chart 1: Volatility in waste feedstocks remains high

{kind=link}

Some traders believe that demand for products like UCO could rise to as much as 10 million tons per year from the current 1.5 million tons per year. With the rise in demand for waste feedstocks, several requests have been made for financial instruments such as futures to manage the growing price risk in the supply chain. To support these changes, CME Group launched a series of futures contracts on used cooking oil methyl ester (UCOME) biodiesel and used cooking oil (UCO). The first trades were concluded in September 20201.

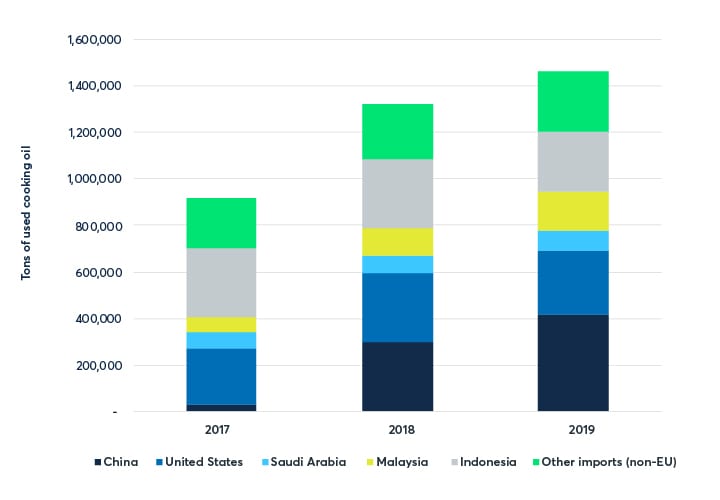

Chart 2: Imports of used cooking oils into northwest Europe

{kind=link}

Source: Eurostat data

Volatility impacts prices in UCO and UCOME

Prices have been volatile over the past 12 months as the coronavirus has impacted the availability of supplies. Retailer and food outlets have been unable to collect used cooking oil due to several global shutdowns to control the COVID-19 virus. Demand has also been curtailed, most notably in European biodiesel, due to the decline in road transport usage during the pandemic.

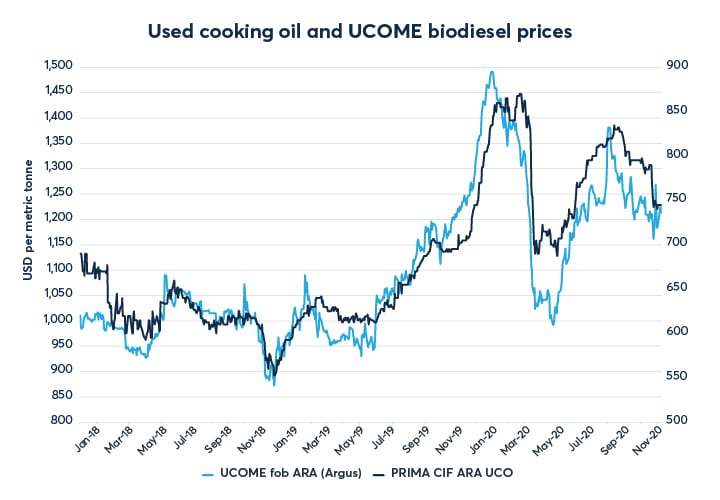

Chart 3: Used cooking oil and UCOME biodiesel prices

{kind=link}

Source data: PRIMA Markets and Argus Media

In 2020, European delivered used cooking oil prices have traded in about a $200 per metric tonne range with prices peaking at around $870 per metric tonne in early March before dropping around $100 per metric tonne in a 3-month period. European UCOME prices experienced similar sharp price movements. Prices for UCOME peaked around $1,500 per metric tonne in Q4 2019 before declining by over $500 per metric tonne around the end of April 2020. Prices have remained volatile through much of 2020 and traders believe that this trend will continue into 2021.

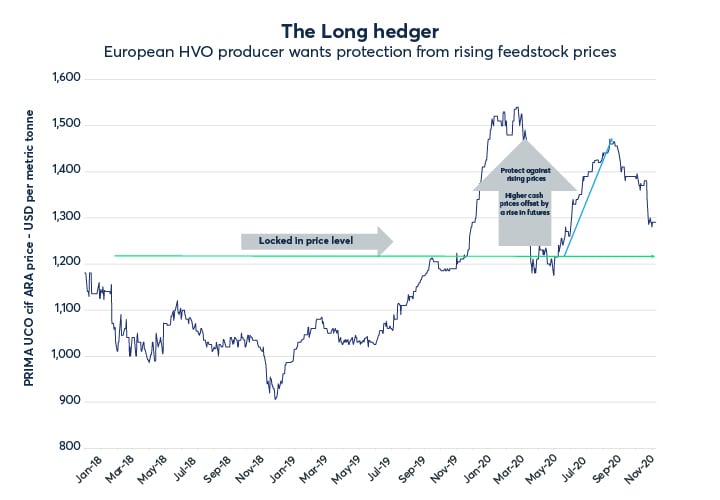

Long hedge example – a European HVO producer wants protection from rising waste feedstock prices

In May 2020, a European hydrotreated vegetable oil (HVO) producer agrees with a used cooking oil feedstock exporter to buy 2,000 tonnes of used cooking oil for delivery on a CIF basis in early September at a market price to be determined close to delivery. The European HVO producer is concerned about the impact from rising used cooking oil prices. By turning to the futures market, they can hedge their position thereby protecting against upwards price movements and can buy forward.

The chart below shows the historical price cash prices for the European UCO T1 (PRIMA) prices since December 2017. The example below shows how the European HVO producer could have protected their margins from the impact of rising feedstock costs by hedging with UCO T1 CIF ARA Excluding Duty (PRIMA) futures.

{kind=link}

Source data: PRIMA Markets

- In May 2020 the HVO producer creates a hedge (long hedge) against a possible rise in the used cooking oil market by buying 2,000 tonnes equivalent of UCO T1 CIF ARA (PRIMA) futures for September 2020 (20 lots) at a price of $687 per metric tonne thereby locking in their purchase price from the UCO exporter at $687 per metric tonne. They now hold a LONG futures position.

- In early September the trader agrees with the buyer to fix the delivery price of physical used cooking oil. Between May and September 2020, the European delivered price for used cooking oil has risen to $825 per metric tonne.

- As the European HVO producer has now agreed with the feedstock exporter to buy the used cooking oil at $825 per metric tonne, they close out their equivalent 20 lot Long futures position by selling (back) the 2,000 tonnes of UCO T1 CIF ARA (PRIMA) future at $825 per metric tonne.

Long hedger example cash flow summary – a European HVO producer looking to secure feedstock supply

Futures of 2,000 tonnes (20 contracts)

Buys May futures @ $687 per metric tonne

Sells September futures @ $825 per metric tonne

Futures gain of $138 per metric tonne

Physical of 2,000 tonnes

Prices September physical at $825 per metric tonne

EXAMPLE NET PURCHASE PRICE WITH FUTURES = $825 per metric tonne physical - $138 futures gain = $687 per metric tonne (= September used cooking oil import price in May)

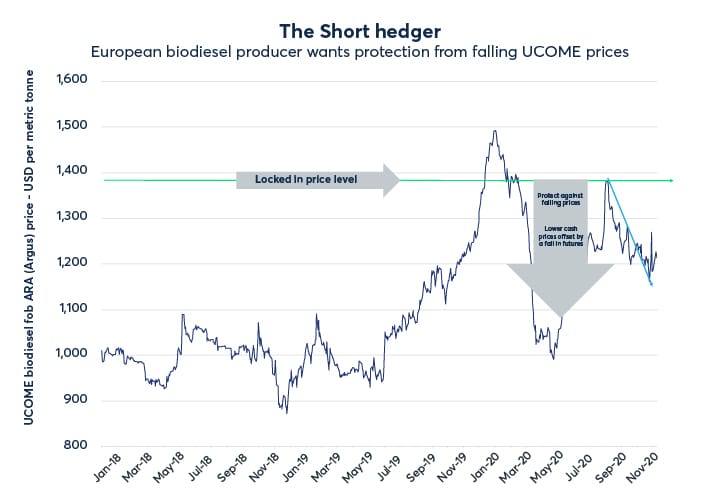

Short hedge example – a European biodiesel producer wants protection from falling UCOME prices

In early August 2020, a European biodiesel producer agrees with a distributor to sell 5,000 metric tonnes of UCOME in late October at a market price to be determined close to delivery. The European biodiesel producer is concerned about the impact from falling biodiesel prices. By turning to the futures market, they can hedge their position thereby protecting against downward price movements and can sell forward.

The chart below shows the historical price cash prices for the UCOME Biodiesel FOB ARA (Argus) prices since December 2017. The example below shows how the European biodiesel producer could have protected themselves from the impact of falling biodiesel prices by hedging with UCOME Biodiesel (RED Compliant) FOB ARA (Argus) Futures.

{kind=link}

Source data: Argus Media

It is worth noting that in some cases, biodiesel producers may also be concerned about the spread to low sulphur gasoil. Therefore, to protect themselves from a possible decline in the premium versus low sulphur gasoil they would have sold 50 lots of the UCOME Biodiesel (RED Compliant) FOB ARA (Argus) vs Low Sulphur Gasoil futures contract as a replacement futures hedge to the outright price of UCOME.

- In early August 2020, the biodiesel producer creates a hedge (short hedge) against a decline in the European UCOME biodiesel prices by selling 5,000 metric tonnes equivalent of October 2020 UCOME Biodiesel (RED Compliant) FOB ARA (Argus) Futures at a price of $1,375 per metric tonne thereby locking in their sale price to the distributor at $1,375 per metric tonne. They now hold a SHORT futures position.

- In late October, the biodiesel producer agrees with the buyer to fix the delivery of physical UCOME biodiesel. Between August and October, the UCOME biodiesel price has fallen to $1,175 per metric tonne.

- As the biodiesel producer has now agreed with the buyer to supply the UCOME biodiesel at $1,175 per metric tonne, they close out their equivalent 50 lot short futures position by buying back the 5,000 tonnes (equivalent) of UCOME biodiesel at $1,175 per metric tonne.

Short hedger example cash flow summary – a biodiesel producer wanting to protect from falling biofuel prices

Futures of 5,000 tonnes (50 contracts)

Sells October futures @ $1,375 per metric tonne

Buys October futures @ $1,175 per metric tonne

Futures gain of $200 per metric tonne

Physical of 5,000 tonnes

Prices October physical at $1,175 per metric tonne

EXAMPLE SALE PRICE WITH FUTURES = $1,175 per metric tonne physical + $200 futures gain = $1,375 per metric tonne (= October UCOME biodiesel price in early August)

Key use cases of UCO and UCOME futures at CME Group2

As well as being able to protect against adverse price movements in the waste feedstocks, waste biofuels markets and buy/sell forward, the futures contracts come with the safety and security of being cleared by CME Clearing, thus making the CME Clearing House the counterparty to each trade.

Key features of the futures include:

- Effective price risk management for both UCO and UCOME cash markets

- No physical delivery – cash-settled using either the used cooking oil (PRIMA) and or the UCOME biodiesel (Argus) assessments

- Physical booked deals can be hedged up to 18 months out

- Price settlements provided by CME Group daily 18 months out

- Numerous brokers provide access to the market

- Clearing addresses counterparty risk and widens the number of potential counterparties

1 CME announces first trade of UCOME https://www.cmegroup.com/media-room/press-releases/2020/9/23/cme_group_announcesfirsttradeofneweuropeanrenewablefuelcontract.html

2 UCO and UCOME Education https://www.cmegroup.com/education/articles-and-reports/faq-used-cooking-oil-uco-and-used-cooking-oil-methyl-ester-ucome-futures.html