{kind=link}

Global Feedstock Volatility Intensifies for Biofuels

The International Energy Agency (IEA) expects the biofuels market to grow 18% from 2019 levels by 2026. The transition to more sustainable fuels remains the cornerstone of environmental policy amongst regulators and will be critical in achieving net zero carbon emissions by 2050. The European biodiesel board estimates that for every 1 kilogram (kg) of biodiesel replacement leads to a reduction of 3s kg of Carbon Dioxide (CO₂)1. An increase in renewable fuels, including biodiesel and hydrotreated vegetable oils (HVO), or renewable diesel also reduces dependency on refined petroleum products.

European regulations, such as the Renewable Energy Directive (RED II)2, legislate for greater quantities of biofuels to be part of the road transport mix. However, rising volatility for the traditional feedstocks such as soybean oil and waste oils are major challenges that need to be managed. The competition between biodiesel and HVO producers for limited feedstocks are expected to increase leading to further possible price volatility amongst many of the relevant feedstocks. Companies are increasingly turning to the futures markets to manage price risk across the sector. Trading volumes have also responded to the increased client demand in many of the key benchmark futures products.

Competitive pressures push feedstocks higher

Biodiesel and HVO producers continue to face challenges in securing feedstocks amidst a rise in production capacity. In many cases, buyers are increasingly looking beyond the local markets to secure feedstocks.

Strong demand has pushed prices sharply higher in some of the key feedstocks such as in the vegetable oil markets. U.S soybean oil prices have more than doubled over the past 12 months to around 56 cents per pound. Part of this increase can be attributed to the demand for biofuels and HVO, but part is also due to the strong level of exports for soybeans3 resulting in less supply being available to be crushed into oil4. Soybean oil exports have been rising from both the USA and Argentina. According to the latest United States Department of Agriculture (USDA), total exports reached around 7.1 million tons in the 2020-2021 marketing year, up from around 6.6 million tons in the prior 12-month period.

Waste biofuel markets such as used cooking oils and animal fats have also been trading at close to record levels. Part of the reason for the shortage is the continued coronavirus pandemic which has curtailed supplies, notably from the hospitality sector due to ongoing restrictions.

Feedstock prices can be hedged in futures

CME Group lists the global benchmark for Soybean Oil futures and options. These tools enable the price risk management of these feedstocks.

Other vegetable oil futures for Palm Oil and a waste Used Cooking oil (UCO) futures are also listed futures contracts to further support client risk management needs. These products feature in feedstock choice by the growing number of biodiesel and HVO producers. In the case of UCO, Rotterdam prices are increasingly seen as the internationally relevant price for the world market, which is also the basis of the CME futures contract5.

{kind=link}

Source: CME Group

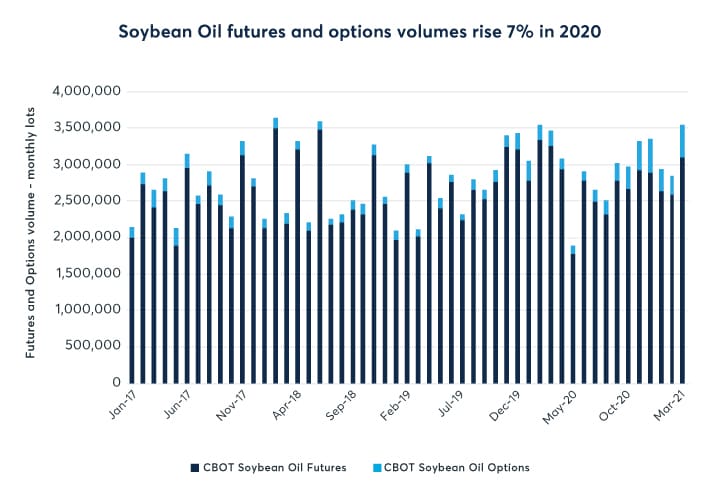

Buoyant Energy feedstock demand supports Soybean Oil futures

The demand for feedstocks has supported U.S Soybean Oil futures and options volumes, CME Group data shows. Total futures and options volumes in 2020 were 35.7 million lots or 143,000 lots per day, a rise of 7% year on year (equates to about 975 million tons per year). This is the equivalent to a multiple of 15 times the global soybean oil production volume. These contracts are traded by a wide range of firms globally including exporters, importers, oil seed crushers, and biodiesel producing firms.

{kind=link}

Source: CME Group

Oil demand is changing the dynamics of the soybean trade

The strength of Soybean Oil futures prices relative to Soybean Meal futures prices suggests that U.S. soybean crushing is likely being driven more by the demand for soybean oil than in the recent past. One question many are considering is whether this result is temporary, or part of a longer-term trend supported by greater soybean oil demand. Soybean meal is used as high-protein animal feed while soybean oil is a vegetable oil used in various food, fuel and industrial applications. The demand for biofuels is changing the relationship between meal and oil, a key indicator for the soybean oil refiners.

The so-called Soybean Oil futures share of the soybean crush margin has recently hit the highest level in over five years, driven in part by the demand for feedstock for the biofuel industry as governments looks to more sustainable energy sources for the future.

{kind=link}

*Rolling 20-day average prices

Source: CME Group

Strong production growth expected for biofuels

The size of the global biofuels market6 in 2020 was 144 billion litres7 equivalent to 2.48 million barrels per day. This represents a drop of around 11.6% on 2019 levels, partly due to the COVID-19 pandemic. However, production is expected to rebound strongly through 2025. The IEA expects biofuel production could increase to 162 billion litres in 2021, rising to over 175 billion litres or just over 3-million barrels per day over the 2023-2025 period.

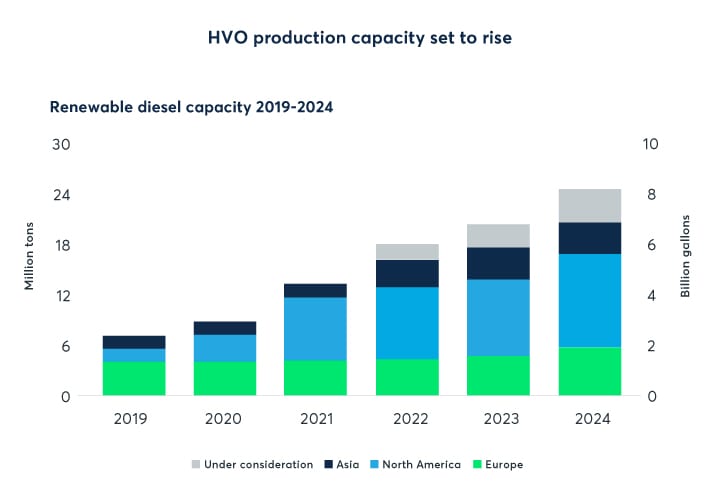

The U.S. expands Europe’s lead in HVO production

HVO is growing in importance globally. Unlike conventional biodiesel markets which are restricted by blending walls delineated by national fuel specifications, the blends in HVO can contain up to 100% of the renewable feedstock to make renewable or green diesel. HVO is also seen as a key product for manufacturing other products including sustainable aviation fuel, renewable naphtha, and renewable propane.

HVO production is a growing market, and Europe currently leads the charge on existing production capacity with about four million tons per year split between a small number of producers. However, the growth over the coming years is expected to come from the U.S. and Asia. The IEA estimates that around half of the planned increases out to 2025 will come from both regions. Total U.S. production capacity of HVO is expected to reach 10 million tons by 20248, an increase of eight million tons from current levels, according to Bloomberg New Energy Finance. Global HVO capacity is expected to reach 24 million tons by 2024.

Renewable diesel refiners will use a selection of feedstocks depending partly on availability and partly on the greenhouse gas savings offered. The most common feedstocks are vegetable oils, animal fats, waste oils, and biomass.

{kind=link}

Source: BloombergNEF, company announcements

Feedstock selection will remain a critical component of the market as more producers bring production capacity onto the market. This creates the situation where many producers are all chasing the same feedstocks with vegetable oils, waste oils, and animal fats at the top of the wish list

The credits do the talking

According to the latest RED II Directive in Europe9, hydrotreated vegetable oil made from rapeseed, sunflower oil, or soybean oil compare favourably with each other in terms of typical greenhouse gas savings (GHG). The directive shows a saving of around 55%. Waste oil feedstocks yield higher savings with GHG savings of up to 87% for waste cooking oil and 83% from animal fats. For this reason, producers are paying particularly close attention to the second-generation feedstocks. However, it is worth pointing out that the waste oils remain in tight supply with many producers aiming to secure the same feedstocks for their production output.

Carbon intensity levels vary according to feedstock choice. Typically, the waste feedstocks afford the producers higher carbon intensity credits compared to non-waste feedstocks such as vegetable oil or crop-based feedstocks. Under the California Low Carbon Fuel Standards legislation, the carbon intensity requirements increase over time meaning that the highest credits are only available for the more green and sustainable feedstocks. This may increase the pressure further on some of the key feedstocks that afford lower carbon intensity levels. CME Group offers futures on the Low Carbon Fuel Standard (LCFS) which is a financial product that allows customers to hedge exposure to the LCFS10.

Waste oils market set to rise

The size of the waste market varies by operator, with ranges estimating from 20 million tons to 30 million tons per year. Barclays estimates that demand will increase by 19 million tons a year by 2030 ‒ suggesting that unless operators are able to double the size of the waste resources pool over the next ten years, the market could possibly experience a period of tightness.

{kind=link}

Source: Barclays Research

Biodiesel producer margins threatened by rising feedstock costs

The Soybean Oil to NYMEX ULSD (diesel) spread is one of the commonly traded financial instruments used by the biodiesel industry, notably in the Americas. It is a good barometer for biodiesel producer margins (for soybean oil). Producers will typically use a range of feedstocks and their choice of feedstocks will be driven by the relative economics, which include the level of credits that a producer would receive from the LCFS. Higher carbon intensity products will receive less credits than the lower carbon intensity feedstocks.

Over the past 12 months, Soybean Oil futures prices have doubled, narrowing producer margins. In March and April 2019, soybean oil prices were trading at a discount to diesel prices. If a producer had hedged the price of soybean oil in March 2020, a purchase price of $200 per metric ton could have been achieved. Considering any carbon credits that a producer may receive via the LCFS, this could have led to a potentially higher margin.

Whilst soybean oil is a commonly traded feedstock globally, it will also have to be priced at a level to compete with less carbon intense alternatives such as waste where producers are likely to receive higher credits from the LCFS market.

{kind=link}

Source: CME Group

As the energy market transitions to less fossil fuel-based products and lower carbon intensity, biofuels and HVO appears to be a significant part of the solution. Production capacity is increasing but this is pulling on an increasingly short supply chain of feedstocks such as vegetable oils, waste oils, and animal fats and greases. This increases the importance of hedging the price of these key feedstocks such as soybean oil in the biofuels sector as it enables producers to manage their input leg of the biodiesel production.

With around 64 countries globally having some form of a biofuel mandate, feedstock choice is going to become a crucial issue in the years ahead. Feedstock selection will remain a critical component of the market as more producers bring capacity onto the market. This creates the situation where many producers are all chasing the same feedstocks with vegetable oils, waste oils, and animal fats at the top of the wish list. These factors are expected to impact margins in the future but are also a lesson about the benefits of hedging an increasingly volatile commodity.

References

- European Biodiesel Board https://www.ebb-eu.org/biodiesel.php

- RED II EU Directive https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32018L2001&from=fr

- https://www.cmegroup.com/education/articles-and-reports/chinas-high-demand-for-soybeans-fuels-asian-hours-futures-trading.html

- CME Group – China’s high demand for Soybeans fuels Asia Hours futures trading https://www.cmegroup.com/education/articles-and-reports/chinas-high-demand-for-soybeans-fuels-asian-hours-futures-trading.html

- CME UCO Futures – FAQ https://www.cmegroup.com/education/articles-and-reports/faq-used-cooking-oil-uco-and-used-cooking-oil-methyl-ester-ucome-futures.html

- Split between Biodiesel, Ethanol and HVO https://www.iea.org/reports/renewables-2020/transport-biofuels

- IEA Report November 2020 Transport biofuels https://www.iea.org/reports/renewables-2020/transport-biofuels

- P66 converts Rodeo refinery in California into world’s largest renewable diesel refinery from 2024 (1-mil tons per year) - https://investor.phillips66.com/financial-information/news-releases/news-release-details/2020/Phillips-66-Plans-to-Transform-San-Francisco-Refinery-into-Worlds-Largest-Renewable-Fuels-Plant/default.aspx

- EU Legislation 2018/2001 https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32018L2001&from=fr

- Prima – Low Carbon Fuel Standard futures https://www.cmegroup.com/trading/energy/emissions/california-low-carbon-fuel-standard-prima_contract_specifications.html