{kind=link}

Black Sea Corn futures boosted by strong eastbound flows

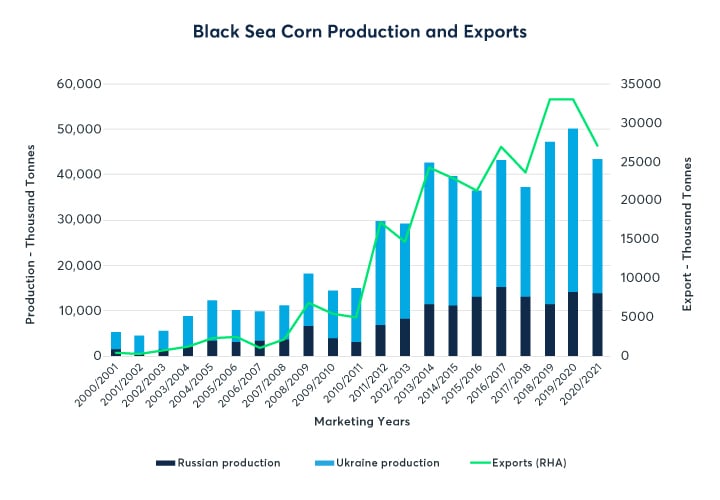

The Black Sea region is emerging as a major center for corn production with volumes rising in both the Ukraine, and increasingly, Russia. The latest data from the United States Department of Agriculture (USDA)1 shows production from both countries at around 43.5 million tonnes in the 2020-2021 marketing year, a continuation of trend-level growth in Black Sea production. Total production in the 2020-2021 marketing year is up 16% compared to the 2017-2018 marketing year but down slightly from the record production in 2019-2020

{kind=link}

Source: USDA

Competition heats up for corn exports

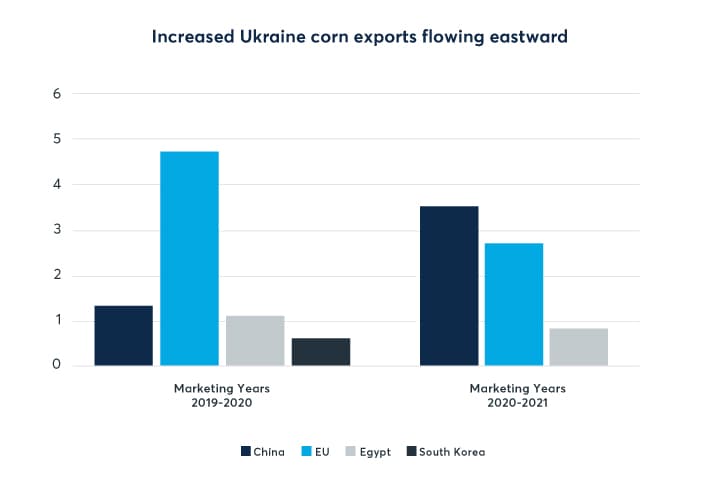

Ukrainian corn exports have remained strong despite a year-on-year decline from the record exports posted during the prior 12-month period. Total Ukrainian and Russian exports for the 2019-2020 marketing year were 33 million tonnes, representing a rise of over 43% from the 2017-2018 marketing year export volumes.

The European Union remains a significant corn importer despite a fall in volumes year on year. Based on the latest UN Comtrade data, total E.U. corn imports were just over 1.3 million tonnes per month, down 23.5% from the same period 12 months earlier. Imports from Ukraine represented about 56% of total European import volumes. The Netherlands was the largest corn importer with total volumes around 500,000 tonnes per month between January and October 2020 of which half originated from the Ukraine. Dutch volumes were flat year on year compared to the same period in 2019.

Global corn trade has also been rising with volumes increasing sharply year on year. S&P Global Platts estimates that China will consume 282 million tons of corn in the 2020-2021 marketing year, up sharply from the previous five year average of 248.3 million tons2. Given the uncertainty around future US-China relations, producers in the Black Sea are expecting to see increased shipments. China remains on track to be the largest corn importer for the marketing year 2020-2021. Ukraine is expected to be one of the major suppliers with exports increasing. Between October 2020 and February 2021, Ukraine exported a total of 4.5 million tons to China. Total exports are expected to reach seven million tons for the 2020-21 marketing year, up 1.5 million tons from the 2019-20 marketing year.

China has become a major buyer of corn, in part to fuel its road transport industry with corn-based ethanol but also on the back of rising grain demand for sectors such as animal feed. In addition to growing Ukraine exports, China has also been stepping up its purchases of US corn. According to the latest USDA data, China bought 1.36 million tons of U.S. corn in late January 2021 bringing the total imports for the 2020-2021 marketing year to 11.76 million tons.

{kind=link}

Source: Argus Media3

Black Sea Corn futures sees strong year-on-year growth

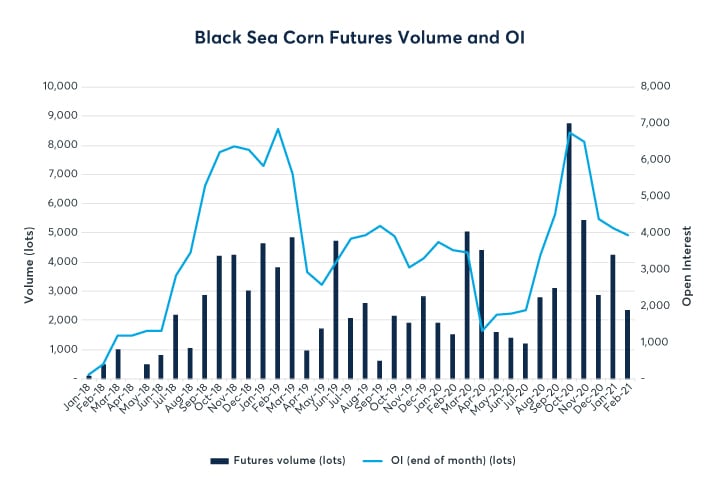

Launched in December 2017 as a price risk management tool for corn exports from the Black Sea region, the futures and options contracts have seen quick adoption as a hedging tool and trading instrument by a wide range of physical market participants ‒ including producers, exporters, trading houses, and processors in Europe, the US, Middle East, and Asia.

Chart 2 shows the volume and open interest of the Black Sea Corn futures and options by month since launch. Total futures volume traded for 2020 was 40,000 lots, equivalent to two million tonnes of corn. This represented an increase of 25% from the 2019 levels. There were around 160 lots of Black Sea corn traded per day in 2020. Open interest in Black Sea Corn futures was 4,387 lots at the end of December 2020, a rise of 32% from the same point a year ago. The 2020 volumes represent around 7% of total Ukraine production for the 2020-2021 marketing year, USDA data shows.

{kind=link}

Source: CME Group data

Black Sea Corn futures correlates highly with regional corn cash markets

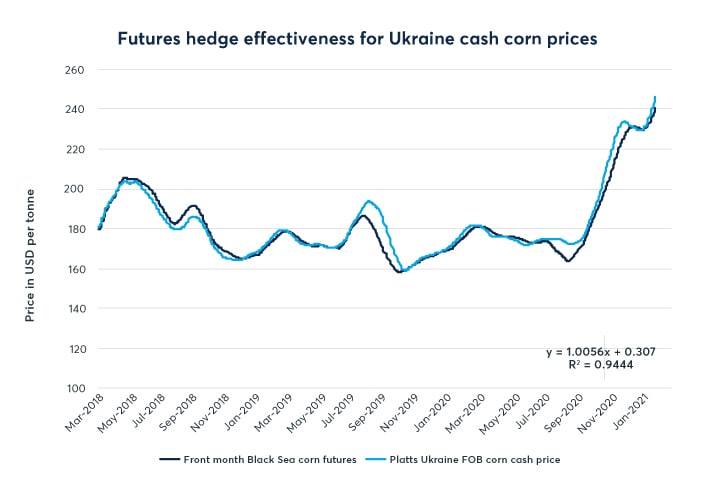

Price correlation measures how effective a hedge would be using a futures contract to manage price risk in a physical cash market. A score of 1.0 is considered a perfect hedge and a figure above 0.80 represents an effective hedge.

Chart 3 shows the prices of both the front month Black Sea Corn futures and the Ukraine fob cash market prices, as well as the hedge effectiveness between the two. The hedge effectiveness for Black Sea Corn futures prices against regional cash prices is high – well above 0.80. The hedge effectiveness was calculated using the rolling 30-day average prices for Black Sea Corn Financially Settled (Platts) futures and Ukraine fob cash corn prices and the data shows a correlation of 0.94.

{kind=link}

Source: CME Group and S&P Global Platts

Basis trading using Black Sea Corn futures

Basis trading is the buying and selling of a physical commodity such as Black Sea corn priced against a correlated futures price. This is a widely used trading and hedging concept in grain markets. Related futures and regional/local physical prices typically move up and down together, enabling hedging to occur.

Market participants may choose to fix the basis when they agree to a trade or they may choose to let the basis fluctuate until the delivery of the physical corn occurs. For example, processors that purchase physical Black Sea corn can use the Black Sea Corn futures, referenced to the Platts FOB Black Sea corn assessment, coupled with a negotiated basis to hedge price risk in their location. With a basis trade, only the difference in price between the physical price and the related futures (i.e. the basis) needs to be negotiated between the buyer and seller.

Purchasing physical shipments of Black Sea corn coupled to Black Sea Corn futures plus a negotiated basis enables buyers to use the Black Sea Corn futures to hedge price exposure to their local corn prices either within the Black Sea region or other destinations with market prices correlated to Black Sea Corn futures.

Hedging using basis – a Dutch importer

The Netherlands is the largest importer of corn in the European Union. Total imports are about 40% of the total European volumes (EU-27).

For example, a Rotterdam corn importer looking to hedge corn imports delivered into a warehouse in the Netherlands. Rather than waiting to purchase at a fixed price delivered into the Netherlands and taking on the price risk inherent in such a trade, this Dutch importer could purchase Black Sea corn for future delivery at a basis to a Black Sea Corn futures contract, thereby hedging their exposure to adverse price movements in the Dutch corn price.

For example, in January, a Dutch importer plans to buy 25,000 tonnes of Ukrainian corn from a Ukrainian corn exporter for May CIF Rotterdam delivery. Assume the May Black Sea Corn futures are trading at $260 per tonne and the CIF Rotterdam cash price is $30 over the futures price for an expected purchase price of $290 per tonne ($260 per tonne plus $30 basis).

Basis remains unchanged at +$30

| Timeline | Cash market | Futures market | CIF Rotterdam cash price – futures = basis |

| January | forward May cash corn is trading at $290/mt | buy May Black Sea Corn futures at $260/mt | +$30 |

| May | cash corn price rises to $320/mt | sell back May Black Sea Corn futures at $290/mt (to close out the futures position) | Basis unchanged at +$30 |

| Change | $30/mt increase | $30/mt gain | |

| Buy cash corn | $320/mt | ||

| Gain on futures position | $30/mt | ||

| Net purchase price | $290/mt |

The basis increases to +$50

| Timeline | Cash market | Futures market | CIF Rotterdam cash price – futures = basis |

| January | forward May cash corn is trading at $290/mt | buys May Black Sea Corn futures at $260/mt | +$30 |

| May | cash corn prices rise to $320/mt | sells back May Black Sea Corn futures at $270/mt (to close out the futures position) | Basis increases to +$50 |

| Change | $30/mt increase | $10/mt gain | |

| Buy cash corn | $320/mt | ||

| Gain on futures position | $10/mt | ||

| Net purchase price | $310/mt |

The basis falls to +$10

| Timeline | Cash market | Futures market | CIF Rotterdam cash price – futures = basis |

| January | forward May cash corn is trading at $280/mt | buys May Black Sea Corn futures at $250/mt | +$30 |

| May | cash corn prices rise to $320/mt | sells back May Black Sea Corn futures at $310/mt (to close out the futures position) | Basis falls to +$10 |

| Change | $40/mt increase | $60/mt gain | |

| Buy cash corn | $320/mt | ||

| Gain on futures position | $60/mt | ||

| Net purchase price | $260/mt |

As the examples above illustrate, basis is always changing. However, changes in the basis are usually much less volatile than changes in price, so a market participant can significantly reduce risk trading basis compared to trading flat price. Using FOB Ukraine cash prices and futures, the basis, discounting the cost of freight, has traded in a range of -$6 per ton to as much as $15 per ton4. A basis trader exchanges flat price risk, which tends to be high, for basis risk, which tends to be lower.

Black Sea corn production volumes are continuing to rise supporting the growth in the futures markets. Strong global demand for corn is also driving higher exports from suppliers such as the Ukraine and Russia. New markets are also emerging with Asia picking up increasing supplies from the Black Sea region. Volatility in corn prices is creating more hedging opportunities for commercial hedging and interest around corn basis is continuing to grow. This growth in corn comes on the back of recent strong growth in the region’s wheat markets5.

Key features of the Black Sea Corn futures include:

- Effective price risk management for Black Sea corn cash markets

- No physical delivery – cash-settled using Platts assessments

- Physical booked cargos can be hedged up to 15 months out

- Price settlements provided by CME Group daily 15 months out

- Numerous brokers provide access to the market

- Clearing addresses counterparty risk and widens the number of potential counterparties