{kind=link}

A Cost Comparison of S&P 500-related Options

Introduction

When it comes to trading S&P 500 options, there are multiple products available to investors and a multitude of factors to consider before choosing the optimal product. This report focuses on transactional liquidity and compares the relative execution quality between two of the most liquid S&P 500-related options products: CME’s options on E-mini S&P 500 futures (ES) and CBOE’s options on the S&P 500 cash index (SPX). The analysis to follow shows that, on average, ES options can offer superior execution relative to SPX options by between 0.04 to 0.15 index points. In dollar terms, ES options offer cost savings of $4 to $15 per contract.

Liquidity Framework

Framework: A mid-sized institutional investor executes a hypothetical S&P 500 options order through a broker intermediary. The analysis focuses on those options that expire within 3 months and that fall within predefined at-the-money (ATM) and out-of-the-money (OTM) ranges. Four scenarios are considered based on type (puts and calls) and relative moneyness1. The report assumes an order size of approximately $50mm vega notional2 and uses 2018 full-year transactional data3 provided by an independent 3rd party data vendor4.

Transaction Costs

Transaction costs are expenses incurred in the opening and closing of the position.

Explicit Costs: These include the commission, or fee, charged by the broker for completing the order as well as fees levied by the exchange and clearinghouse. Table 1 in the Appendix provides a general comparison of explicit costs for end customers/non-CME exchange members5. This report does not focus on explicit costs given these fees are not too dissimilar between both products. Instead, the analysis focuses on implicit costs given those are the more meaningful differences.

Implicit Costs: Market impact6 is a measurement of execution quality that reflects the adverse price movement caused by the act of executing the order. In the simplest sense, market impact can be defined as the volume-weighted bid-ask spread differential for executing a given order. The following scenarios show that, on average, ES options offer more cost-effective execution relative to SPX options by 0.04 to 0.15 index points. This corresponds to between ~$960 to ~$2,550 in cost savings7 on the $50mm vega notional order, which equates to approximately $4 to $15 per contract in cost savings using ES options in lieu of SPX options.

Scenario Analysis

The following scenarios summarize the relative execution advantages, on average, for the $50mm vega notional order and the corresponding dollar savings per contract.

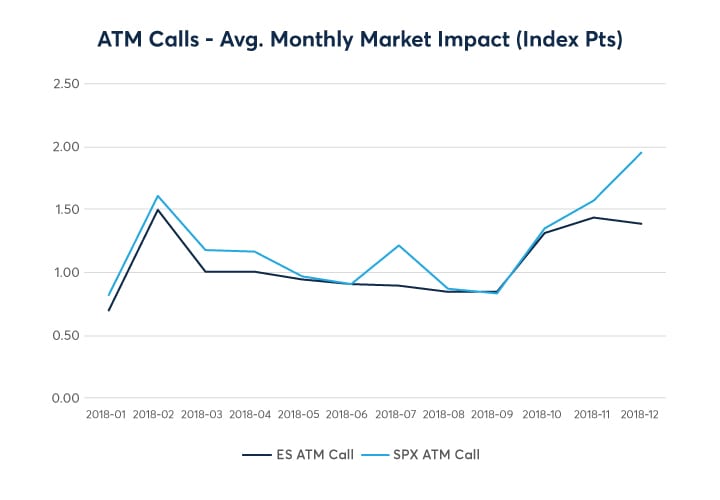

Scenario 1: ATM Call Options

ES options offered superior execution by 0.11 index points, or ~$11 per contract in cost savings.

| ES | SPX | Diff (Index Pts) | Diff $ |

| 1.07 | 1.18 | 0.11 | $1,909 |

{kind=link}

Source: OneMarketData

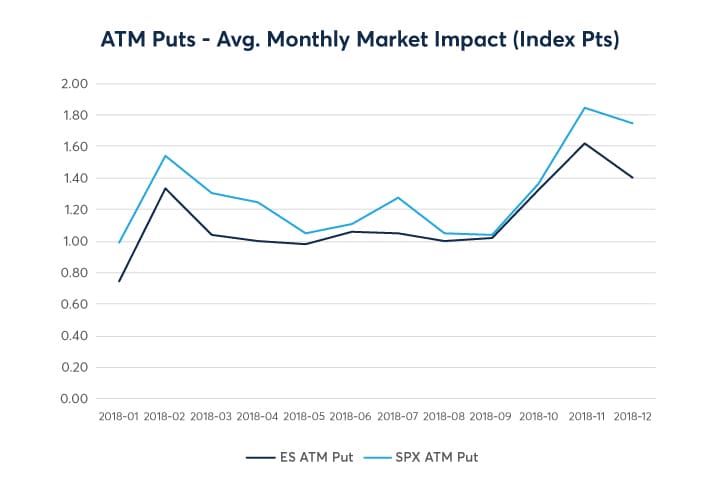

Scenario 2: ATM Put Options

ES options offered superior execution by 0.15 index points, or ~$15 per contract in cost savings.

| ES | SPX | Diff (Index Pts) | Diff $ |

| 1.14 | 1.28 | 0.15 | $2,551 |

{kind=link}

Source: OneMarketData

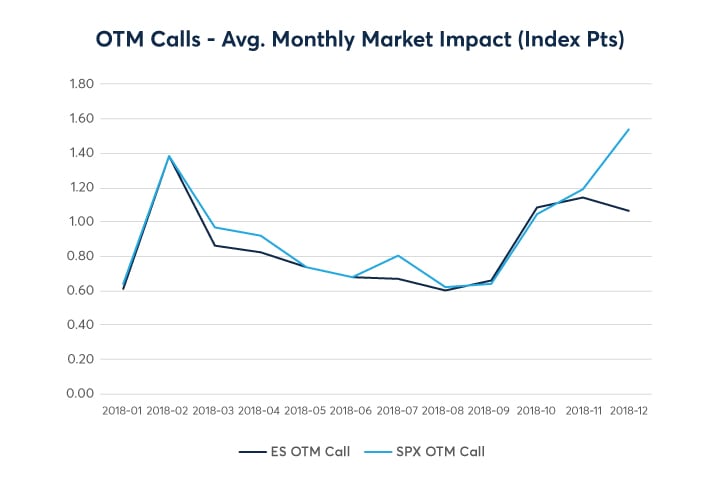

Scenario 3: OTM Call Options

ES options offered superior execution by 0.04 index points, or ~$4 per contract in cost savings.

| ES | SPX | Diff (Index Pts) | Diff $ | |

| 0.87 | 0.91 | 0.04 | $964 |

{kind=link}

Source: OneMarketData

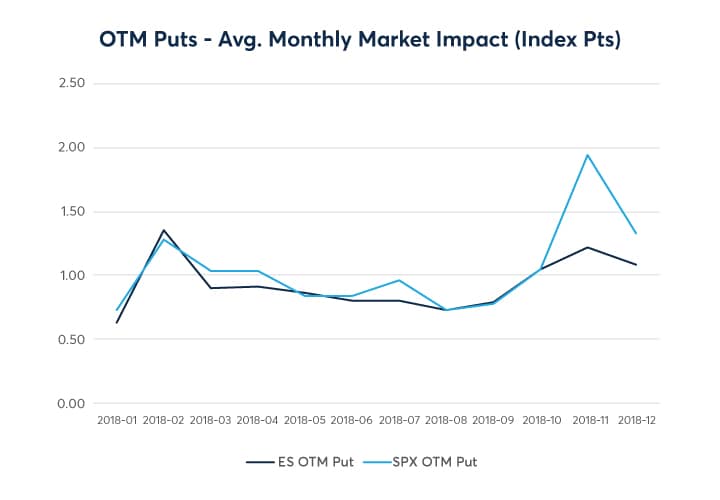

Scenario 4: OTM Put Options

ES options offered superior execution by 0.11 index points, or ~$11 per contract in cost savings.

| ES | SPX | Diff (Index Pts) | Diff $ |

| 0.93 | 1.04 | 0.11 | $2,511 |

{kind=link}

Source: OneMarketData

Other Considerations

While this analysis has focused on execution quality, there are other factors to consider when evaluating the multitude of S&P 500-related options products. Here are a few additional considerations when looking at using ES and SPX options.

Around-the-clock liquidity

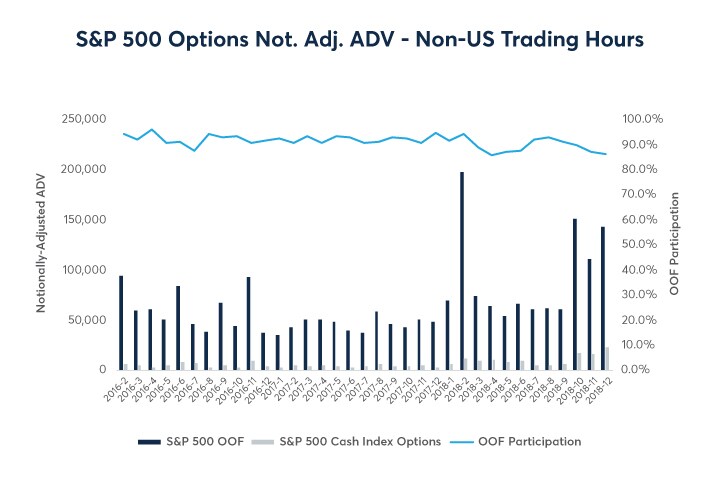

ES options offer liquidity for nearly 24 hours of the day. Looking only at ES and SPX options, over 90% of average daily volume8 during non-U.S. regular trading hours occurs in ES options. Around-the-clock liquidity in ES options can allow investors to manage their risk and prepare for market fluctuations around-the-clock. The chart below compares S&P options on futures (OOF) and S&P cash index options ADV outside of regular U.S. trading hours.

{kind=link}

Source: OneMarketData

Capital Commitment

Those investors who prefer to source liquidity outside of the central limit orderbook can take advantage of CME’s Options on Standard S&P 500 Index futures (SP)9, which offer 100% guaranteed capital commitment in a listed product. Meaning, 100% of the trade can be privately negotiated and consummated either as a delta-neutral or outright SP options block trade10. Because the covered SP options block trade is bilateral with no need to expose the trade to the pit, participants do not face break-up risk. Conversely, SPX options crosses must be shown to the pit, which carries the risk of the trade being broken up.

Conclusion

ES options offer superior execution of between 0.04 to 0.15 index points, on average, relative to SPX options. This translates to cost savings of $4 to $15 per contract. Figure 1 summarizes the results of this analysis. Investors are reminded that the results in this analysis are based on the stated assumptions and historical data. The actual costs incurred by an investor will depend on the specific circumstances of both the investor and the particular trade scenario including the instrument, option type (put/call), order size, maturity, broker fees, execution methodology, time of execution, and general market conditions, among other factors. Investors should always perform their own analysis.

Figure 1

| ES | SPX | ES Advantage | |

| ATM CALL | 1.07 | 1.18 | 0.11 |

| ATM PUT | 1.14 | 1.28 | 0.15 |

| OTM CALL | 0.87 | 0.91 | 0.04 |

| OTM PUT | 0.93 | 1.04 | 0.11 |

Source: OneMarketData

Appendix

Table 1: Customer/Non-Liquidity Provider Fee Comparison

| Order Size (Vega Notional): $50mm | ||||||||||||||||

| S&P 500 Index: 2,750 | ||||||||||||||||

| Moneyness/ Contract |

Contracts | Exchange Fee | Execution Surcharge Fee |

Floor Broker Fee |

Customer Priority Surcharge |

OCC Fee | Fee Per Contract | Total Cost |

||||||||

| ATM SPX | 175 | 0.44 | 0 – 0.21 | 0.42 | 0 – 0.10 | 0.05 | 0.91 – 1.22 | $159 – $214 | ||||||||

| ATM ES | 350 | 0.35 – 0.55 | 0 | 0 | 0 | 0 | 0.35 – 0.55 | $123 – $193 | ||||||||

| OTM SPX | 230 | 0.35 | 0 – 0.21 | 0.42 | 0 – 0.10 | 0.05 | 0.82 – 1.22 | $189 – $260 | ||||||||

| OTM ES | 460 | 0.35 – 0.55 | 0 | 0 | 0 | 0 | 0.35 – 0.55 | $161 – $253 | ||||||||

Source: OneMarketData

Notes

- Exchange fees

SPX fees based on 2 tiers: premiums< $1 fee is $0.35 and >$1 is $0.44.

SPX customer transaction fees will only be charged up to the first 20,000 contracts per order.

ES fee range of $0.35 – $0.55 depending on CME membership - Execution Surcharge

SPX Execution Surcharge of $0.21 applies to all electronic executions - Floor Broker Fee

Indicative of “middle-of-the-range” pricing for institutional clients. - Customer Priority Surcharge

Surcharge of $0.10 applies to SPX Weekly Options executed electronically

More About OneMarketData

OneMarketData is a leading provider of solutions and data for the financial industry. OneTick is a comprehensive suite for time-series data management, real-time and historical analytical tools to address the most demanding requirements. Proprietary traders, hedge funds, asset managers and investment banks can leverage the built-in capabilities of OneTick for order book and liquidity analysis, quantitative research, transaction cost analysis, surveillance and backtesting. Built by Wall Street experts, the OneTick suite of products is an enterprise-wide tick data capture and storage solution offering analytical modelling tools, global history across equities and futures markets and reference data. In 2015, OneMarketData acquired Tick Data, LLC, the first and leading provider of historical intraday market data, to marry the industry’s most powerful analytics platform with the cleanest, most reliable historical intraday data available. More information about OneMarketData is available at www.onetick.com.

References

[1] The report defines ATM options as those with a 45-55 delta, and OTM options as those with 30-45 delta.

[2] Using the average daily closing S&P 500 level of 2,746.21 for 2018 full-year, $50mm vega notional equates to approximately:

ATM: 350 ES contracts, 175 SPX contracts

OTM: 460 ES contracts, 230 SPX contracts

[3] The report uses transactional data during the most liquid time period: regular U.S. trading hours, which are defined as 8:30am – 3:00pm CT.

[4] Source: 3rd party vendor OneMarketData

[5] Differences may vary based on broker-client relationship as well as exchange fee changes and rebate schemes.

[6] For this analysis, market impact is calculated for every 15-minute window during U.S. trading hours (8:30am – 3:00pm CT), and a per-day average is computed for each product (SPX and ES).

[7] Market impact in dollar terms is calculated as the difference between: (the number of SPX contracts x $100 multiplier x SPX market impact in index points) and (the number of ES contracts x $50 multiplier x ES market impact in index points).

[8] Because SPX’s multiplier is twice as larger as ES’, SPX volume is notionally-adjusted to ES-equivalent (i.e. SPX volume doubled) to allow for an appropriate comparison.

[9] SP options are primarily traded on CME’s trading floor and are 5x the notional of ES options.

[10] Block trades are privately negotiated futures, option trades or combination transactions, pursuant to Rule 526, that are permitted to be executed between two eligible counterparties -which are subsequently submitted to CME Clearing through CME Direct. Block trade have required minimum sizes. More information about block trade minimum thresholds can be found here.

Equity Index Options on Futures

CME Equity Index Options on Futures provide around-the-clock liquidity and extensive product choice on benchmark indices.