{kind=link}

Wheat: Will High Inventory Further Dent Prices?

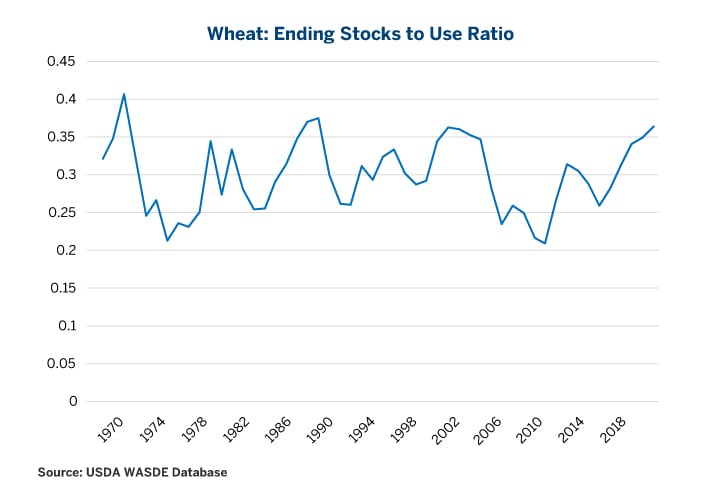

Chicago Board of Trade soft red winter wheat prices began a long-term bear market over five years ago in July 2012. Since then, prices have fallen by more than 50%. The good news for wheat growers is that while prices are depressed by 2007-2017 standards, at $4.30 per bushel, they remain higher than levels between 1997 and 2006 when prices fell below $3.00 per bushel (Figure 1). What concerns many wheat growers, however, is the level of inventory. Ending-stocks-to-use ratios have rarely been so high (Figure 2). Will the level of inventories further pressure prices and send wheat below $4.00, or even $3.00 per bushel?

Figure 1: Wheat Prices Haven’t Been Consistently Lower Since 2006.

{kind=link}

Figure 2: Ending-Stocks-to-Use Ratio Shows Near-Record Inventory.

{kind=link}

The good news for farmers is that while the level of ending-stocks-to-use ratio has a reasonably strong inverse relationship with the inflation-adjusted level of prices, it has almost no bearing on future price performance. Generally, constant dollar wheat prices are higher in years during which ending-stocks-to-use-ratios are low and vice versa (like 2017) (Figure 3). In order words, high levels of wheat held in inventory explain why prices are already depressed.

Figure 3: High Ending-Stocks-To-Use Ratios Correlate with Lower Constant Dollar Prices.

{kind=link}

That said, the relationship between the level of ending-stocks-to-use ratio and subsequent price changes is pretty close to neutral (Figure 4). High level of ending stocks don’t necessarily further depress prices and low levels of ending stocks don’t always cause bull markets. This makes sense in an efficient market. Information regarding inventories is quickly incorporated into prices and one cannot gain an advantage by trading off of it subsequently. That said, there is still one relationship that jumps out regarding the impact of ending stocks: when inventory levels are high, price volatility tends to be low and when inventories are low price, volatility tends to be high. This makes sense in that, if demand for wheat rises in a high-inventory environment, it can be met quickly by liquidating inventories. Prices don’t have to soar to incentivize additional production the next season as might be the case in a low- inventory environment. This helps to explain the lack of volatility in wheat options, which currently demonstrate a remarkable lack of worry about the future. Watch out, one bad harvest and inventory levels could fall, sending both prices and volatility higher.

Figure 4: High Ending-Stocks-To-Use Ratios Often Equates to Low Realized Volatility.

{kind=link}

Figure 5: Wheat Options are Trading Near the Lower End of their Recent Range.

{kind=link}

Bottom line

- After many years of decent harvests and growing inventories, wheat prices are at decade-long lows.

- High ending-stock-to-use ratios have little bearing on whether future price movements will be up or down.

- High inventories do, however, tend to dampen volatility.

- One bad harvest and inventories could fall, sending prices and volatility much higher.

Recommended For You

Wheat

Prices have taken a beating, dropping more than 50% over the past five years on the back of large inventories. Will the high stocks-to-use ratio continue to pressure the market or is the worst over? Hedge against volatility at the largest marketplace for grains using CME Group products.