{kind=link}

UK: What to Expect from a Prime Minister Corbyn

Since losing its parliamentary majority in June 2017, British Prime Minister Theresa May’s Conservative Party has been hanging by a thread, propped up by coalition partner, the Democratic Unionist Party (DUP) of Northern Ireland. Even under the best of circumstances, keeping the coalition’s grip on power was a difficult task. For starters, the government must negotiate Brexit, which was already complicated without the DUP advocating special arrangements for Ireland. Making matters worse, European Union (EU) leaders told Britain “to go back and try harder,” saying that Brexit negotiations haven’t advanced far enough on issues such as the status of EU citizens living in Britain and the payment Britain will make to Brussels when it leaves the EU and Northern Ireland to advance the discussions to Britain’s future commercial relationship with Europe or a post-Brexit transition period. While there is some hope that Britain will soon agree to a £60 billion divorce fee, the negotiations haven’t gotten past square one.

Adding to May’s woes is tabloid-worthy discord within her cabinet. Andrea Leadsom, the Leader of the House of Commons, denounced Michael Fallon, the Defense Secretary, for making “derogatory comments of a sexual nature” towards her, prompting his resignation. This dispute triggered an eruption of unrelated allegations of inappropriate conduct within parliament. While these controversies touch all major parties, the government is taking the brunt of it.

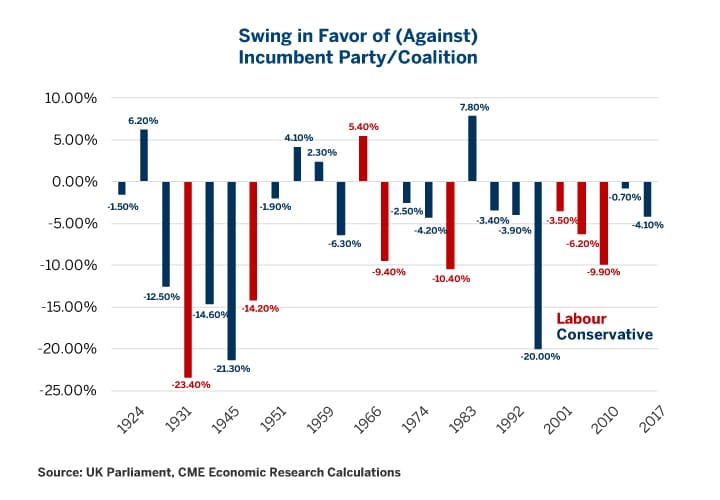

Given the fragility of the current government, markets should probably be thinking carefully about the next Prime Minister and the potential impact on the U.K. economy and currency. In fact, even if things in Westminster were going swimmingly (which they aren’t), markets should probably be looking to the next elections anyway. As is the case in democracies, U.K. voters have a way of turning against incumbents. In the past century, there have been 26 general elections. In those 26 elections, the incumbent party or coalition of parties expanded their popular vote margin in only five of them and lost support in the other 21, including each of the past eight elections (Figure 1).

Figure 1: Gaining Power is Easier than Keeping It.

{kind=link}

On average, the incumbent party has lost about 6% of the votes with respect to the opposition, something that the Tories can ill afford given that they won the June 2017 elections with a plurality of only 2.4%. The Labour Party has moved into a small but consistent polling lead since the June election. When new elections take place, they could easily produce a Labour majority or a hung Parliament in which no party commands a majority. What is difficult to know is the timing of any such elections. They don’t have to take place until 2022, but if the Conservatives lose by-elections as members of Parliament resign, the election could be hastened. All of this is good news for Jeremy Corbyn, the leader of the Labour Party who stands to become Prime Minister should his party wins the next election.

Not New Labour

In 2002, a dozen years after she left office, Margaret Thatcher said that her proudest accomplishment was New Labour and Tony Blair – that she had forced her opponents to change their minds and embrace free market economics. Under Prime Minister Blair, budget deficits were negligible, income tax rates stable, government spending grew at a moderate pace, regulation had a light touch and the pound was reasonably strong. That was then. Labour’s current leader Corbyn rebelled against Blair and his successor, Gordon Brown, more than any other Labour MP in party-line votes in the 1997-2001, 2001-2005 and 2005-2010 Parliaments. Corbyn advocates increasing income taxes and authorizing the Bank of England to directly finance infrastructure spending rather than buying bonds during quantitative easing and vastly expanding public spending, especially on education. The merits of these policies aside, none of them are likely to support the pound.

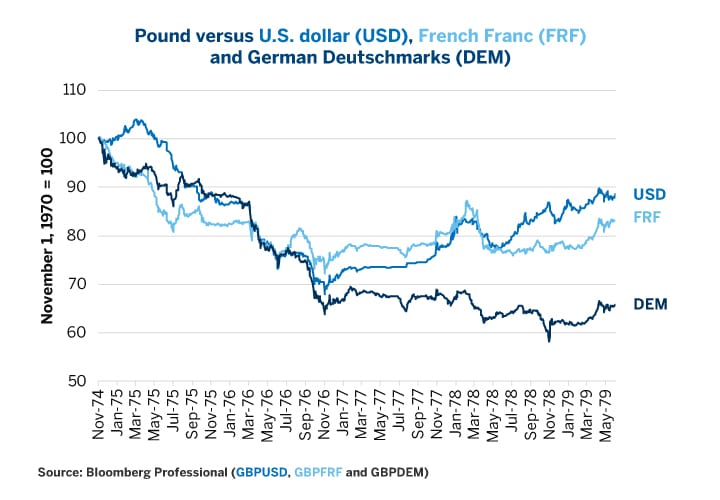

To find an analogous set of policies, one has to look back to the Labour government of Harold Wilson (1974-76) and James Callaghan (1976-79). Wilson began his term in office by increasing the tax rate on personal income from 75% to 83% and the rate on “unearned income” from 90% to 98% while intervening to control wages and prices. Between November 1974 and November 1976, the pound plunged 31% versus the U.S. dollar, fell 27% versus the French franc and tumbled 37% versus the German deutsche mark. It remained weak against the franc and deutsche mark through the end of the 1974-79 Labour government (Figure 2). To be fair, the pound continued to fall versus the dollar and the deutsche mark (but not the franc) during the 18 years of Tory government from 1979-1997, albeit at only a fraction of its 1974-79 pace of decline. Moreover, the U.K. economy in the 1970s was very different from what it is today: notably, the Bank of England had trouble controlling inflation then, and has trouble generating it now.

Figure 2: Old Labour and the Pound.

{kind=link}

The Brexit-Corbyn Nexus

Although Brexit had supporters across the political spectrum, it got more support on the political right than on the left. This is evident in recent polling such as YouGov’s October 23-24, 2017, poll which shows Conservative Party voters supporting Brexit by a 69%-31% margin, whereas Labour voters wish to remain in the E.U. by a 67%-33% margin.

One the key arguments in favor of Brexit on the part of its Conservative supporters was that it would allow the U.K. to become more like Switzerland, with low taxes and light-touch regulation. Not happening, if Corbyn wins. In the event that the U.K. takes a ‘hard’ Brexit followed by a Labour victory, it could see Britain transform into a more socialist, centrally-controlled economy – just one that happens to be outside of the E.U. This is the nightmare scenario for the pound. Since late September, it has fallen by 4.5% versus the dollar and fallen slightly versus the euro as May’s position weakened and the Brexit talks stalled. If events spiral beyond May’s control and the Brexit talks are further paralyzed, this should intensify the downward pressure on the sterling.

There are, of course, other scenarios. One possibility is that the Tory government collapses and Labour comes to power prior to March 2019 when the Brexit negotiations are meant to conclude. Changing negotiators mid-course could also be bearish for the pound in the short term but, if for some reason Brexit doesn’t happen, the pound could easily snap back to 1.50 versus the dollar and 1.25 versus the euro from its current levels close to 1.30 and 1.13, respectively. Some strategically minded Tories might even want to foist the Brexit negotiations on Labour and then benefit from any deterioration in Labour’s popularity once Corbyn is in power. At any rate, it would be easier for the Conservatives to deal with their internal divisions if they were out of power rather than when they are running the country. After all, most Tory parliamentarians supported the ‘Remain’ camp whereas most rank and file Tory voters favored leaving the E.U.

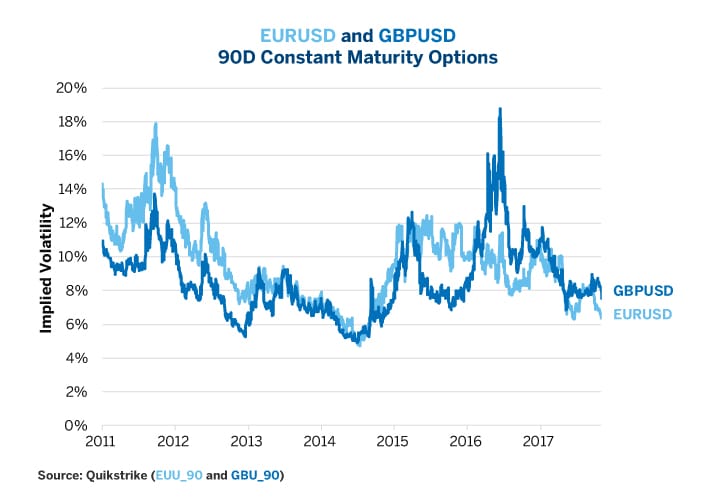

Given the potential for volatility, it’s curious how complacent options market are. Implied volatility on 90-day pound-dollar (GBPUSD) options traded recently as low as 7.5%. To be fair, it’s not the lowest ever. In the past, it has fallen as low as 5% implied volatility but it’s much closer to the lower end of its volatility range than the higher end, which is around 19% (Figure 3).

Figure 3: Westminster & Brexit Negotiations Might be Melting Down but Options Traders Don’t Care.

{kind=link}

Bottom Line

- Theresa May’s situation continues to deteriorate.

- The Tories risk losing by-elections, reducing their already slender margin of control.

- Brexit negotiations are not going well, with the E.U. refusing to advance past the initial set of issues to even more difficult areas.

- The likelihood of another U.K. general election is growing.

- A Labour victory could bring higher taxes and more inflationary policies that could weaken the pound.

- Markets, especially for options, may be too complacent given the political risks.

Recommended For You

British Pound

British Prime Minister Theresa May's grip on power seems tenuous after her Conservative Party's lackluster performance in the last election. The pound could be in play if opposition leader Jeremy Corbyn's Labour Party wins the next election. Hedge against the uncertainty at the world's largest regulated FX market place with CME Group futures and options.