https://www.cmegroup.com/content/dam/cmegroup/images/common/default/article-brightcove-1440x500.jpg

{kind=link}

Gold: Will Prices Dip If Fed Hikes Rates?

Gold: Will Price Dip Below $1,000 If Fed Hikes Rates?

https://www.cmegroup.com/education/images/articles/bnr-erik-norland.jpg

{kind=link}

Five Factors that Could Drive Gold and Silver…Lower or Higher

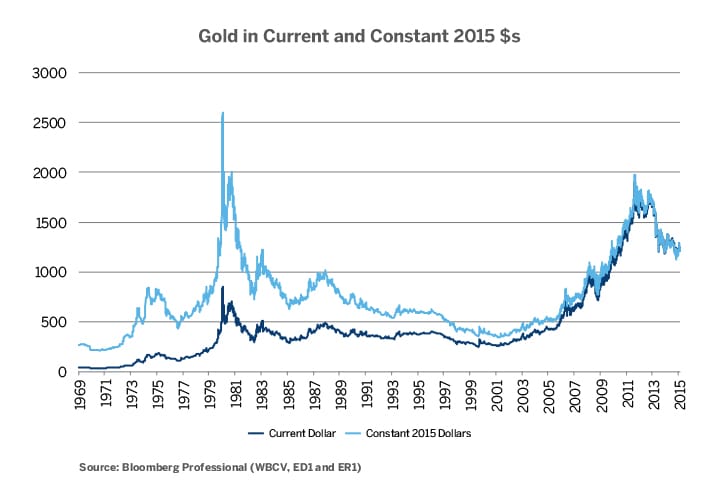

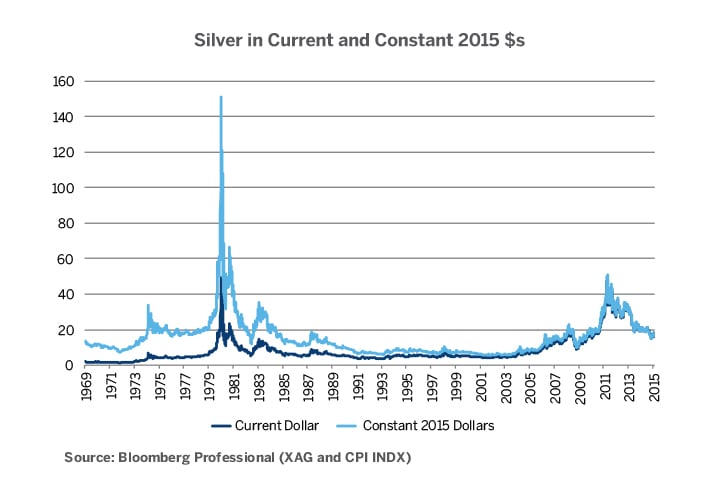

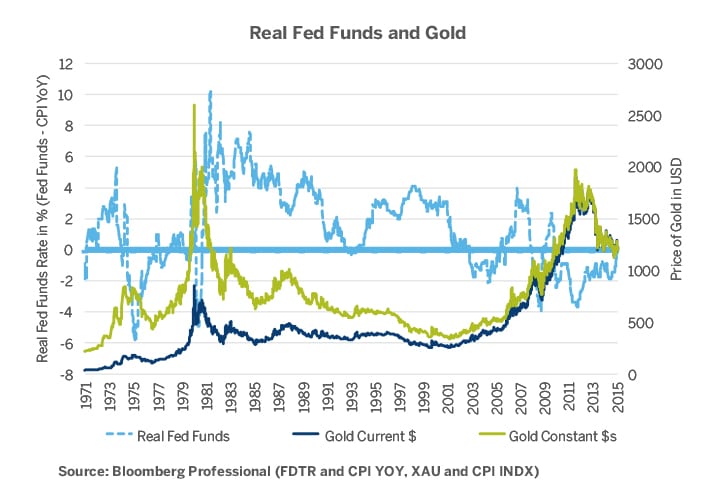

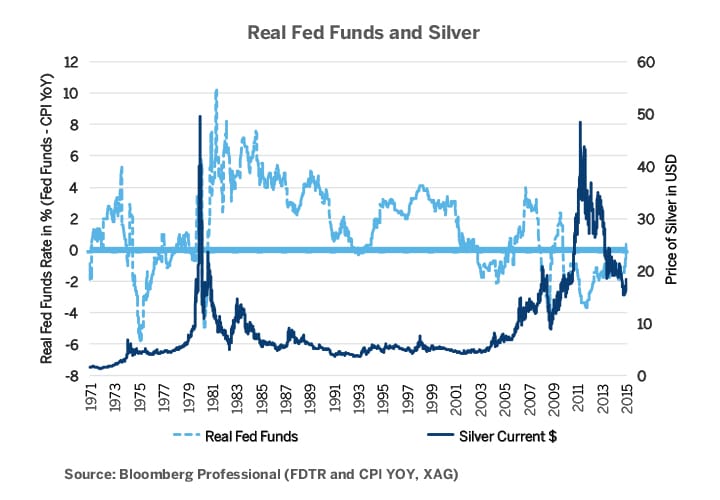

Gold and silver prices have fallen considerably from their 2011 highs. Silver peaked at nearly $50 per ounce and now trades below $20. Gold topped out at about $1,900 an ounce and is currently close to $1,200. Both metals are not only trading far below their peaks, but also their inflation-adjusted highs set in 1980 (Figures 1 and 2). This gives a sense of the scale of their downside and upside potential.

At least five factors may have contributed to their decline:

- The steady recovery of the US economy has allowed the US Federal Reserve to end quantitative easing and begin considering rate hikes, possibly as soon as June.

- The European Central Bank (ECB) has succeeded in containing the European debt crisis (at least excluding Greece) by promising to act as a buyer of last resort of the debt of Italy, Spain and other financially-challenged Eurozone countries, vastly reducing intra-European spreads.

- The value of the US Dollar (USD), the currency of choice in the global commodities trade including gold and silver, has soared versus other currencies.

- The prices of many other commodities including industrial metals, crude oil, natural gas and agricultural goods, have fallen in USD terms.

- The crisis in the Middle East has not spread, at the moment, to the largest oil producing nations in the Persian Gulf.

Let’s look at how gold and silver prices might trend based on these possible drivers of market returns.

Figure 1.

{kind=link}

Figure 2.

{kind=link}

US Monetary Policy

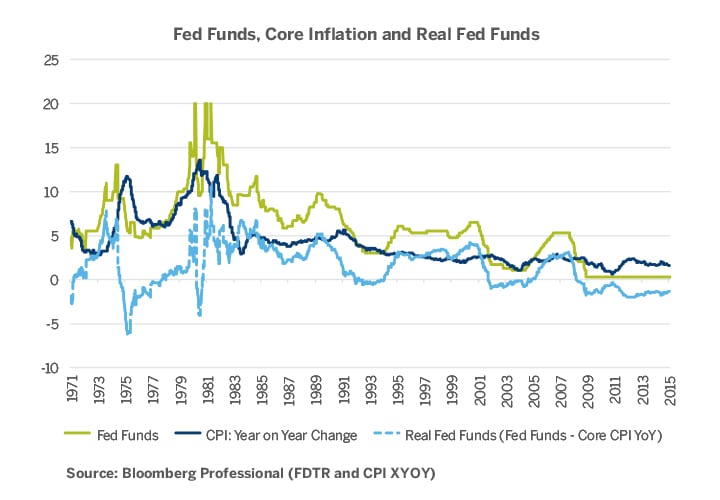

Since 2009, the Fed has found itself in the unusual position of holding its policy rate (Fed Funds) below the rate of core inflation. This is something that has only occurred on a few occasions (Figure 3).

- 1969-1970: Rates were lowered to fight a mild recession. The Nixon Administration attempted to contain inflation afterwards with wage and price controls.

- 1974-1977: When the Fed mistakenly thought that inflation from the first oil crisis would be temporary. This resulted in a massive run up in inflation from 1977-1980 that was reined in by soaring interest rates and a deep recession.

- Brief periods of slightly negative real rates in 1992-1993 and 2001-2004 when the economy was healing from recession.

Figure 3.

{kind=link}

Figure 4.

{kind=link}

When the Fed holds Fed Funds below the rate of headline inflation, there is a tendency for gold and silver prices to soar (Figures 5 and 6):

Figure 5.

{kind=link}

Figure 6.

{kind=link}

The tendency appears to last until the market begins to anticipate that the Fed will hike rates or tighten policy (by ending quantitative easing, for example).

It is our view that the Fed is likely to begin tightening policy in 2015 for a variety of reasons:

- A strong recovery in the labor market, with average hourly earnings up by 2.0% year- over-year and average hours worked increasing 0.6%. This makes for a 2.6% gain in average earnings, comparing February 2015 to February 2014 – quite respectable given the low rate of inflation.

- The number of people working rose by 2.4% between February 2014 and February 2015. This brings the increase in total labor income to 5.0% (2.4% more people working + 2.6% increase in average wages). This should make for robust consumer spending.

- The Fed sees the recent energy-related dip in inflation as being temporary.

- Other areas of the economy appear to be robust, including corporate profits near a record high and the housing market continuing to recover slowly.

As such, we would not be surprised if the Fed increases rates as soon as this June. Fed Funds futures reflect a rate hike by September and a second one by January 2016 – with the possibility that such rate moves could come sooner.

If the Fed does raise rates as expected, it could pressure gold and silver prices. As such, we would not exclude the possibility of gold dipping below $1,000 per ounce into the triple digits, and silver making a run for below $10 per ounce.

There are risks to this forecast, however. Equity markets have been trading at valuations that look reasonable so long as corporate earnings hold up. If corporate earnings begin to decline in 2015, however, there is a real possibility that the equity market could have its first major correction since 2011. Two previous Fed chairmen, Alan Greenspan and Ben Bernanke, were known for lowering interest rates (or ramping up quantitative easing) in the face of equity market weakness – dubbed the Greenspan and Bernanke puts. Will there be a put by current Fed Chair Janet Yellen as well? We don’t know, but it’s hard to imagine that she and the FOMC would risk exacerbating market volatility by hiking rates in the middle of a steep downturn in stocks. As such, if an equity market correction happens, to the extent that it delays Fed rate hikes, it might give at least a temporary boost to gold and silver prices.

Bottom line, we think that US monetary policy holds more downside risks than upside potential for precious metals in 2015, but if the Fed delays rate hikes for any reason, it could be good for gold and silver.

Europe

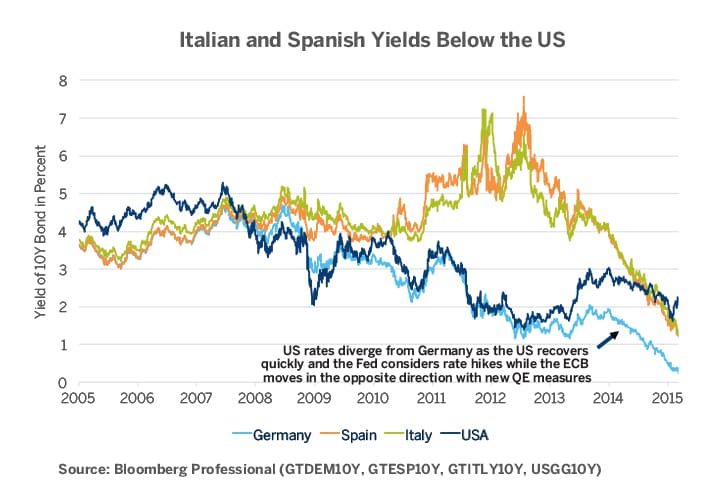

While gold is denominated in US Dollars and therefore responds more strongly to changes in the Fed’s monetary policy than it does to actions by other central banks, the US isn’t the only game in town. On the other side of the Atlantic, it appears that the ECB’s gambit of promising to buy the debt of Italy, Spain and other financially-challenged Eurozone nations as a last resort has paid off. That promise, along with the announcement of a massive quantitative easing program, has pushed German yields close to zero, while Italian and Spanish yields have fallen below the yields on US Treasuries (Figure 7).

Figure 7.

{kind=link}

The easing of tensions in the Eurozone has been generally bad news for gold and silver. It eliminated the possibility of any imminent Eurozone break up to the disappointment of gold bugs who see the yellow metal as a store of value in times of inflation and uncertainty.

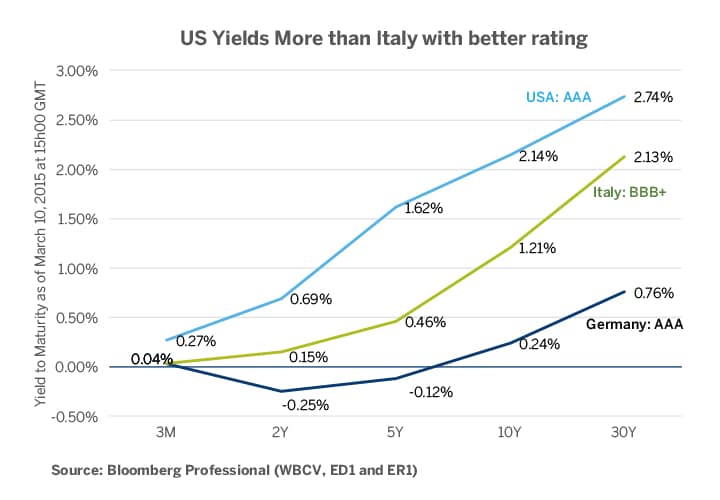

The good news for investors in precious metals is that the process of calming the European rate markets is probably nearing an end. Simply put, rates might not be able to fall much further. German yields are already negative, below the six year point on the curve, and BBB+ rated Italian debt and BBB rated Spanish debt pay less than AAA (composite) rated debt in the United States. Once the ECB begins its buying program, there is a risk that rates might back up a bit. This won’t necessarily help gold and silver but the harm to gold and silver long position holders from the calming of the situation in Europe over the past few years is almost certainly over.

Greece is the one exception. Its yields are still above 9% and Greece’s possible exit from the Eurozone monetary union, dubbed Grexit, could still happen later this year or in 2016. Even so, the impact of Greece’s withdrawal should be minor -- Europeans have already ring-fenced most of their private sector exposure to Greece, which constitutes less than 2% of the Eurozone economy.

Bottom line: We see Eurozone events as a net neutral for gold and silver going forward.

Figure 8.

{kind=link}

US Dollar

USD has soared against most other currencies in the past year for several reasons:

- US economy is strengthening, as evidenced by a broad range of indicators.

- That strength has allowed the Fed to end quantitative easing and has enabled the bank to seriously consider rate hikes in 2015.

- Monetary policy is heading in the opposite direction in many other countries and regions, including the Eurozone where the ECB is embarking on a quantitative easing program: Japan, where the Bank of Japan continues to ease policy; and Australia and Canada where central banks have cut rates.

- Commodity prices have collapsed, taking a diverse range of emerging market currencies down with them.

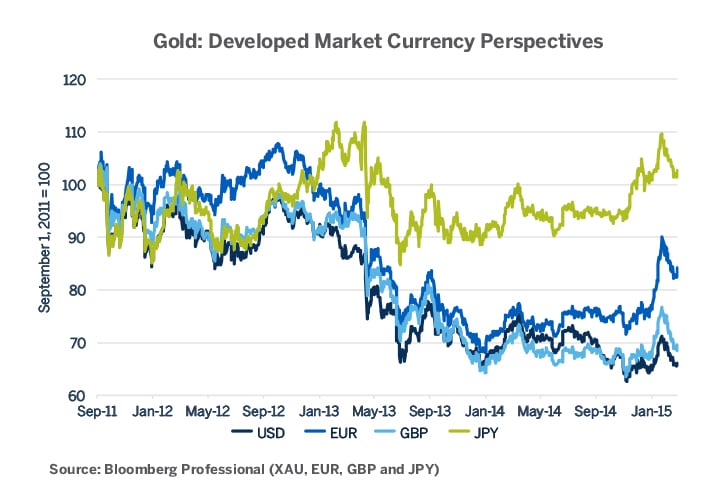

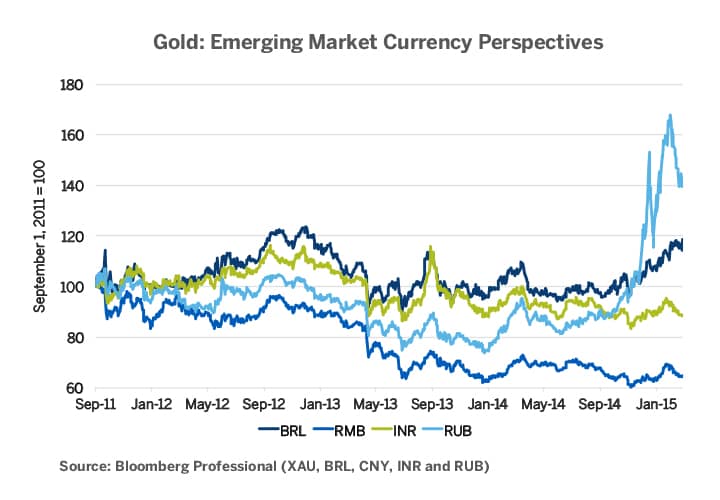

Whether the current strength in the US Dollar will continue or not is difficult to say. Nevertheless, if it does keep its uptrend, it will likely put pressure on gold prices in USD terms but not necessarily from the perspective of buyers using other currencies (Figures 9 and 10).

Figure 9.

{kind=link}

Figure 10.

{kind=link}

Gold prices have fallen sharply since their September 2011 peaks in USD terms and from the perspective of other relatively strong currencies such as the British Pound (GDP) and Renminbi (RMB), but not from the perspective of weaker currencies such as Japanese Yen (JPY) or Russian Ruble (RUB) (Figures 9 & 10).

This is a double-edged sword for gold and silver. On the one hand, from the standpoint of a buyer in India, Japan or Russia, gold has held its value from the perspective of their currency, which is desirable. On the other hand, from their vantage point, it has become more expensive to buy which could curtail their ability and willingness to purchase more of it in the future.

Overall, the US Dollar rally might have some life left and if USD continues to power higher, it will be bad for gold. Any upside surprises on economic growth outside of the US or any downside shocks in the US could hurt the Dollar, however, and could boost the price of precious metals.

Other Commodities

Our base case view is that crude oil prices are unlikely to rebound towards $100 per barrel any time soon and that the most likely scenario is that prices could remain in a wide trading range from perhaps $30-$70 per barrel for the rest of 2015 and maybe even into 2016 and 2017. Most oil producers, whether they are indebted private sector companies or state entities serving government interests, are simply not in a position to cut back their current production which would result in a loss of revenue.

For the moment, Saudi Arabia does not appear to be in the mood to cut back production. For the Saudis, lower oil prices are like killing several birds with one stone. Lower prices reduce investment in fracking in the US and elsewhere, which could boost prices several years down the road, although having little impact on current production. Lower prices also hinder Iran and Russia with which Saudi Arabia has contentious relations, and limit revenues of the Islamic State militant group.

Industrial metals such as copper and aluminum have also weakened considerably. This appears to be related to slowing growth in China. We don’t see a change in this in 2015 and, in fact, expect China’s pace of growth to continue to moderate.

Food prices are the hardest of all to predict since they are only modestly influenced by macroeconomic conditions and are subject to other forces such as weather.

Geopolitics

To the extent that the collapse in commodity prices can create political instability, notably in major oil producing nations, it could have upside benefits for gold and silver. Otherwise, we see the likelihood of continued low prices for other commodities in 2015 and 2016 as likely weighing on precious metals.

(Please see our paper Oil Collapse: Winner and Losers, The Geopolitical and Economic Consequences of Lower Oil Prices).

Overall, we see downside risks to gold and silver outweighing upside risks in 2015. That said, we think that the key upside risks to watch for are:

- A US equity correction or slowdown in the US economy that causes the Fed to delay rate hikes or, in an extreme case, even to ease further.

- Geopolitical instability, especially in the Middle East or other key oil producing nations.

- A drop in the US Dollar.

- Renewed questions about the viability of the Eurozone.

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.