{kind=link}

Equities: Driven by Trump or Macroeconomics?

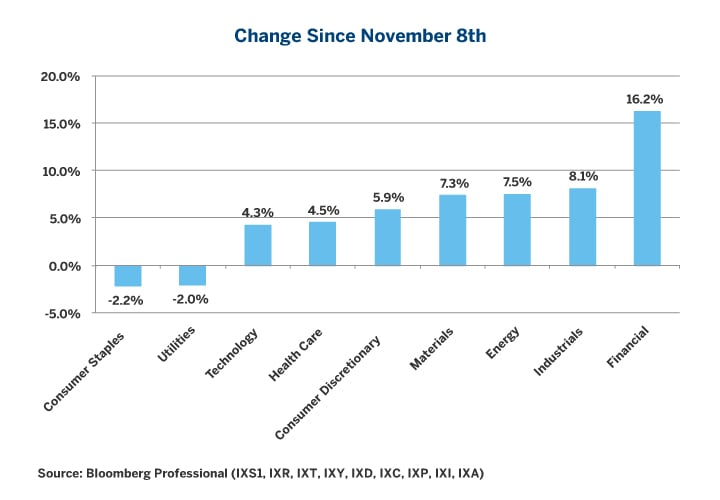

Since Election Day on Nov. 8, stocks have been on a tear. However, not all sectors have performed equally well. The best performers have been the financial, energy, industrial, and materials sectors. Others, notably utilities and consumer staples, have lagged (Figure 1).

The powerful post-election sector rotation has given rise to the notion that highly-regulated industries have outperformed, perhaps in part, because markets anticipate a lighter regulatory touch by the incoming administration that will benefit them. While this narrative may contain some truth, our research indicates that it is far from being a complete explanation.

Figure 1: Highly-Regulated Sectors Have Outperformed Post Election but was Regulation the Reason?

{kind=link}

Rather, macroeconomic factors along the lines of those that we laid out in our paper “Four Key Drivers of Equity Sector Performance” [link-bold] have been driving equity sector relative performance. In that paper, we demonstrated that factors such as movements in short-term interest rate expectations, the U.S. dollar, and the prices of crude oil and copper explain much of the over/underperformance of the various E-Mini S&P sector futures versus the S&P 500® Index. All of these factors have been in play since Election Day and collectively they do an excellent job of explaining the relative performance of the various S&P 500® subsectors versus the index itself.

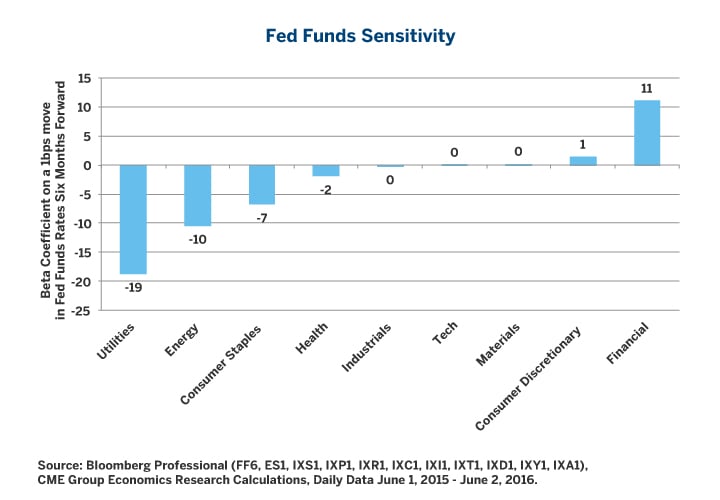

For example, why have financial shares rallied? The reasons mostly come down to increased expectations of interest rate hikes by the Federal Reserve (Fed) in 2017 and beyond since Nov. 8. Financial shares tend to benefit relative to the S&P 500® as a whole when expectations for Fed rate hikes strengthen (Figure 2). By contrast, rising rates are bad news for utility, energy, and consumer staples.

After the election, expectations for further Fed rate hikes have soared (Figure 3). Some of this may be due to anticipation that President-elect Donald Trump will stimulate faster economic growth through a loosening of fiscal policy (tax cuts, spending increases and bigger budget deficits). Some of it may have happened in due course even if the election outcome had been different. Long-dormant inflation is beginning to rise and labor markets are tightening as the seven-year-old economic expansion continues.

Figure 2: Rising Rate Expectations Are Generally Good News for Financial Shares.

{kind=link}

Figure 3: Expectations for Fed Rate Hikes Soared Post-Election.

{kind=link}

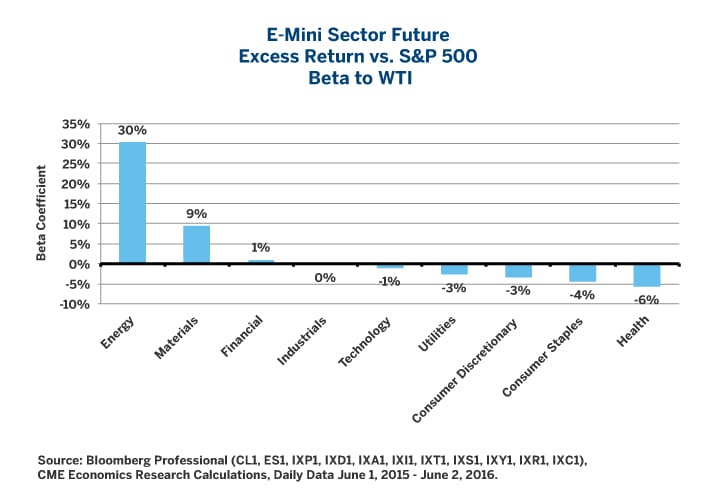

Increased rate-hike expectations have probably played a key role in the outperformance of financial services stocks like those included in the S&P Financial Sector Index. But if that’s the case, why did energy stocks also outperform? Usually, investors in highly-leveraged energy stocks take the news of higher interest rates rather badly. In this case, the bad news of higher rates for energy stocks was more than offset by the good news of higher prices for West Texas Intermediate crude oil. Energy stocks tend to do well when oil prices rise (Figure 4) and oil prices are up 16% since the election.

Figure 4: Energy, Materials and Financial Stocks Tend to Benefit from Higher Oil Prices.

{kind=link}

Higher energy prices are also good news for financial stocks. This is not too surprising given that the many energy companies borrowed heavily from banks to finance their expansion and found themselves in trouble when oil prices collapsed, potentially impairing bank balance sheets. Materials stocks, another outperforming sector, also tend to benefit from higher energy prices. By contrast, health care, consumer, and utilities stocks typically underperform in the face of higher energy prices and the post-election period has been no exception to this rule.

Here, too, fundamental factors that drive the relative performance of equity sectors appear to better explain the post-election sector rotation than a vague notion that certain industries will benefit from a possible deregulation.

The same is true if one looks at copper, also a powerful factor for explaining sector relative performance. Since Nov. 8, COMEX High Grade Copper prices have risen nearly 10%. As such, it’s not too surprising to see materials, industrial, and energy stocks among the outperformers, and consumer, and utility stocks among the post-election underperformers (Figure 5).

Figure 5: Higher Copper Prices Correlate with Outperformance by Materials, Industrials, and Energy.

{kind=link}

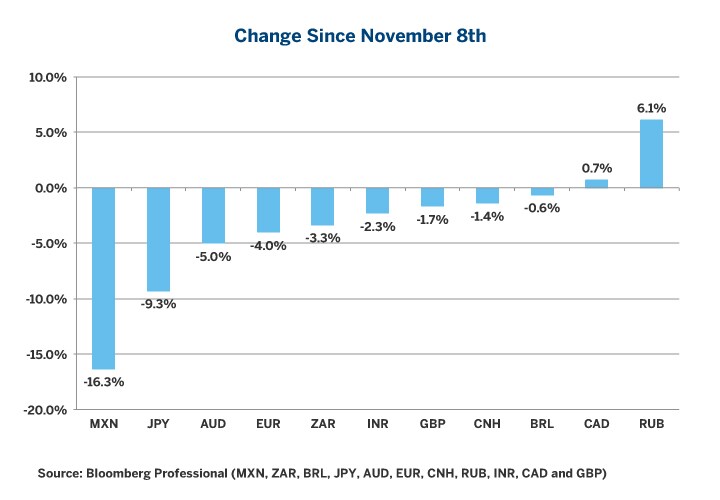

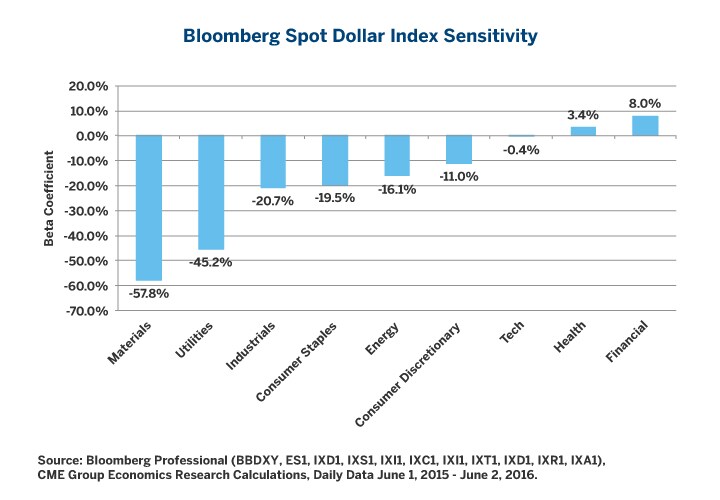

Lastly, since the election, the U.S. dollar has strengthened versus most major currencies (Figure 6). For the most part, a stronger dollar is bad news for stocks: it makes U.S. companies less competitive abroad. However, there are exceptions. A stronger dollar is generally good news for financial shares but bad news for materials, and utilities stocks (Figure 7). This may explain why materials stocks haven’t benefitted as much as one might have expected given the rise in copper prices.

Figure 6: The U.S. Dollar Generally Strengthened After the Election Except Versus Petro-Currencies.

{kind=link}

Figure 7: A Stronger Dollar Tends to Sink Some Boats.

{kind=link}

Outlook

Equity-sector relative performance will likely continue to depend upon how interest rates, currencies and commodity prices trend. Our sense is that short-term interest rates risks are still mainly to the upside. The U.S. employment market is tight and inflation is beginning to rise. If interest rates rise faster than what the forward curve currently suggests (two Fed rate hikes in 2017), this will likely benefit financial stocks and hurt most other sectors. It could also make financial stocks more volatile than other market segments. Any selloff in equity markets could diminish those rate-hike expectations to the detriment of financial shares. If rates rise, it will probably also send the dollar higher against most other currencies, also to the benefit of financial shares and to the detriment of most other sectors.

The future direction of energy prices is unclear. On the bearish side, crude oil inventory levels are exceptionally high and continue to rise; U.S. production is growing again and it is unclear which OPEC nations will adhere to their production targets. On the bullish side, the pace of U.S. inventory growth has slowed considerably and there are substantial risks to the stability of a number of oil suppliers. Higher oil prices would likely benefit the energy, materials, and financial sectors relative to the rest of the market.

Finally, copper prices are highly sensitive to developments in China, whose economy may be set to slow further. If copper prices move lower in 2017, it would likely be bad news for materials stocks and possibly for industrials and energy but could lead the other sectors to outperform.

Bottom line:

- Post-election equity-sector performance is not mainly attributable to expectations of regulatory change under the incoming administration.

- Rather, post-election relative performance of equity sectors appears to have deeper macroeconomic drivers, some of which may have been influenced by the outcome of the election and some of which may have occurred independently of the election result.

- Financial shares have outperformed mainly as a result of higher interest rate expectations and a stronger U.S. dollar, and they may also have benefitted from higher energy prices.

- Soaring oil and copper prices supported energy, and materials stocks, overcoming the negative consequences of expectations for a more rapid Fed tightening, and a stronger dollar.

- Higher interest rates, energy and metals prices, along with a stronger dollar, is a perfect storm of negativity for utilities stocks, which pay high dividends and thus compete with bonds for investors, and make heavy use of both energy (electricity generation) and metals (wiring for distribution).

- Consumer shares, especially staples, have also been depressed by higher interest rates and rising energy prices.

Recommended For You

More about E-mini S&P Select Sector futures

Discover a cost-effective way to manage your portfolio sector exposure with E-mini S&P Select Sector Futures.