{kind=link}

Is Crude Oil Taking Cue from Vegetable Oils?

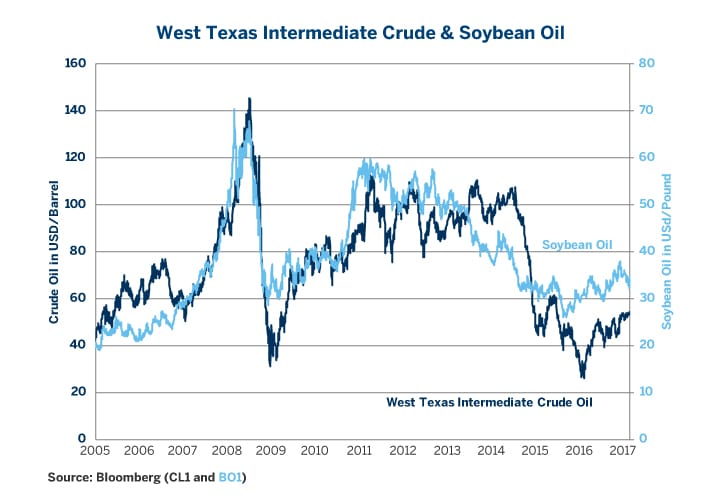

It looks like the ultimate case of the tail that wagged the dog: soybean oil foreshadowing price trends of crude oil (Figure 1). It seems odd. How could the modest soybean oil, whose average daily volume in dollar terms amounted to $2.8 billion in February 2017, lead the colossal West Texas Intermediate crude oil market, whose volume that same month was 21 times greater?

Everybody knows that the muscles in a dog’s tail aren’t strong enough to wag the animal but, as any dog owner knows, a canine’s tail is highly expressive and can indicate its feeling and what it intends to do. Likewise, it’s fairly obvious that vegetable oils aren’t causing crude oil prices to move up or down. But the vast difference in the size of the crude oil and vegetable oil markets may be a part of the explanation for their behavior. Because of the relatively small size of the market, vegetable oil prices may be highly sensitive to subtle supply and demand shifts in crude oil.

Figure 1:

{kind=link}

The key mechanism that drives the relationship is biofuels. Sixty-four countries have or are considering biofuel mandates or targets, including the 27 nations of the European Union. If crude oil is in short supply, refiners may increase their purchases of biofuels, driving the price higher. Likewise, if crude oil supply is abundant or if demand is weak, refiners may reduce their buying of vegetable oils, driving the price down in a manner that appears to anticipate a coming decline in crude oil prices.

Over the past dozen years, the relationship between movements in vegetable oil prices and ensuing changes in crude oil prices have been quite remarkable:

- Soybean oil ignored the rally in crude oil prices in 2006, and later that year crude oil prices corrected lower to the level of soybean oil prices.

- As crude oil was falling in late 2006 and early 2007, soybean oil prices began to surge, ahead of the massive January 2007 to July 2008 bull market rally in crude oil to its all-time high.

- Soybean oil prices peaked in March 2008, four months before crude oil prices reached their all- time highs in July of that year.

- Soybean oil prices hit bottom in December 2008, followed four weeks later by crude oil. By the time crude oil prices had regained their footing in February and March 2009, soybean oil was well into a rally.

- Vegetable oil prices reached their post-financial-crisis peak in February 2011, almost three months before crude oil prices topped out at the end of April 2011.

- While crude oil prices range-traded between $80 and $115 per barrel from 2011 through mid-2014, vegetable oil prices began a long bear market that foreshadowed the abrupt collapse of crude oil in late 2014.

- Soybean oil prices bottomed in August and September 2015, almost six months before crude oil prices hit bottom in January and February 2016.

- Recently, soybean oil prices have been plunging even as crude oil rallies. Does this presage a coming decline in crude oil price?

There is no guarantee, of course, that such a relationship will hold up in the future. There are at least two factors that could temper the apparent relationship between vegetable oil and crude oil prices: 1) some countries may sour on biofuel mandates and repeal them. 2) if crude oil traders accept that vegetable oils may be a leading indicator of crude oil prices, they might change their behavior and respond more quickly to moves in vegetable oil prices. However, that doesn’t appear to be the case for the moment.

For the time being, crude oil traders might well be advised to heed the most recent moves in soybean oil and palm oil, and to give serious consideration to the possibility that the next move in crude oil might be downward. There are other reasons to think that crude oil might be vulnerable to a decline, including:

- Inventories, which continue to grow, are up 7% year on year.

- U.S. production continues to grow and is up nearly 600,000 bpd since July.

- Oil and gas rig counts continue to rise, implying a further increase in U.S. production over at least the next two months, if not longer.

- Oil markets might also get jittery if they begin to doubt the Organization of Petroleum Exporting Countries’ ability to maintain production cuts in May when the producer group must decide if it will extend its six-month output reduction agreement that began January 1.

Oil prices have plenty of upside risks as well, including those coming from possible increases in demand and potential supply disruptions. That said, if oil prices were to fall over the coming weeks or months, don’t say that the vegetable oil markets didn’t warn you.